🧠 SK Hynix Bets AI Broke the Cycle

The AI memory leader is coming to Nasdaq

Welcome to the Premium edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

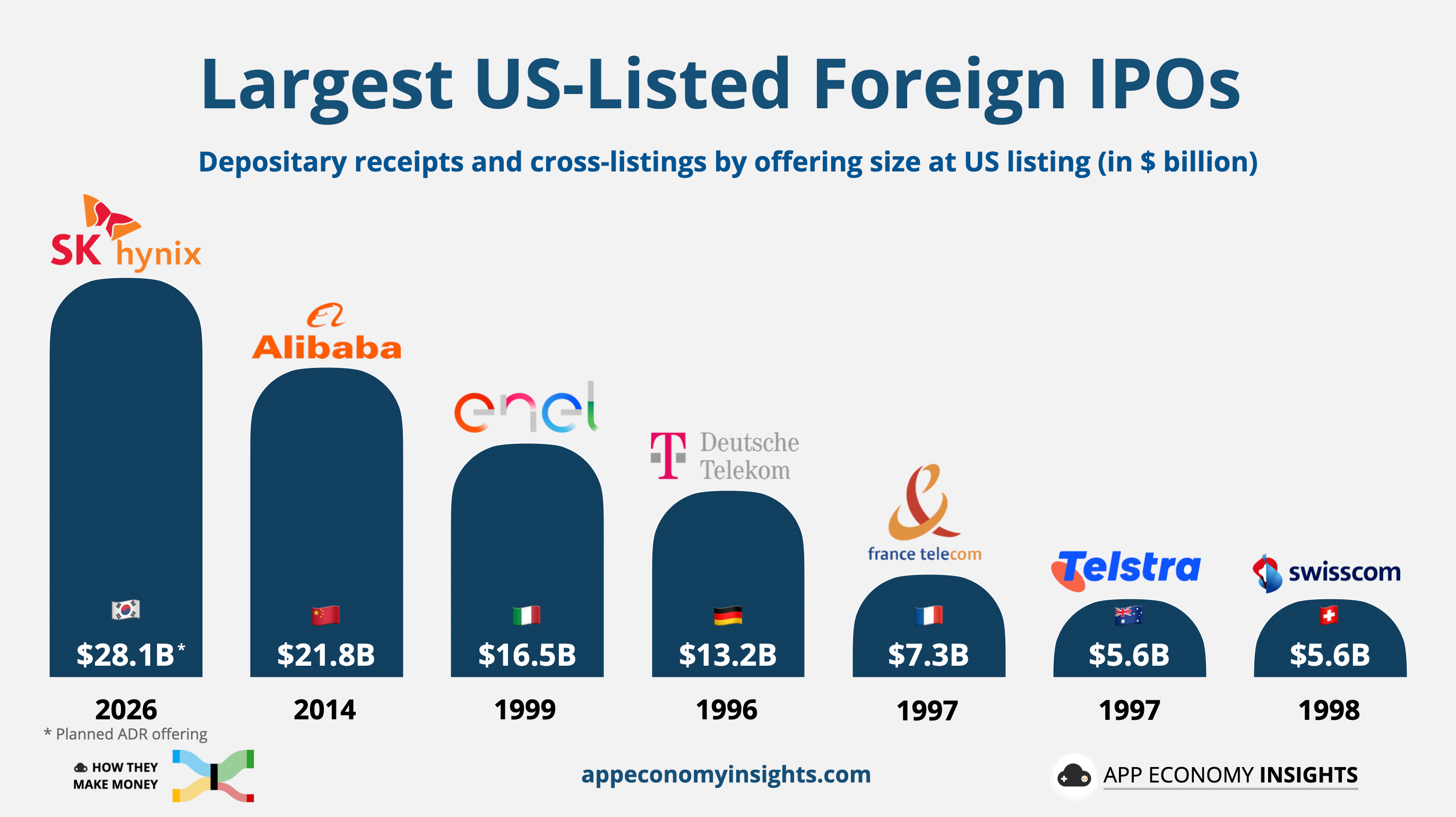

SK Hynix is trying to pull off the largest ADR listing in history.

The planned Nasdaq listing targets over $28 billion (45 trillion won), edging past Alibaba’s ~$22 billion New York debut in 2014. Trading is expected to begin around July 10. Every dollar is earmarked for fabs, packaging, and lithography machines. The funny part is that the company doesn’t really need the money.

SK Hynix is the world’s #1 HBM maker (High Bandwidth Memory) at ~57% share. The company sold out of capacity three years in advance, and it just surpassed Samsung to become South Korea’s most valuable company. It also already trades right in line with Micron, near 7x forward earnings. The re-rating a Nasdaq listing is supposed to deliver already happened.

We broke down Micron’s blowout quarter last week, noting that the company benefited from the AI memory shortage.

This week, the leader that ships the majority of NVIDIA's HBM is asking US investors to price it like the AI infrastructure play it has become.

Today at a glance:

📈 The US Listing

🧠 How SK Hynix Makes Money

📊 Q1 FY26 in Numbers

🇰🇷 What You're Paying

⚔️ Competition & Risks

🔭 What to Watch

🧭 Personal Take

📈 The US Listing

SK Hynix shares trade in Seoul, in won, on the Korea Exchange. That makes them awkward and expensive for US institutions to touch directly. An American Depositary Receipt (ADR) solves that. The company issues new shares, parks them with a custodian bank, and a US depositary issues receipts that trade on Nasdaq in dollars like any American stock.

SK Hynix plans to issue up to 178 million ADRs, the equivalent of 2.5% of the company. Each Seoul share trades near $1,580 (₩2,425,000) and splits into ten ADRs, so a single ADR is referenced at around $158 (₩242,500), with the final price set on July 10. The ADRs list on the Nasdaq Global Select Market under SKHY.

Every dollar is going into capacity.

The proceeds are split four ways:

🏭 Yongin Y1: the first fab at SK Hynix’s sprawling new Yongin cluster, its next major DRAM and HBM base.

📦 Cheongju P&T7: an advanced packaging plant built for HBM, where the die-stacking that sets SK Hynix apart actually happens.

🔬 ASML EUV scanners: the extreme-ultraviolet lithography tools that leading-edge DRAM can’t be made without.

🇺🇸 Indiana: a $4 billion packaging plant, SK Hynix’s first US fab.

Compare that to the SpaceX IPO. SpaceX is raising funds for its CapEx ramp, with $10 billion in negative free cash flow in Q1 alone. SK Hynix is raising money from a position of strength, with $24 billion in net cash and an order book sold out through 2028.

SK Hynix first floated a raise of around $10 billion, and the board eventually settled on $28 bllion. You don’t do that unless internal demand forecasts have moved well past the old memory-cycle playbook.

There’s a control wrinkle worth mentioning. SK Square, the holding company that owns ~20% of SK Hynix, must keep its stake above 20% under Korea’s holding-company rules. That constraint is why the deal issues new shares sized to protect that floor, rather than selling treasury stock. Some Korean shareholders are unhappy about the dilution. For US investors, the dilution is the price of admission to a stock they couldn’t easily buy before.

🧠 How SK Hynix Makes Money

The comeback

SK Hynix started in 1983 as Hyundai Electronics, the chip arm of the Korean industrial group. The Asian financial crisis reshaped it. Seoul forced a 1999 merger with rival LG Semicon, creating a top-tier DRAM maker overnight and burying it in debt. When memory prices collapsed ~80% in 2001, the renamed Hynix lost billions, fell under creditor control, and became a national symbol of corporate failure.