🚀 How SpaceX Makes Money

Starlink funds the moonshots

Welcome to the Premium edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

🚀 SpaceX is going public

The rocket company is now an AI company too.

The IPO filing landed last week, with xAI, Grok, and X folded inside. SpaceX aims for a $1.5–$2 trillion valuation with up to $75 billion raised, which would make it the largest IPO in history by both measures.

The pitch writes itself in three lines.

Starlink generates the cash.

Rockets bend the cost curve.

AI and Mars are the moonshots.

This may be the most ambitious story ever brought to public markets.

It’s also the messiest.

I condensed 300+ pages of S-1 into a clean breakdown, supported by our signature visuals. By the end, you'll have a sum-of-the-parts framework for SpaceX, and a view on whether the IPO price makes sense.

Today at a glance:

Overview

Business Model

Financial highlights

Risks & Challenges

Management

Use of Proceeds

Future Outlook

Personal Take

1. Overview

SpaceX is no longer just a rocket company. It‘s the world’s dominant launch provider, the operator of the largest satellite network ever built, the Pentagon's primary access to orbit, and now the corporate home of xAI, Grok, and X following a February 2026 merger.

One framing note before we dig in: The S-1's financials have been retroactively rewritten. Every prior period now includes xAI and X as if they'd always been part of SpaceX. So all financial data is a consolidated view that bakes in AI, X advertising, and data licensing.

The basics:

Headquarters: Starbase, Texas (reincorporated from Delaware in 2024)

Founded: 2002 by Elon Musk

Ticker: SPCX (Nasdaq)

Mission: Make life multiplanetary

You probably have heard of SpaceX’s two main rocket programs:

Falcon 9 is the medium-lift workhorse that flies today.

Starship is the next-generation fully reusable super-heavy vehicle still in development, designed to carry roughly 5x more payload per launch.

The railroad to space

The cleanest way to think about SpaceX is as a railroad to space. Before SpaceX, rockets were discarded after launch — the equivalent of scrapping a 747 after every flight. That was the entire industry.

Reusability changed the economics. NASA estimates Falcon 9 brought launch costs to ~$2,700 per kilogram, against a historical industry average of $18,500 — an 85% reduction. One Falcon 9 booster has now flown 34 times. Starship is designed to take another 99% off that figure if it works at scale.

At its core, SpaceX is an infrastructure story. Cheap, reliable access to orbit turned launch from a bespoke government project into something closer to a utility. Once orbit is cheap, businesses that were never economically viable suddenly are. Starlink, SpaceX's satellite internet service, is the proof. AI compute in orbit may be the next. Mars is the eventual destination.

Three segments under one roof

The S-1 presents SpaceX in three segments:

🚀 Space: Falcon, Dragon, Starship, and the launch business that serves NASA, the Pentagon, intelligence agencies, and commercial customers

🛰️ Connectivity: Starlink consumer, enterprise, government, and direct-to-mobile

🤖 AI: xAI, Grok, X, and the compute infrastructure underneath all of it

Each segment has a different economic profile, and the gap between them is the most important thing to understand about this filing. We’ll break that down next.

Scale, in numbers

Launch dominance

~650 orbital launches, >540 on flight-proven boosters

>80% of everything launched into orbit since 2023, by weight

165 Falcon launches in 2025, up from 96 in 2023 — a 30%+ annual cadence

>99% Falcon mission success across ~7,400 metric tons cumulatively to orbit

Network scale

~9,600 Starlink satellites in orbit — roughly 75% of all active maneuverable satellites worldwide

10.3 million subscribers across 164 countries

Financials

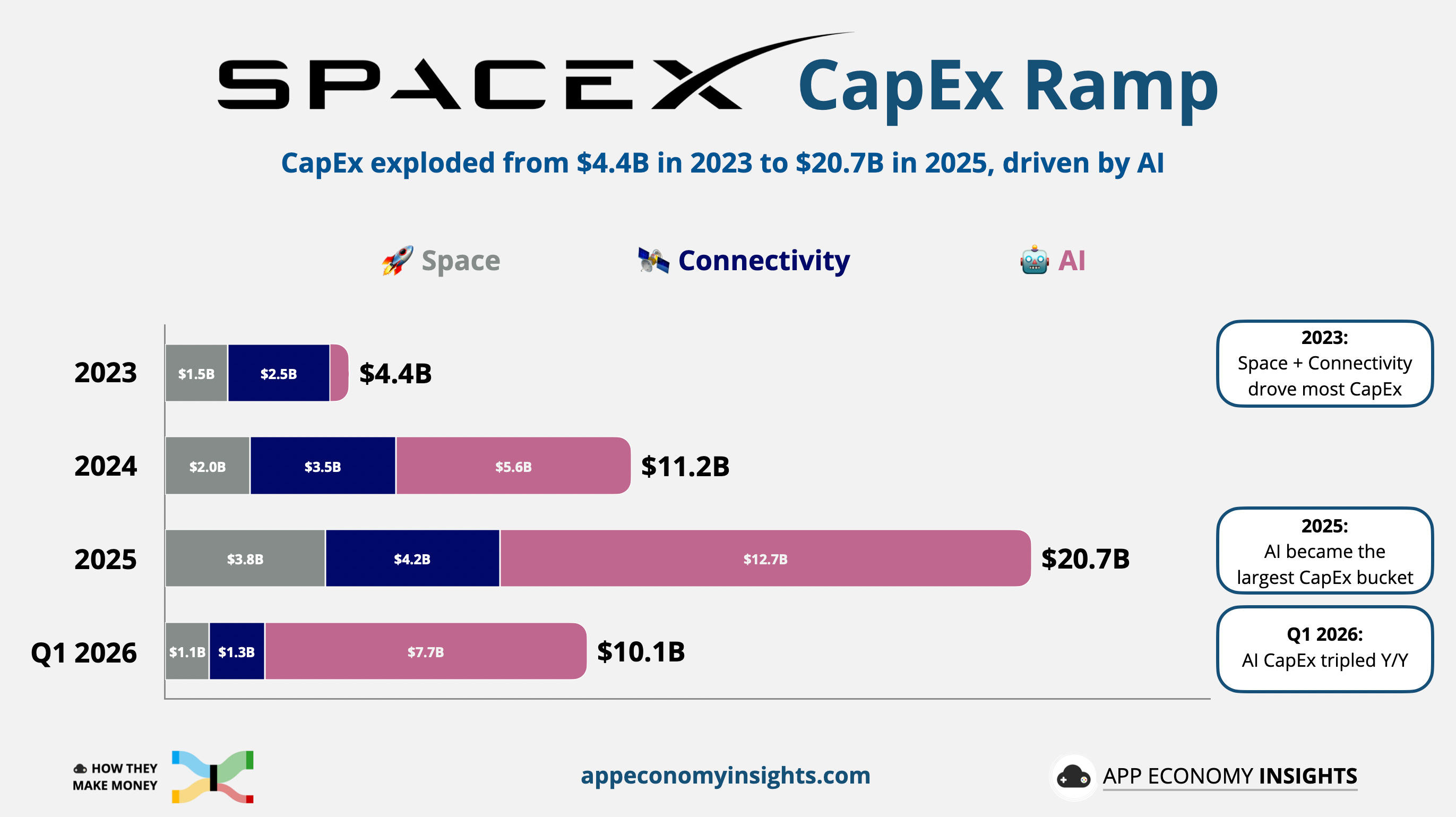

$18.7 billion in FY25 revenue (+33% Y/Y)

$20.7 billion in FY25 CapEx (nearly 5x in two years)

At this stage, SpaceX spends more than it makes. The IPO story comes down to one question: Does each new dollar of AI CapEx create a wider moat or just a bigger cash burn?