📊 PRO: This Week in Visuals

AMD ARM ANET MCD SHOP APP UBER NVO PFE MAR NET MELI ABNB DASH CRWV RACE FTNT COIN DDOG PYPL XYZ LYV CPNG FI AXON RDDT EXPE TWLO KHC AFRM GPN FLUT TOST QSR HUBS DOCN SNAP Z NYT DKNG TEM MTCH CELH TTD

Welcome to the Saturday PRO edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Premium members get:

📊 Monthly reports: 200+ companies visualized.

📩 Tuesday articles: Exclusive deep dives and insights.

📚 Access to our archive: Hundreds of business breakdowns.

PRO members get everything PLUS:

📩 Saturday PRO reports: Timely insights on the latest earnings.

Today at a glance:

↗️ AMD: CPU Reawakening

📱 Arm: AGI CPU Demand Doubles

🌐 Arista Networks: Demand Beats Supply

🍟 McDonald’s: Value Plays Through Anxiety

🛍️ Shopify: Growth Deceleration Ahead

📱 AppLovin: Axon Opens to the World

🚖 Uber: Bookings Accelerate

🇩🇰 Novo Nordisk: Oral Wegovy Boost

💉 Pfizer: Defining Period

🏨 Marriott: US Demand Reaccelerates

☁️ Cloudflare: Shrinking To Grow Faster

🤝 MercadoLibre: Growth Over Margins

🛖 Airbnb: Guidance Goes Higher

🥡 DoorDash: Demand Offsets the Misses

☁️ CoreWeave: Backlog Near $100B

🏎️ Ferrari: Scarcity Holds Up

🔒 Fortinet: AI-Era Demand Surge

📈 Coinbase: Crypto Winter Continues

🐶 Datadog: AI Becomes the Engine

💳 PayPal: Lores Lays Out the Cuts

🔲 Block: AI Bet Pays Off

🎤 Live Nation: Antitrust Bill Lands

🇰🇷 Coupang: Recovery Takes Time

💳 Fiserv: Transformation Strain

⚡️ Axon: AI and Counter-Drone Inflection

👽 Reddit: Profitability Tier Unlocked

✈️ Expedia: B2B Carries The Load Again

💬 Twilio: Voice AI Reaccelerates

🌭 Kraft Heinz: Early Traction

🌈 Affirm: Card Engine Keeps Roaring

🌎 Global Payments: Worldpay Era Begins

🏈 Flutter: Howe Out, Predictions In

🍞 Toast: Agentic Platform Hits Stride

🍔 RBI: Burger King's Inflection

📢 HubSpot: Another Pricing Pivot

🌊 DigitalOcean: AI Capacity Surge

👻 Snap: Restructure & Reset

🏠 Zillow: Profit Outlook Spooks Street

🗞️ NYT: Ad Engine Reaccelerates

👑 DraftKings: Predictions Push Goes Live

🧬 Tempus AI: Pharma Brings Visibility

🔥 Match Group: Tinder Rebounds

⚡️ Celsius: Portfolio Plays the Hits

📺 The Trade Desk: Guide Disappoints Again

🚲 Peloton: Turnaround Finds Its Footing

🏴 Klaviyo: Agents Find Leverage

🍿 AMC: Box Office Leverage

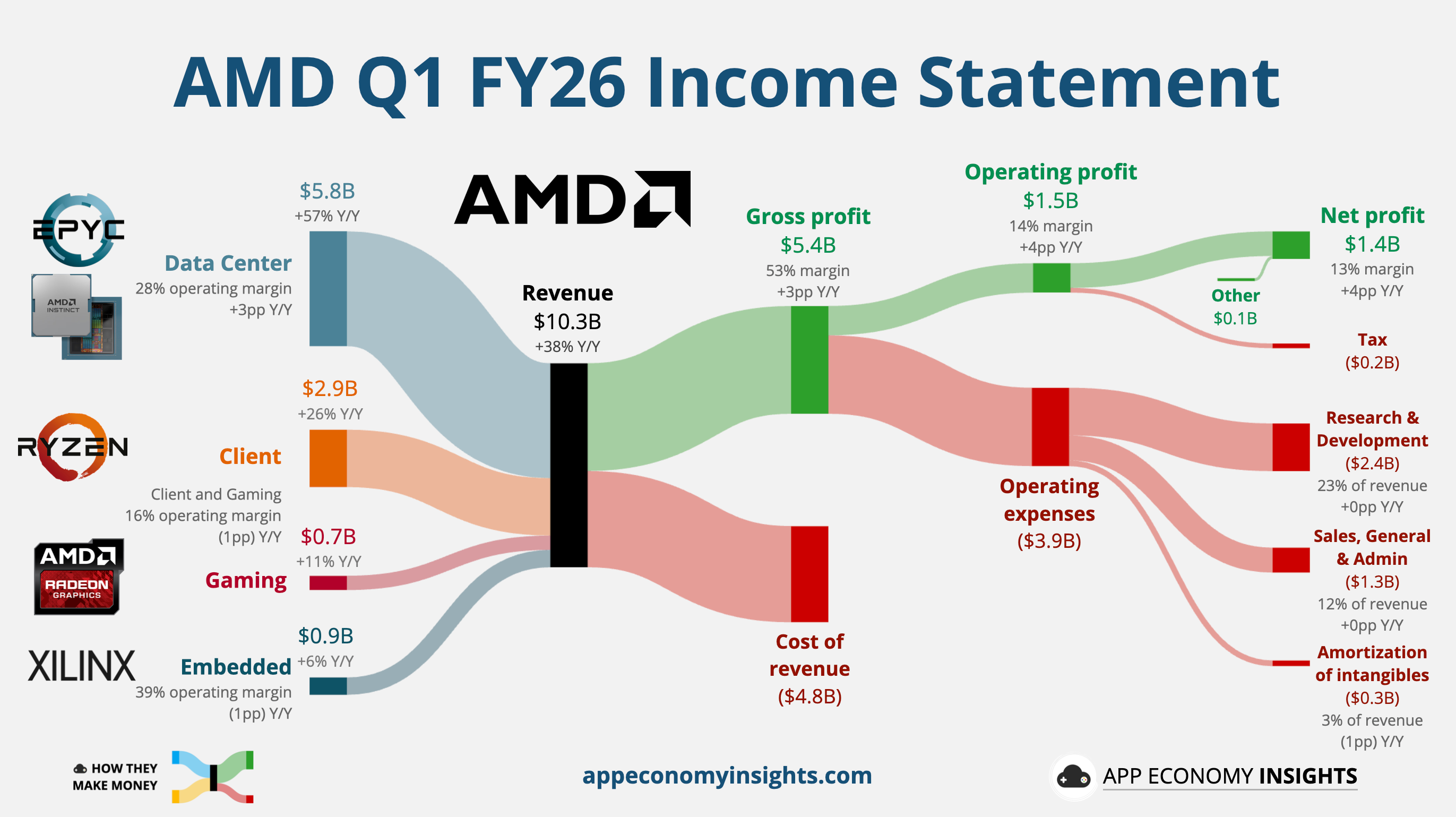

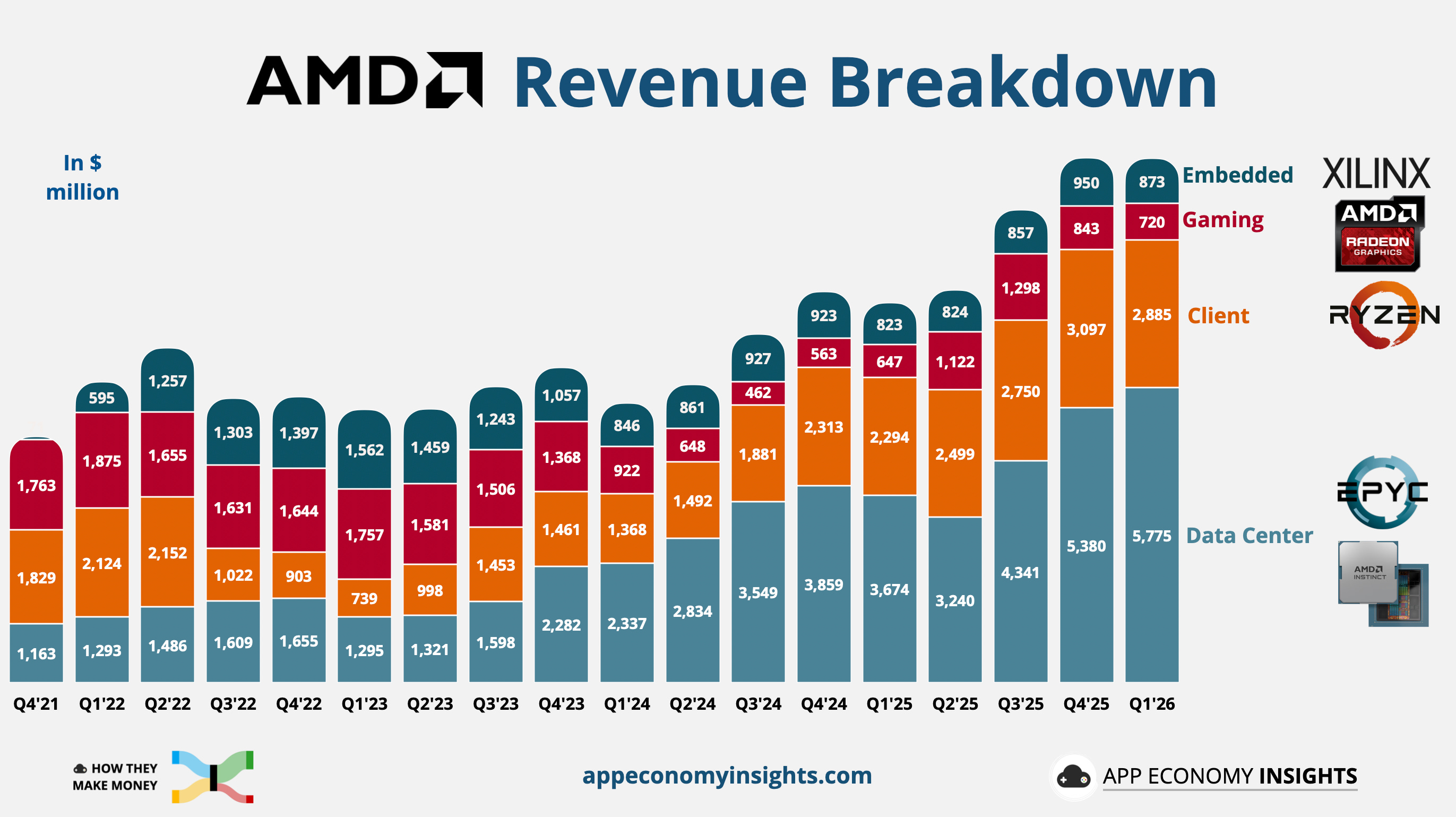

1. ↗️ AMD: CPU Reawakening

AMD’s Q1 revenue rose 38% Y/Y to $10.3 billion ($0.3 billion beat), and non-GAAP EPS was $1.37 ($0.08 beat).

Data Center revenue surged 57% Y/Y to $5.8 billion, ahead of expectations, as EPYC CPUs and Instinct GPUs became the primary growth engine. Free cash flow more than tripled to a record $2.6 billion, showing the AI ramp is already flowing through the model.

The biggest shift was not just GPUs. AMD doubled its server CPU market outlook, now expecting the TAM to grow at a 35%+ annual rate to more than $120 billion by 2030, up from its prior 18% CAGR view. The logic is simple: inference and agentic AI require more CPU compute for orchestration, data movement, parallel execution, and head nodes for accelerators. AMD now expects server CPU revenue to grow more than 70% Y/Y in Q2, with robust growth continuing into the second half and 2027.

The accelerator story also strengthened. AMD said that MI450 and Helios customer forecasts now exceed initial expectations, with production shipments still on track to ramp in the second half. The company pointed to multi-generation partnerships with Meta and OpenAI, plus additional large-scale customer interest, as evidence it can generate tens of billions in annual data center AI revenue in 2027. That matters because AMD is no longer pitching itself as a distant NVIDIA alternative. It’s trying to become the second strategic AI platform for hyperscalers that need more supply and leverage.

Outside Data Center, the picture was less explosive. Client and Gaming revenue rose 23% Y/Y to $3.6 billion, with Client up 26% and Gaming up 11%. Ryzen demand remains strong, especially in commercial PCs, but management warned that higher memory and component costs could pressure second-half PC and gaming demand. Embedded returned to growth, up 6% Y/Y to $873 million, helped by test, aerospace, defense, communications, and broader x86 adoption.

Management guided Q2 revenue to $11.2 billion (a massive $0.7 billion beat at the midpoint), implying 46% Y/Y growth, with adjusted gross margin expected to improve to 56%. The setup is increasingly about execution under constraint: securing enough wafers, back-end capacity, memory, and data center power to meet demand. The next test is whether AMD can turn MI450 and Helios into large-scale 2027 deployments while keeping gross margins in the 55%–58% long-term range.

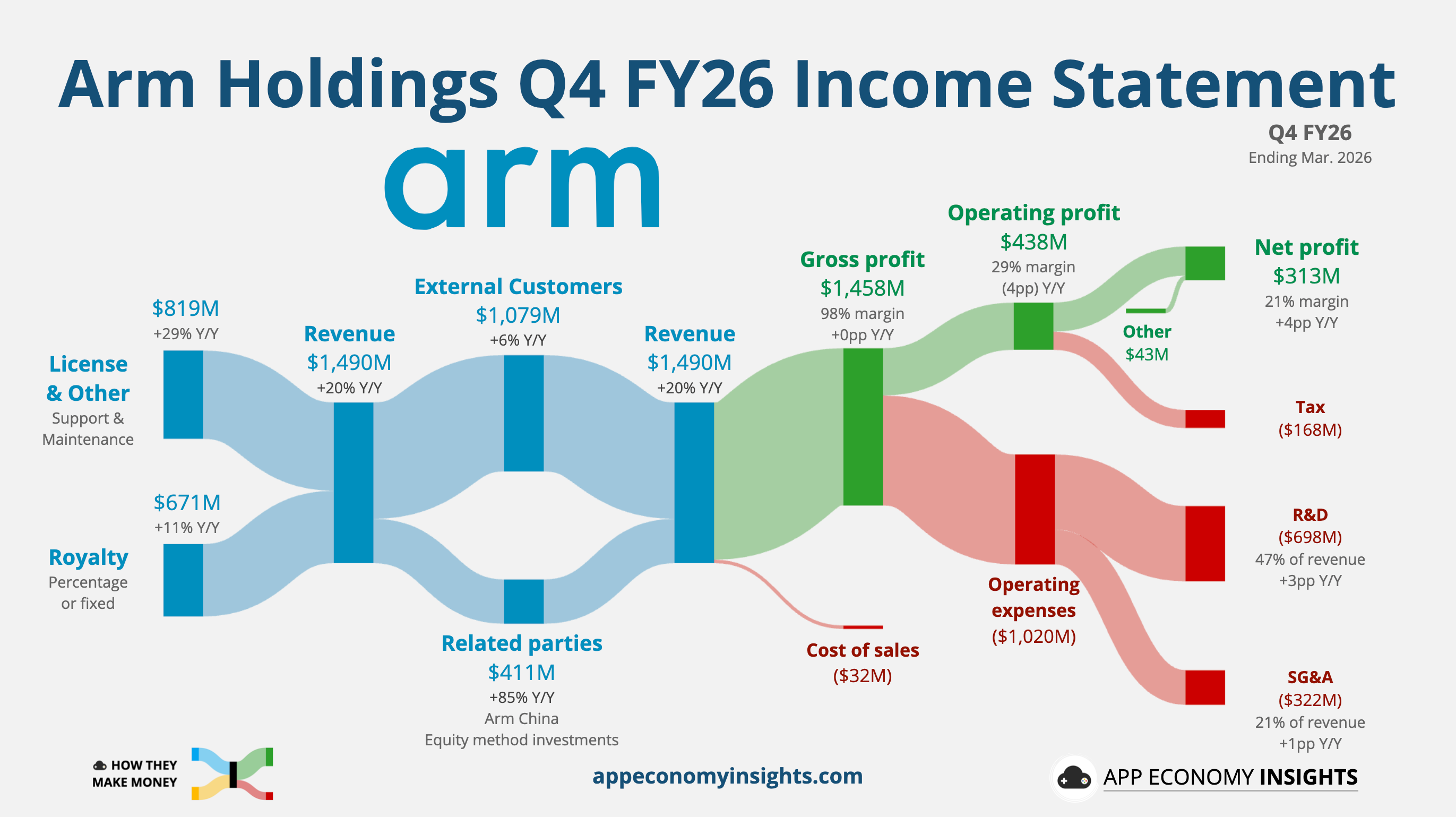

2.📱 Arm: AGI CPU Demand Doubles

Arm Q4 FY26 (March quarter) revenue rose 20% Y/Y to $1.5 billion ($20 million beat), and non-GAAP EPS was $0.60 ($0.02 beat).

Licensing surged 29% to $819 million, $43 million ahead of consensus.

Royalties grew just 11% to $671 million — a $22 million miss as memory chip shortages weighed on smartphone production.

ACV (Annualized contract value), a metric for normalized license and other revenue, rose 22% Y/Y to $1.7 billion.

Shares fell over 10% as the smartphone slowdown overshadowed AI data center momentum.

The headline story is the Arm AGI CPU, Arm’s first homegrown data center chip and a direct competitive shift against its own customers. Demand more than doubled to over $2 billion across FY27 and FY28, but Arm held its revenue forecast at $1 billion citing TSMC advanced-node wafer constraints. Meta is the lead partner and co-developer. Data center royalty revenue more than doubled Y/Y, with Neoverse CSS holding ~50% market share among top hyperscalers.

CEO Rene Haas saw smartphone unit growth “flip to negative,” though the weakness was concentrated in low-end phones where Arm earns lower royalty rates. The cost of building chips directly is showing up in margins: operating margin fell to 29% from 33% a year ago.

For Q1 FY27, Arm guided revenue to ~$1.26 billion (vs. $1.25 billion consensus) and non-GAAP EPS of ~$0.40 (vs. $0.36 consensus), with both royalty and licensing growing ~20%. Long-term FY31 targets remain intact at $25 billion revenue ($15 billion from AGI CPU, $10 billion from IP) and $9+ EPS. The next quarter test is whether royalty growth reaccelerates as the smartphone memory squeeze eases, and whether TSMC capacity loosens enough to let Arm convert the full $2 billion in AGI CPU demand into revenue rather than the $1 billion currently guided.