🏆 Live Sports Steal the Show

Q1 events lifted revenue but exposed the rising rights bill

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

🏆 The Live Sports Trade-Off

Comcast called it “Legendary February.” For 17 days, the Winter Olympics, Super Bowl, and NBA All-Star Game all aired across NBCUniversal, generating over $2 billion of incremental revenue.

Disney got its own Super Bowl boost on ABC. Paramount leaned on the NFL and UFC. Roku benefited as tentpole events pulled more ad dollars into connected TV.

The takeaway from media earnings is clear: live sports are one of the few remaining forces powerful enough to reshape an entire quarter.

But the same quarter also showed the trade-off. Comcast’s Media EBITDA swung to a $426 million loss as NBA rights hit the P&L. Disney’s Sports operating income fell 5%. Warner, having walked away from the NBA, saw linear ad revenue dropped 8%.

The bill for being in sports keeps rising. The bill for sitting out may be even higher.

Today at a glance:

🏰 Disney: Streaming Finally Scales

🦚 Comcast: The Sports Bill Arrives

🎥 Warner: Paramount’s Inheritance

⛰️ Paramount: The Easy Part Is Over

📺 Roku: The CTV Toll Booth

FROM OUR PARTNERS

📊 Fiscal.ai: 25% Off Your Research Terminal

Fiscal.ai now powers my charts and financial data.

It’s my favorite place to research new stock ideas and visualize their performance:

Chart builder.

Portfolio tracker.

Stock screeners.

Earnings materials.

Side-by-side comparisons.

Quick fundamentals overlays.

You can select a specific company revenue segment or KPI and compare it across multiple companies. Turn financial data into charts, comparisons, and insights in minutes.

Fiscal.ai is our data partner, so our readers already get 15% off their paid plans. And this week only, you get an even larger discount of 25% off all their paid plans!

But don’t wait! The discount is only valid until Thursday, May 14th.

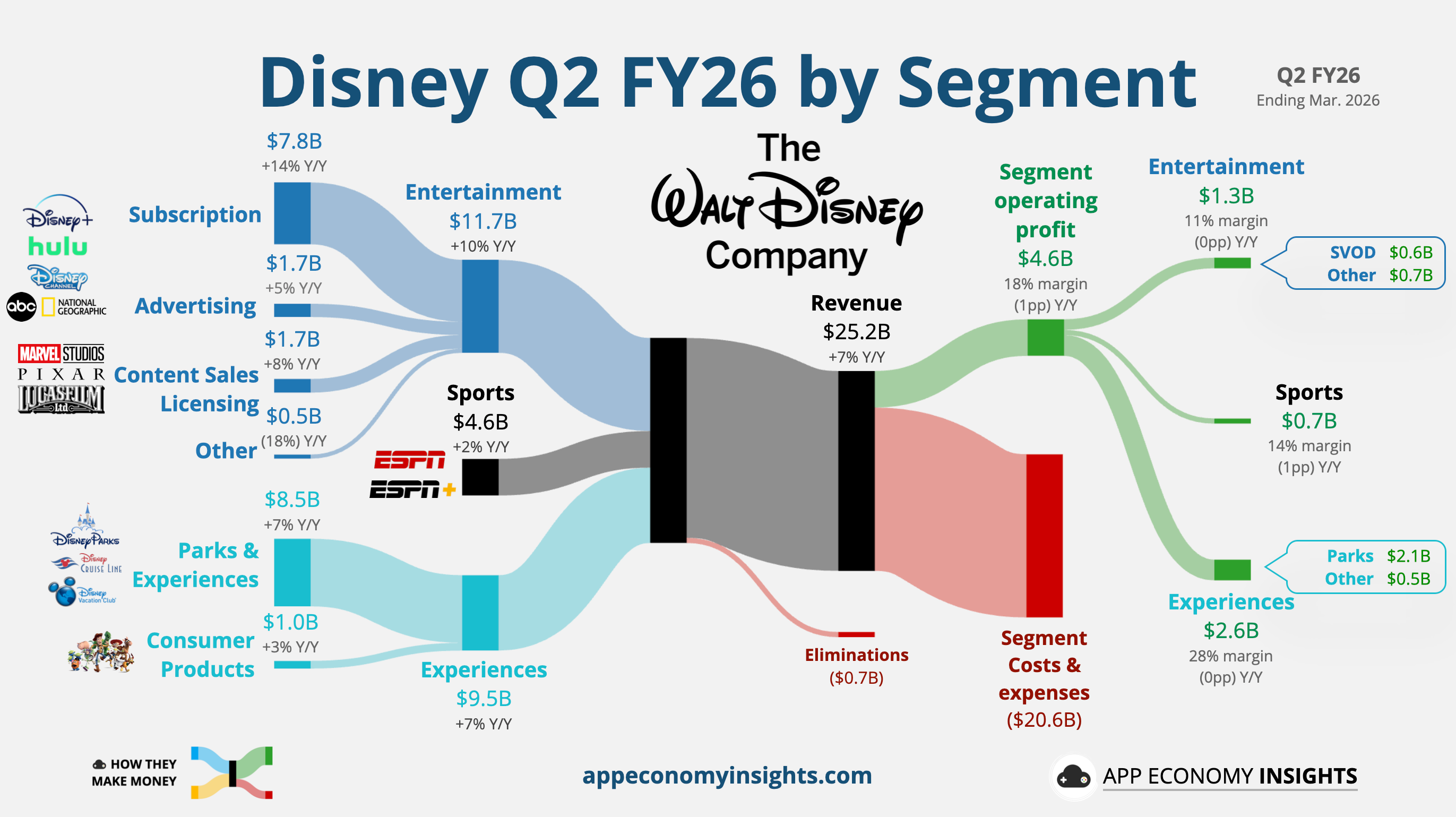

🏰 Disney: Streaming Finally Scales

Disney’s fiscal year ends in September, so the March quarter was Q2 FY26.

📸 Big picture: Revenue rose +7% Y/Y to $25.2 billion ($0.3 billlion beat), and adjusted EPS grew +8% to $1.57 ($0.07 beat) in new CEO Josh D’Amaro’s first quarter at the helm. Total segment operating income rose +4% to $4.6 billion, with all three segments beating expectations. Disney also guided FY26 adjusted EPS growth to ~12% and raised its buyback target to at least $8 billion.

📈 Streaming hits double-digit margins: DTC profitability inflected meaningfully. Disney+/Hulu profits jumped +88% Y/Y to $582 million on subscriber growth, January’s price hike, and ad improvements — delivering Disney’s first-ever double-digit DTC margin. Disney has also stopped reporting subscriber counts, mirroring Netflix’s playbook.

🍿 Entertainment swings up: Entertainment revenue grew +10% Y/Y, helped by the Fubo transaction and a stronger film slate. Avatar: Fire and Ash, Zootopia 2, and Pixar’s Hoppers have generated more than $3.7 billion combined at the global box office. Streaming now generates more than 2x the revenue of linear at Disney Entertainment.

🏰 Experiences keep cruising: Experiences revenue rose +7% to $9.0 billion, with operating income up +5% to $2.6 billion. Cruise capacity remains the growth engine, with the fleet set to expand from 8 to 13 ships by 2031. Domestic park attendance dipped -1% on softer international visitation, but global attendance grew +2%, and per-guest spending rose.

🏈 Sports stuck in transition: Sports revenue grew just +2%, while ESPN operating income fell -5% to $652 million on lower ad revenue and higher rights costs. Q3 sports operating income is guided to fall -14% on rights timing. CFO Hugh Johnston also shut down the linear-spinoff debate, calling it “highly complex” and unlikely to create value.

🤖 D’Amaro’s vision: In a 3,000-word shareholder letter, D’Amaro positioned Disney+ as the company’s “digital centerpiece” — a single hub for streaming, games, parks bookings, and merchandise. AI is also being deployed for ad targeting and labor forecasting at the parks.

Bottom Line: D’Amaro inherited a better setup than Iger did, and his first move gives Disney a strategy investors can finally model: Disney+ as the front door to streaming, sports, games, parks, and commerce. ESPN and parks remain pressure points, but the quarter made the bull case cleaner.

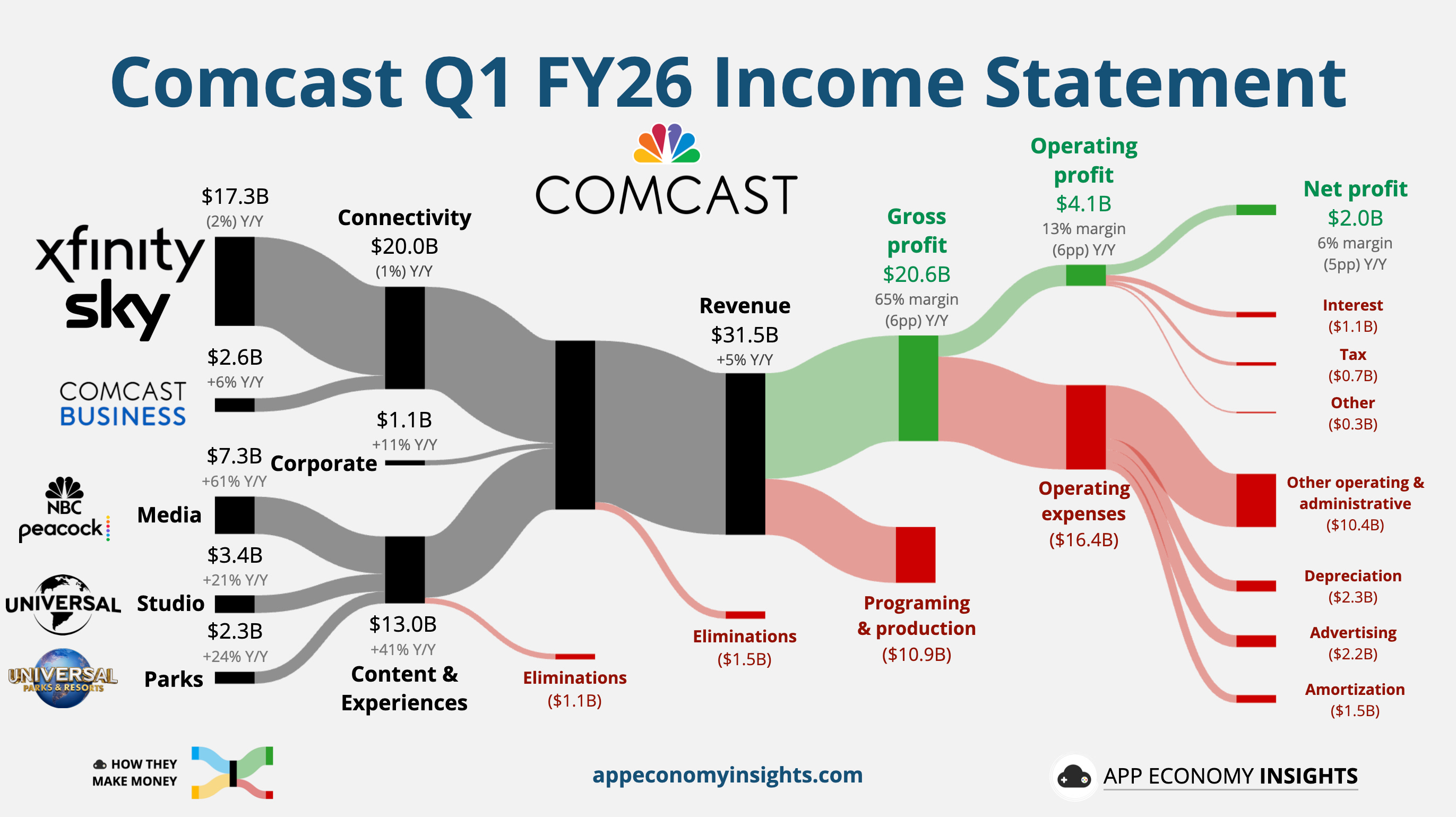

🦚 Comcast: The Sports Bill Arrives

📸 Big picture: Revenue rose +5% Y/Y to $31.5 billion ($1.1 billion beat), or +11% pro forma post-Versant. Adjusted EPS fell -27.5% to $0.79 ($0.06 beat), and adjusted EBITDA declined -9% to $7.9 billion as NBA rights costs hit the P&L for the first time.

📉 Broadband losses moderate: Comcast lost only 65,000 domestic broadband customers, far better than the ~170,000 analysts feared and the first Y/Y improvement since Q4 2020. The catch: domestic broadband revenue still fell 5% to $6.3 billion as $45/month price guarantees and free wireless bundles compress ARPU.

📱 Wireless sets a record: Xfinity Mobile posted its best net additions quarter ever, with domestic wireless service revenue up +15% to $977 million. The real test arrives in 2H 2026, when bundled free lines hit their one-year mark and convert to paid. Early cohorts are seeing “a significant majority” roll over.

🦚 Peacock breaks $2 billion: Peacock added 5 million paid subscribers to reach 46 million, with revenue up +71% Y/Y to $2.1 billion. EBITDA losses widened to $432 million on NBA costs, but management called Q1 the “peak dilution” and guided Peacock to “approach profitability” in Q2.

🎢 Epic Universe keeps printing: Theme parks revenue jumped +24% to $2.3 billion, with EBITDA up +33% to $551 million, fueled by Epic Universe’s first full year in Orlando. International parks softened, but US parks show no concerning pullback.

📺 ‘Legendary February’ comes at a cost: The 17-day Olympics/Super Bowl/NBA All-Star stretch generated $2.2 billion in advertising alone, more than doubling Media ad revenue. Yet Media EBITDA still swung to a $426 million loss as NBA costs hit the segment.

Bottom line: Comcast’s pivot is working, but the trade-off is visible: lower broadband ARPU today in exchange for better retention and a larger wireless base tomorrow. If free lines convert to paid in 2H, the strategy starts to compound. If not, Comcast just bought stability at a steep price.

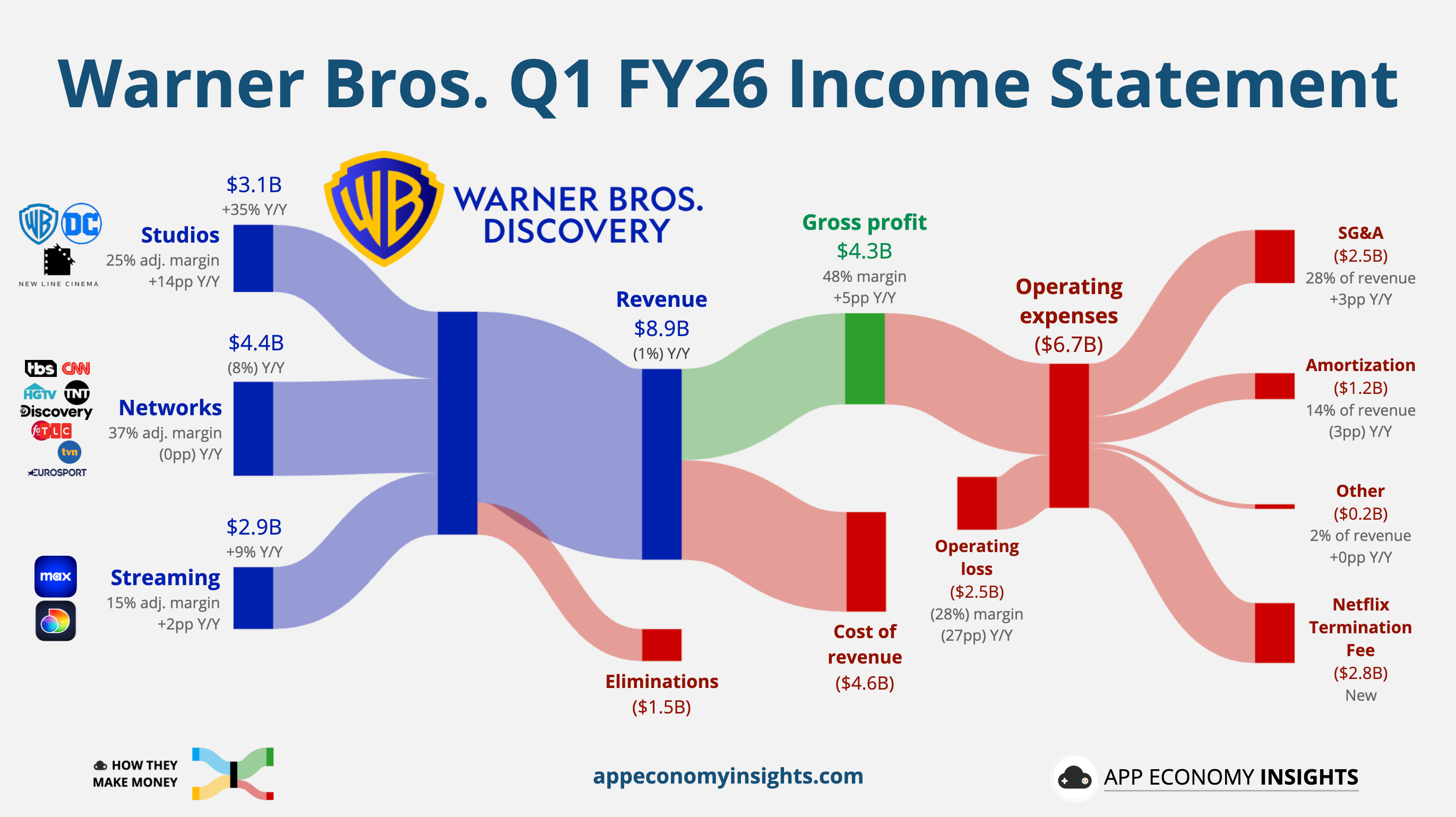

🎥 Warner Bros: Paramount’s Inheritance

📸 Big picture: Revenue dipped -1% Y/Y to $8.9 billion ($10 million beat), or -3% in constant currency. GAAP EPS came in at -$1.17 ($1.08 miss), with the $2.9 billion net loss almost entirely driven by the $2.8 billion Netflix termination fee Paramount paid on WBD’s behalf, plus acquisition-related amortization and restructuring. Excluding those items, the results were broadly in line.

🍿 Studios still on a roll: Studios revenue surged +35% Y/Y to $3.1 billion, with adjusted EBITDA up +199% to $775 million. Wuthering Heights anchored the slate, and CEO David Zaslav reaffirmed the goal of at least $3 billion in WB Studios EBITDA for the year. The “Warner Bros.” side is doing exactly what the bull case requires.

📈 Streaming crosses 140 million: HBO Max launched in the UK, Germany, Italy, and Ireland, helping the company “meaningfully exceed” its prior 140 million subscriber target. Streaming revenue rose +9% to $2.9 billion, and EBITDA grew +29% to $438 million. Management now expects to exit 2026 with more than 150 million subscribers globally.

📺 Linear keeps bleeding: Global Linear Networks revenue fell -8% Y/Y to $4.4 billion, with EBITDA down -9% to $1.6 billion. Ad revenue declined -8% in constant currency, with the absence of the NBA accounting for 7 points of the drop. CFO Gunnar Wiedenfels said the company has “long stopped viewing our linear networks as linear networks” — a tacit acknowledgment that the segment is being managed for cash, not growth.

🪧 The deal is almost done: WBD shareholders approved Paramount Skydance’s $31/share cash offer in April. Closing remains targeted for the end of Q3, pending foreign regulatory approval. WBD ended the quarter with $30.1 billion in net debt, or 3.4x leverage — Paramount’s inheritance.

Bottom Line: WBD’s quarter was good enough underneath the accounting noise, but the stock is no longer trading on operations. With Paramount’s offer locked in, investors are effectively underwriting deal timing, regulatory risk, and the ticking-fee sweetener. The operational story is real, but the trade is no longer about WBD.

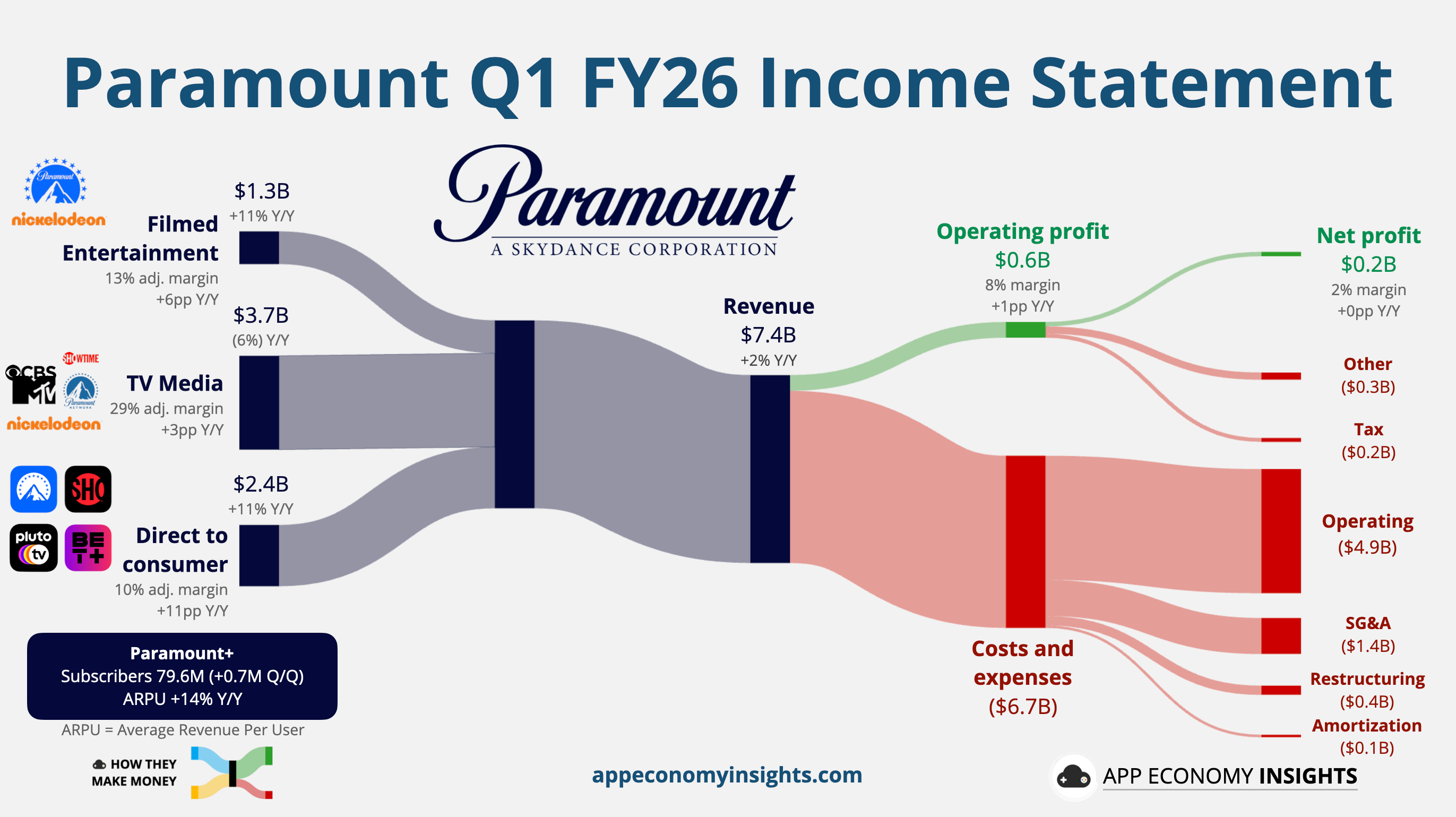

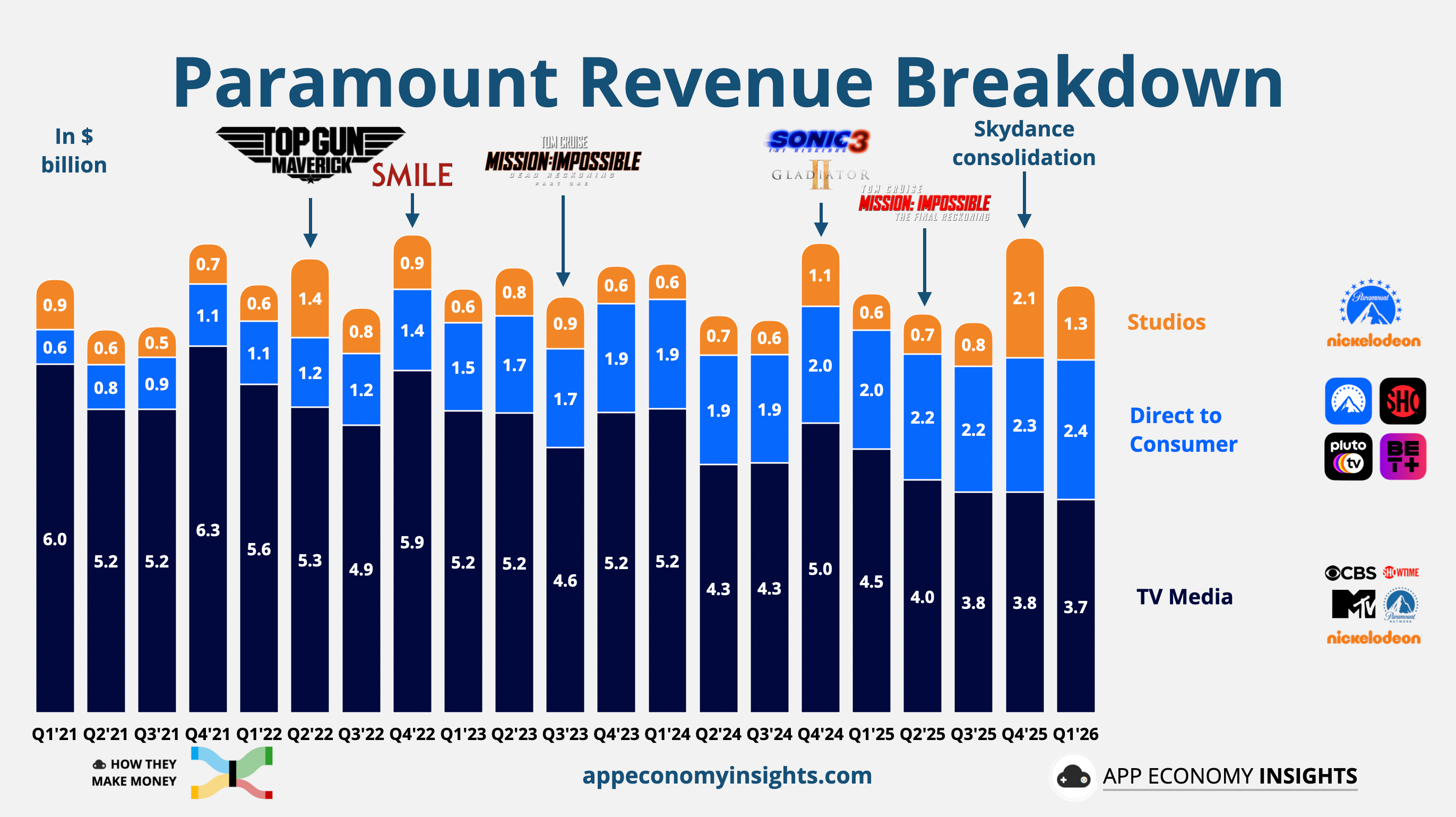

⛰️ Paramount: The Easy Part Is Over

📸 Big picture: Revenue rose +2% Y/Y to $7.4 billion ($70 million beat) in Paramount Skydance’s second quarter under new ownership. Adjusted EPS came in at $0.23, down from $0.29 a year ago, while adjusted EBITDA jumped +59% to $1.2 billion. The company reaffirmed its 2026 outlook of $30 billion in revenue and $3.8 billion in adjusted EBITDA.

📉 TV Media keeps sliding: Linear remains the drag, with TV Media revenue down -6% Y/Y to $3.7 billion, better than the -9.5% Wall Street feared. Affiliate and ad revenue both declined, though total advertising improved versus Q4, and management expects ad growth to return in 2H 2026.

📈 Streaming holds up: Direct-to-Consumer revenue grew +11% Y/Y to $2.4 billion, with Paramount+ revenue up +17% to $2.0 billion on a +14% ARPU lift from January’s price hike. Paramount+ ended with 79.6 million subscribers after exiting low-value international hard-bundle subs, and management expects near-term subs to stay “flattish” as more bundles roll off.

🎬 Studio finds its footing: Filmed Entertainment revenue grew +11% to $1.3 billion, anchored by Scream 7 — now the highest-grossing entry in the franchise’s history. Ellison reaffirmed the target of 30 theatrical films per year, with 15 on the 2026 calendar. Landman also became the most-watched series in Paramount+ history.

♟️ WBD closing in Q3: Paramount drew $2.2 billion on its credit facility to help pay Netflix’s $2.8 billion breakup fee, ending Q1 with $1.9 billion in cash and $15.5 billion in gross debt. The $110 billion WBD deal cleared a shareholder vote in April and remains targeted to close by the end of Q3, pending regulatory approval.

Bottom Line: Ellison’s team delivered the kind of clean quarter Paramount needed before taking on WBD. But this was the easy part: cost cuts, better execution, and a cleaner streaming story are only the opening act. The real test begins when Paramount inherits WBD’s debt, linear decline, and integration complexity.

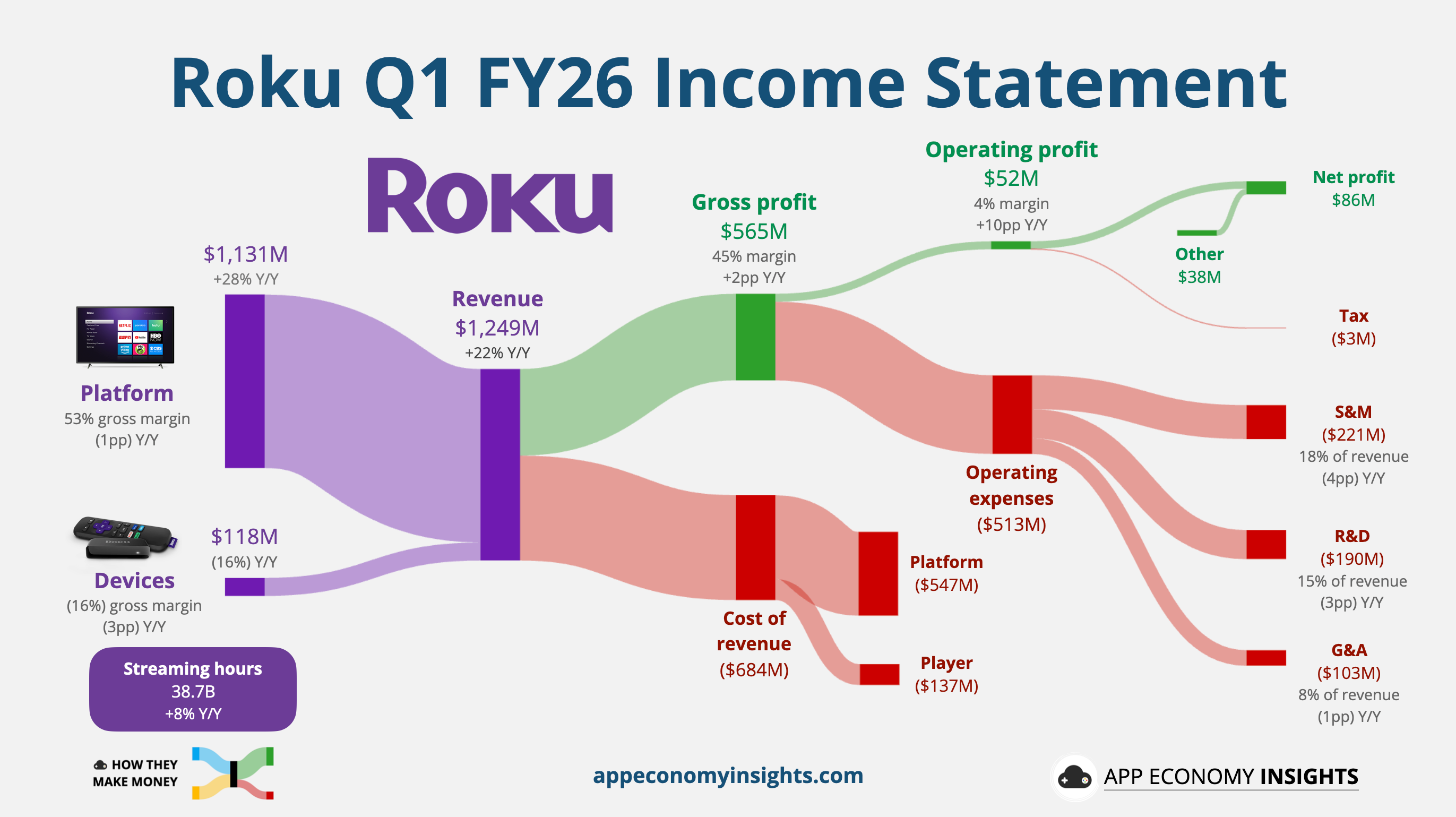

📺 Roku: The CTV Toll Booth

📸 Big picture: Revenue grew +22% Y/Y to $1.25 billion ($50 million beat), and EPS swung to a $0.57 profit ($0.24 beat) versus a $0.19 loss a year ago. Adjusted EBITDA jumped +165% to $148 million, and free cash flow hit $148 million — the second-highest on record.

📈 Platform accelerates: Platform revenue grew +28% Y/Y to $1.1 billion, lifted by the Olympics and Super Bowl. For the first time, Roku broke out Platform into two segments: Advertising revenue grew +27% to $613 million, while Subscriptions grew +30% to $519 million. Roku said its video ad growth outpaced both the broader US CTV and digital ad markets.

📉 Devices stay a loss-leader: Devices revenue fell -16% Y/Y to $118 million, with a -16% gross margin on lower player unit sales and promotional pricing. The strategy hasn’t changed: hardware exists to seed the platform.

📊 100 million households: Roku passed 100 million streaming households globally, with its devices used by more than half of all US broadband households. Streaming hours rose +8% Y/Y to 38.7 billion, and Q1 was Roku’s best quarter ever for new Premium Subscription sign-ups.

🔮 Guidance raised again: Roku lifted full-year Platform revenue guidance to ~+21%, raised adjusted EBITDA to $675 million, and reiterated the path to $1 billion in free cash flow by 2028 “if not sooner.” Q2 guidance calls for Platform revenue growth of +20% Y/Y.

Bottom Line: Roku doesn’t need to own sports rights to benefit from them. As tentpole events pull more ad dollars into connected TV, Roku acts like a toll booth on the shift. The H2 caution matters, but it sounds more macro than company-specific.

📊 Stay tuned for nearly 50 companies visualized tomorrow in our PRO coverage!

That’s it for today!

Stay healthy and invest on!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Start an account for free and save 15% on paid plans with this link.

Disclosure: I own AAPL, AMZN, GOOG, NFLX, and ROKU in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.