☁️ Amazon: The Inference Era

AWS is building the stack for agentic AI

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Three months ago, Amazon committed $200 billion in CapEx to bankroll the AI gold rush. Now AWS is selling the gold itself.

Amazon’s OpenAI deal is no longer just a financing headline. It is becoming an AWS product roadmap. OpenAI models are landing on Bedrock. Codex is moving into the AWS developer workflow. And Bedrock Managed Agents, powered by OpenAI, are designed to run production-scale agents directly on Amazon’s infrastructure.

That matters because agentic AI changes the cloud equation. Training models is one workload. Running millions of persistent agents with memory, tools, orchestration, and real-time reasoning is another.

Jassy framed the demand shift clearly:

“AI is commonly seen as a GPU story, but the rise of agentic workloads, real-time reasoning, code generation, learning, and multi-step task orchestration is driving massive CPU demand as well.”

Amazon says its chips business has topped a $20 billion annual revenue run rate, including Graviton, Trainium, and Nitro. In other words, AWS is moving up the stack with agents and down the stack with custom chips.

Now let’s see what stood out this quarter.

Today at a glance:

Amazon Q1 FY26.

AWS moves up the stack.

Key quotes from the call.

What to watch moving forward.

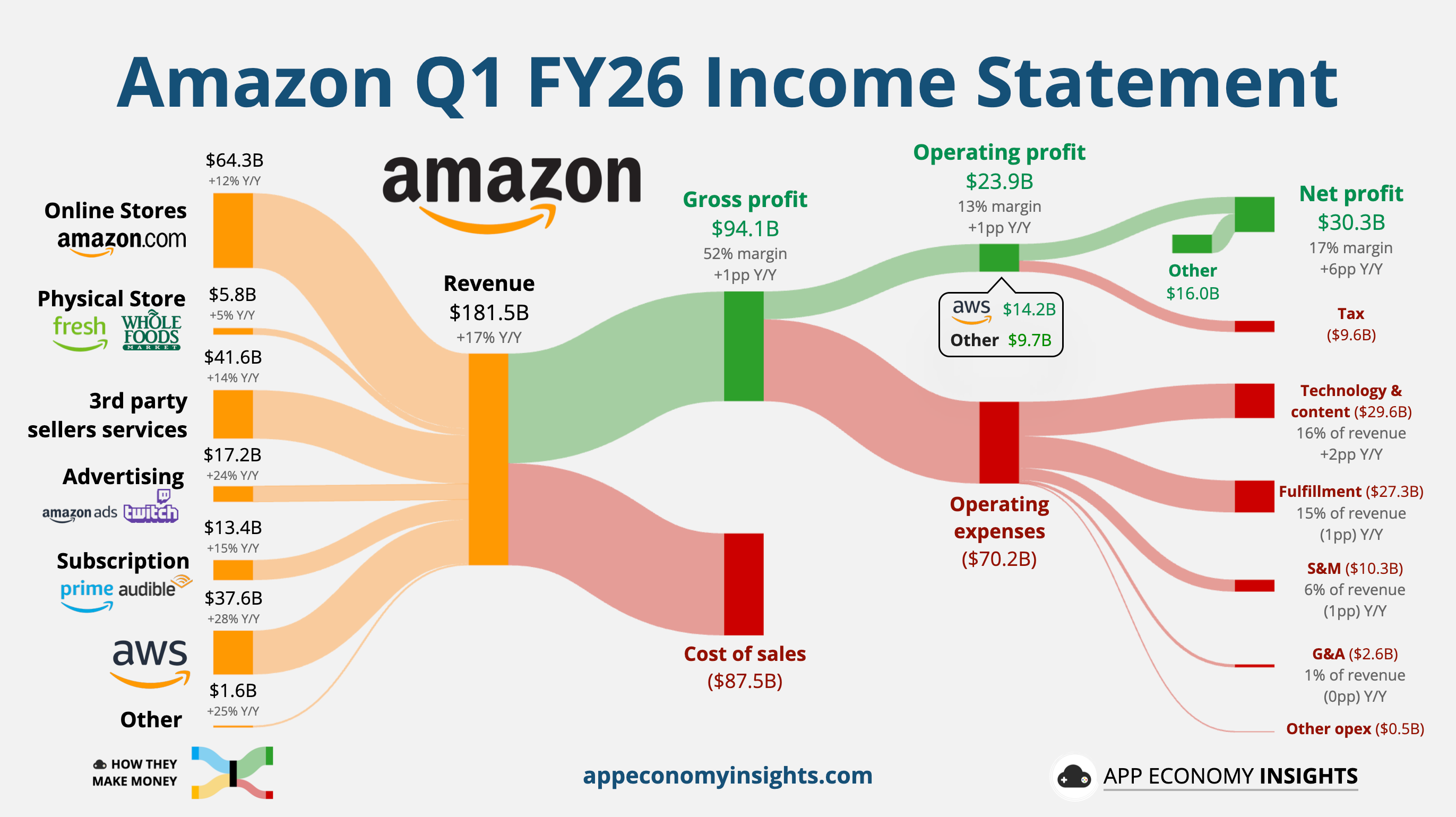

1. Amazon Q1 FY26

Income statement:

Revenue rose +17% Y/Y to $181.5 billion ($4.3 billion beat).

Gross margin was 52% (+1pp Y/Y).

Operating margin was 13% (+1pp Y/Y).

AWS: 38% margin (-2pp Y/Y).

North America: 8% margin (+2pp Y/Y).

International: 4% margin (+1pp Y/Y).

Net profit included a $16.8 billion non-operating gain from the valuation markup of Anthropic. This was triggered by the $30 billion Series G round in February, which established a new valuation benchmark of $380 billion. Amazon recently doubled down on its investment as we covered here.

Cash flow:

Operating cash flow TTM was $148.5 billion (+30% Y/Y).

Free cash flow TTM was $1.2 billion (-95% Y/Y), driven by the operating cash flow growth, offset by a 67% rise in Capex to $147.3 billion.

Balance sheet:

Cash, cash equivalent, and marketable securities: $143 billion.

Long-term debt: $119 billion.

Q2 FY26 Guidance:

Revenue +16% to 19% Y/Y.

Operating income ~$22 billion or +15% Y/Y in the mid-range.

So, what to make of all this?

☁️ AWS accelerates: AWS revenue grew 28% Y/Y to $37.6 billion, its fastest growth in 15 quarters and a clear step-up from 24% last quarter. Operating income reached $14.2 billion, implying a nearly 38% margin, while Amazon’s chips business topped a $20 billion revenue run rate (annualized) and is growing triple digits. AWS is finally showing the AI acceleration investors were waiting for.

💵 The AI bill comes due: Free cash flow collapsed to just $1 billion over the past 12 months, down from $26 billion a year ago, as Amazon doubled down on AI infrastructure. It will stay that way as management still expects roughly $200 billion of CapEx in 2026, mostly tied to AWS, AI, chips, robotics, and satellites. Jassy’s message is simple: near-term cash flow takes the hit, but these assets should monetize for decades. It’s still ‘Day 1’ after all.

📦 Retail is still compounding quietly: North America revenue grew 12% to $104.1 billion, with the operating margin for the region improving to 8%. Worldwide paid units grew 15%, the fastest pace since the COVID lockdown era, and Amazon has already delivered more than 1 billion same-day or overnight items in 2026.

📢 Advertising keeps climbing: Advertising revenue accelerated 24% Y/Y to $17.2 billion, pushing the business to $72 billion in revenue in the trailing 12 months. This remains one of Amazon’s cleanest margin levers, benefiting from sponsored ads, video ads, and Prime Video monetization. The more Amazon grows retail volume and Prime engagement, the larger the ad flywheel gets.

🔮 Guidance says growth first, margins second: Q2 guidance calls for revenue to grow 16% to 19% Y/Y, with operating income rising 15% in the mid-range. It reflects the strong demand, but also the continued pressure from new bets and infrastructure spending.

2. AWS moves up the stack

👔 From infrastructure to software

Amazon is moving up the stack to compete for the enterprise seat. With agents, Amazon wants AWS to own the workflow layer.

Amazon Quick: This is the front-end service. It’s a unified AI workspace for Business Intelligence, research, and task automation. At $20/user/month, it is a direct, cheaper alternative to Microsoft’s Copilot.

Connect Suite: Think of Connect as the operational engine. Amazon has expanded Connect from a contact center tool into four agentic pillars: Customer, Decisions, Talent, and Health.

By bundling these agentic services into existing AWS accounts, Jassy wants to make AWS the operational OS of the company, significantly raising switching costs and driving high-margin SaaS revenue.

🧠 OpenAI lands on Bedrock

As of this week, the latest OpenAI frontier models and Codex are officially in limited preview on Amazon Bedrock. OpenAI has committed to spending $100 billion on AWS over eight years and using 2 gigawatts of power specifically for Amazon’s Trainium chips.

Codex integration: Bringing Codex (with its 4 million weekly users) into the AWS environment allows developers to build and deploy agents without ever leaving the Amazon ecosystem.

Bedrock Managed Agents: This service provides a managed harness for OpenAI models to handle memory, tool orchestration, and long-running tasks. By providing the orchestration layer, Amazon ensures the business logic stays within the AWS perimeter.

Amazon wants to become the Switzerland of enterprise AI. By hosting OpenAI alongside Anthropic and Meta, Jassy is ensuring that no matter which model wins, the infrastructure, security, and data reside on AWS.

3. Key quotes from the earnings call

Check out the earnings call transcript on Fiscal.ai here.

Andy Jassy on custom silicon:

“If our chips business was a standalone business and sold chips produced this year to AWS and other third parties as other leading chip companies do, our annual revenue run rate would be $50 billion. As best as we can tell, our custom silicon business is now one of the top three data center chip businesses in the world.”

A $50 billion standalone run rate would place Amazon's silicon arm in elite company — behind only NVIDIA and Broadcom in data center chip revenue. The $225 billion Trainium backlog, with Trainium2 sold out and Trainium3 nearly fully subscribed, is what gives Jassy room to speak with such confidence. A decade of vertical integration is now the moat that makes Bedrock price-competitive against pure NVIDIA stacks.

On the future of agents

“I think the future of using these models is a stateful model, a stateful API. [...] The Bedrock managed agents that we collaborated with and invented with OpenAI [...] I think that is the future of how these agents are going to be built. It is something that nobody else has.”

Stateless inference is a commodity. Stateful runtime is a platform. Jassy is staking the next phase of Bedrock on the bet that enterprise AI will live inside persistent, multi-step agent sessions — and that running those sessions inside AWS will be stickier than swapping models behind a chatbot. If he's right, OpenAI on Bedrock is less about access to GPT-5 and more about who owns the agent runtime.

On the memory shortage:

“One of the interesting things that we see right now with the change in price and supply on things like memory is that it is a further impetus pushing companies who have on-premises infrastructure into the cloud. [...] We have seen a number of conversations we have been having with enterprises for many months—where it has just been slower in getting the transformation plan to move to the cloud—accelerate rapidly just because we have a lot more supply than what others have.”

The memory squeeze is doing AWS a favor. Growth accelerated to its fastest pace in 15 quarters — and one underrated reason is that hyperscalers got priority allocation from suppliers while on-prem buyers were left waiting. A supply shock is converting wait-and-see migration plans into signed contracts.

On AI inside Amazon:

“If you look at one of our services, we swapped out the engine of the service while we were also running the service full tilt. Normally, that would have taken 40 or 50 people about a year to do. We took five really smart, AI-forward-thinking people building on agentic coding tools, and those five people rebuilt it in 65 days.”

That ratio explains Amazon’s broader efficiency push in plain English: more software shipped with fewer engineers. It explains Project Dawn's 30,000 corporate layoffs.

4. What to watch moving forward

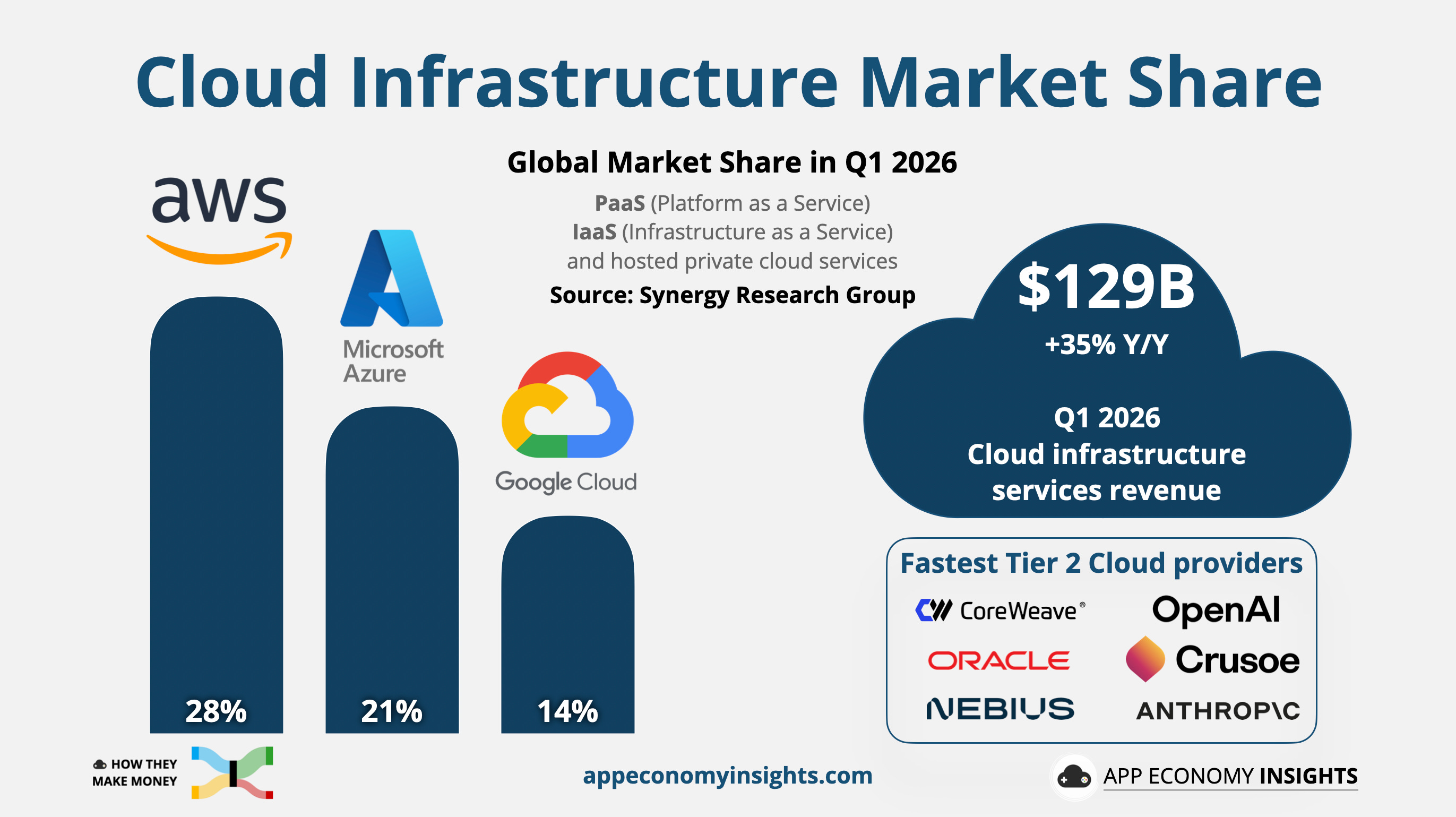

☁️ AWS market share and margins

Total cloud infrastructure market spending grew by 35% Y/Y to $129 billion in Q1 2026, the ninth consecutive quarter of accelerating growth. Synergy Research Group estimates it was the fastest growth since 2021.

AWS maintained its leading 28% market share, compared to 21% for Microsoft Azure and 14% for Google Cloud.

All hyperscalers remain supply-constrained, so I try to refrain from analyzing the quarter-to-quarter changes too closely. But it’s hard not to notice a clear inflection point for Google Cloud (with TPUs playing a role) and impressive acceleration for AWS at this scale (boosted by Trainium), while Azure growth has plateaued.

🧠 Challenging NVIDIA

Jassy disclosed that the custom silicon portfolio (Graviton, Trainium, Nitro) has reached a $20 billion annual revenue run rate (or $50 billion if AWS were counted as a customer).

Triple-digit growth: If this trajectory holds, the chips business could approach a $25–$30 billion run rate by year-end.

Meta Catalyst: Meta’s recent multibillion-dollar deal for tens of millions of Graviton5 cores (CPUs) validates the scale. While Meta is building its own chips (MTIA), its reliance on Graviton for general-purpose compute shows that Amazon’s vertical integration is a structural cost advantage Meta can’t ignore.

NVIDIA pricing power: As Trainium3 (the new 3nm chip) becomes fully subscribed, AWS can offer AI training at a 30-40% lower cost than NVIDIA-based instances. If Trainium3 delivers the promised price-performance advantage, AWS can pressure NVIDIA pricing inside its own ecosystem.

Jeff Bezos famously said, “Your margin is my opportunity.” This playbook can apply to the chip business, as most Fortune 500 companies optimize their cost per token.

🏗️ The CapEx Payoff

In Q1 2026, the leading hyperscalers (Google, Microsoft, dAmazon, Meta) grew their trailing-12-month operating cash flow by 30% to $617 billion.

This represents the cash engine they can tap to fund the AI CapEx ramp without leaning on leverage. Amazon has even more flexibility because it continues to avoid stock buybacks and dividend payments.

The CapEx ramp is likely to keep absorbing more of that cash flow in the coming quarters, compressing free cash flow toward zero.

To be sure, that will spook some investors. But the rising backlogs and untapped opportunities suggest the bigger mistake would be failing to seize the moment.

Amazon is spending like crazy, but the spend is not random. AWS is building the stack for enterprise AI: custom chips underneath, Bedrock as the model layer, and managed agents on top. The free cash flow hit is real, but so is the strategic logic.

That’s it for today!

Stay healthy and invest on!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Start an account for free and save 15% on paid plans with this link.

Disclosure: I am long AMZN, GOOG, and META in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.

You describe the shift toward inference as a kind of structural inevitability —

one that justifies the scale of investment, infrastructure, and expansion.

And yet, the more persistent and embedded these systems become,

the more important it is to ask not only what they enable,

but what guides their direction.

Inference, at scale, is continuous action.

But action alone is not judgment.

And without judgment, even the most powerful infrastructures risk advancing

without a clear understanding of what they are ultimately shaping.

— A voice across time: Hannah Arendt