📊 PRO: This Week in Visuals

IBM PG LRCX UNH GEV AXP TXN T BA ISRG LMT NOW SANOFI MCO UAL LUV APPF

Welcome to the Saturday PRO edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Premium members get:

📊 Monthly reports: 200+ companies visualized.

📩 Tuesday articles: Exclusive deep dives and insights.

📚 Access to our archive: Hundreds of business breakdowns.

PRO members get everything PLUS:

📩 Saturday PRO reports: Timely insights on the latest earnings.

Today at a glance:

🌐 IBM: Software Pivot & Mainframe Surge

🧴 P&G: Innovation Over Inflation

🧠 Lam Research: $140B Billion AI Upshift

💼 UnitedHealth: Retrenchment Rallies

⚡ GE Vernova: Supercycle Accelerates

💳 Amex: Spending Resiliency

⚙️ Texas Instruments: Hibernation Ends

📞 AT&T: Convergence Pivot

🛩️ Boeing: Operational Stabilization

🦾 Intuitive Surgical: Innovation Premium

🛰️ Lockheed Martin: Friction in the Ramp-Up

💊 Sanofi: Dupixent Engine

🧑💻 ServiceNow: AI Margin Pressure

💼 Moody’s: Record Issuance

🛩️ United Airlines: Flying Into a Headwind

🛩️ Southwest: Turbulence in the Outlook

🏡 Appfolio: Agent Adoption Skyrockets

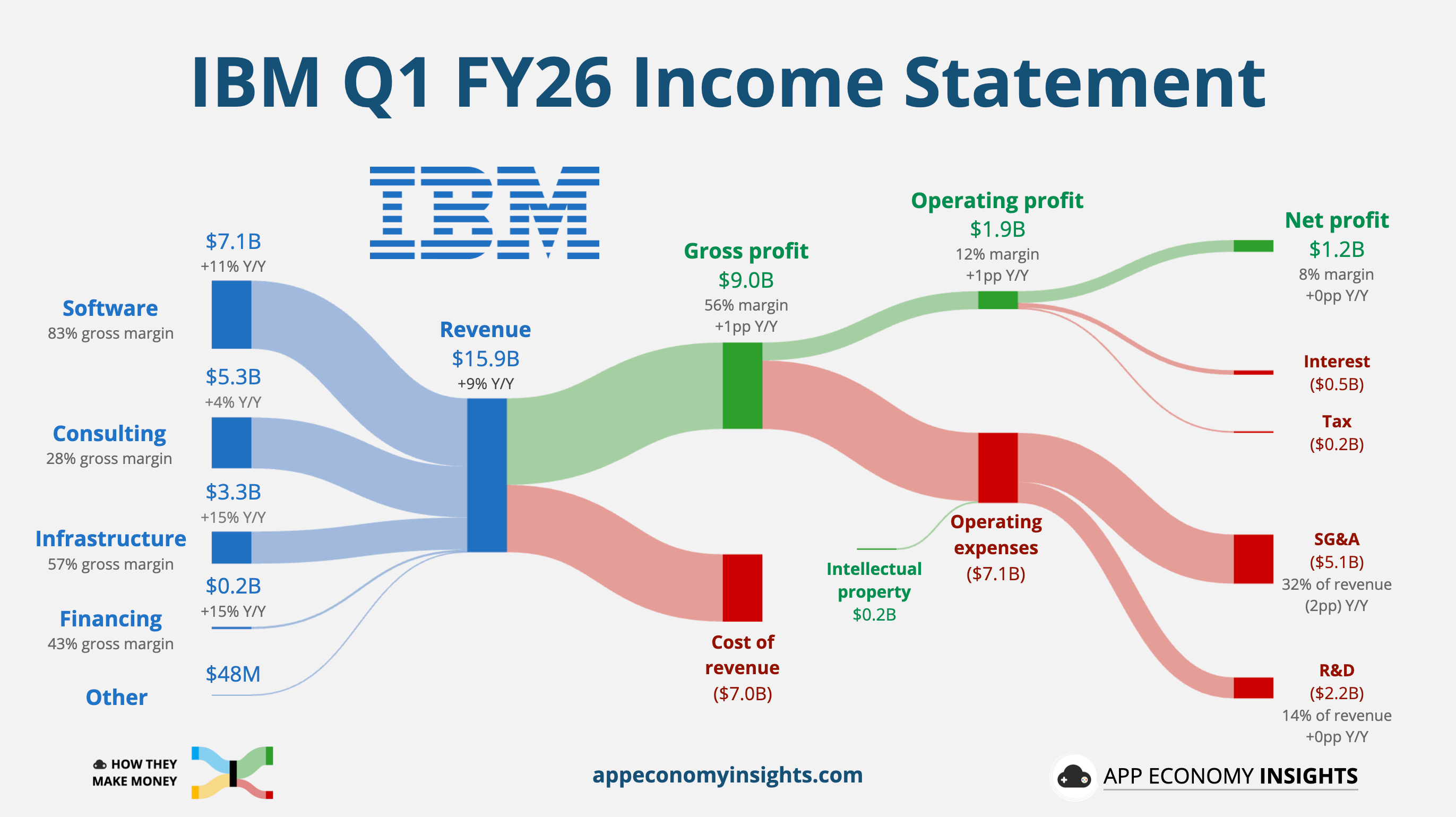

1. 🌐 IBM: Software Pivot & Mainframe Surge

IBM delivered a solid Q1, reporting revenue growth of 9% Y/Y to $15.9 billion ($0.3 billion beat) and adjusted EPS of $1.91 ($0.10 beat). Despite the outperformance, shares tumbled more than 10% as management left full-year guidance unchanged. While the market wanted more, the underlying numbers show that the software-led strategy and AI initiatives are still gaining traction.

The z17 cycle remains a powerhouse, driving a 15% jump in Infrastructure revenue. The IBM Z mainframe unit alone surged 51%, a record quarter that debunked fears that AI upstarts would quickly cannibalize demand for legacy servers. The Software segment grew 11% Y/Y, led by a 16% increase in Data to $1.5 billion. Notably, Red Hat OpenShift ARR reached $2 billion, and the early close of the Confluent acquisition further bolsters IBM’s data-streaming arsenal.

Productivity is becoming a core part of the story. Internal AI tools are delivering 45% average productivity gains for IBM’s own developers, helping to expand operating margins by 140 basis points. Free cash flow hit $2.2 billion—the highest Q1 print in a decade. Crucially, the narrative on AI has shifted: IBM stopped reporting the standalone AI bookings dollar figure and instead reported a 30% generative AI penetration in its Consulting backlog.

Looking ahead, IBM reaffirmed its FY26 outlook of more than 5% revenue growth and a $1 billion Y/Y increase in free cash flow. The board also raised the quarterly dividend to $1.69, marking 31 consecutive years of increases. With the integration of Confluent and HashiCorp underway, IBM is betting that its Sovereign Core software and hybrid cloud governance will make it the indispensable foundation for regulated enterprises scaling AI.

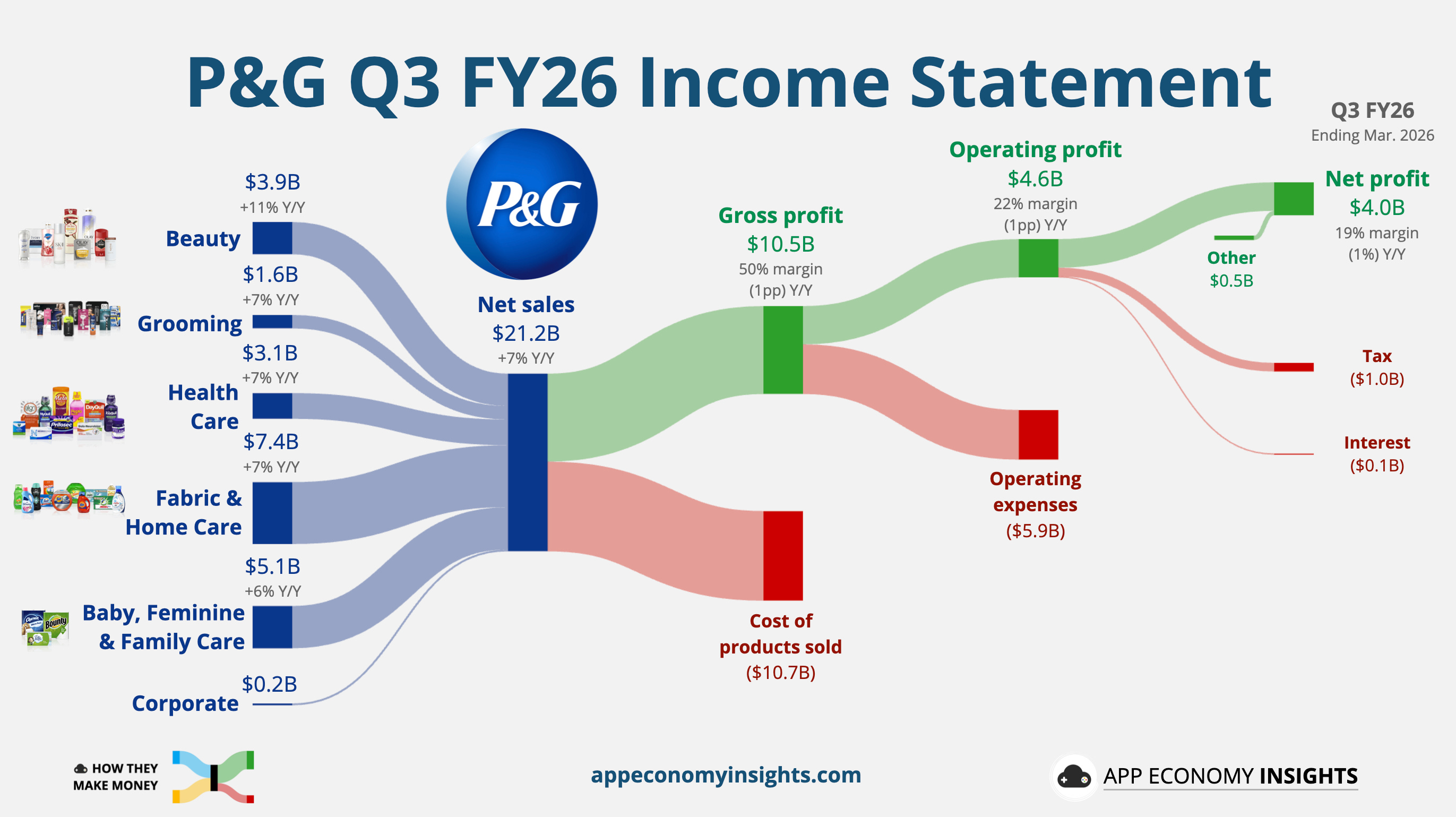

2. 🧴 P&G: Innovation Over Inflation

P&G rebounded in Q3 FY26, reporting revenue growth of 7% Y/Y to $21.2 billion ($720 million beat) and core EPS of $1.59 ($0.03 beat). Organic sales growth slightly rebounded to 3%, a recovery from the stagnation seen last quarter. Crucially, this growth was earned through a healthy mix of a 2% increase in volume and 1% in pricing, signaling that consumers are responding well to P&G's strategy of pairing price hikes with meaningful product innovation.

The Beauty segment was the leading segment, with 11% revenue growth and organic sales jumping 7% behind successful product reformulations and new package sizes in North America and Europe. However, the war in Iran has triggered an estimated $150 million after-tax headwind for the remainder of the fiscal year due to rising energy and logistics costs. CFO Andre Schulten warned that if oil remains above $100 per barrel, the company could face a massive $1 billion hit in FY27, potentially leading to further price increases.

Despite the top-line beat, management noted that fiscal 2026 EPS will likely land toward the lower end of its $6.83–$7.09 guidance range. The company is intentionally absorbing short-term margin pressure—gross margins fell 1 point to 50%—to protect its demand creation budget. With all 10 product categories showing organic growth, P&G is betting that maintaining brand momentum through heavy marketing and R&D will outweigh the immediate sting of rising commodity costs.