📊 PRO: This Week in Visuals

TSM ASML JNJ MS GS PEP ABT SCHW BLK

Welcome to the Saturday PRO edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Premium members get:

📊 Monthly reports: 200+ companies visualized.

📩 Tuesday articles: Exclusive deep dives and insights.

📚 Access to our archive: Hundreds of business breakdowns.

PRO members get everything PLUS:

📩 Saturday PRO reports: Timely insights on the latest earnings.

Today at a glance:

⚡️ TSMC: Agentic Shift Acceleration

🔬 ASML: AI Demand Boosts Outlook

💊 J&J: Oncology Powers Guidance

👔 Morgan Stanley: Record Trading

🏛️ Goldman Sachs: Equities Hit Records

🥤 PepsiCo: Snack Volume Returns

🧬 Abbott: Strategic Reset

🏦 Schwab: Trading Records

📈 Blackrock: iShares Momentum

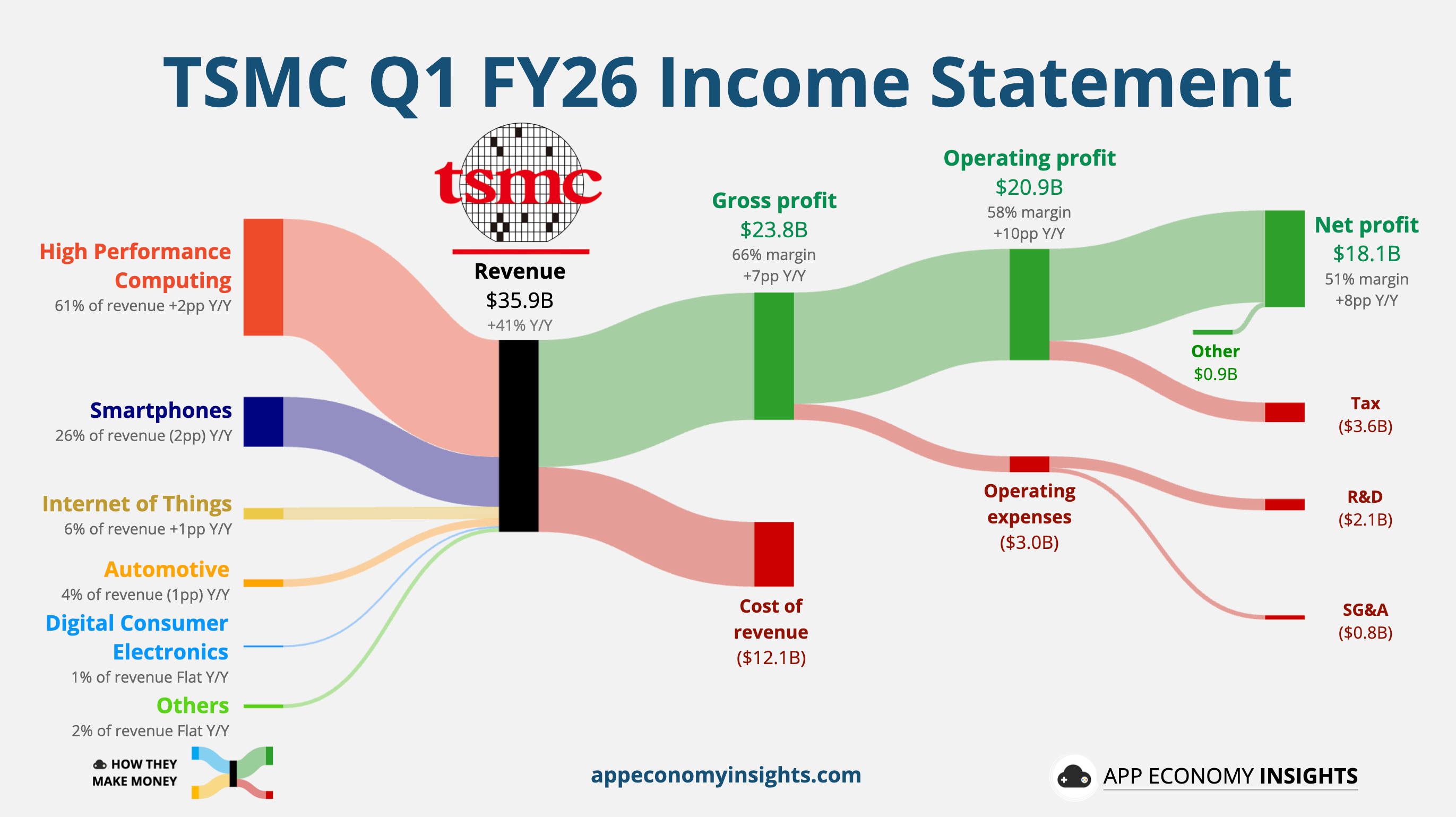

1. ⚡️ TSMC: Agentic Shift Acceleration

TSMC’s Q1 FY26 results reflected a massive transition, as demand for AI infrastructure moved from speculation to concrete financial gains. Revenue skyrocketed 41% Y/Y to $35.9 billion ($0.4 billion beat), while net income surged 58%. Management raised its full-year 2026 revenue growth forecast to above 30%, up from the previous ~30% target.

Gross margins expanded to a staggering 66%, far exceeding the analyst consensus of 64.5%. CEO C.C. Wei noted that the industry is moving beyond generative AI into agentic AI—where platforms perform actions rather than just answering queries—leading to a step-up in chip demand that shows no sign of cooling.

TSMC’s dominance is now almost entirely tied to its most advanced leading-edge technologies. Chips made with 7nm or smaller nodes accounted for 74% of total wafer revenue. The high-performance computing (HPC) segment, which houses the powerhouse AI chips for NVIDIA and AMD, now accounts for 61% of total revenue. That compares to just 41% four years ago.

While the 3nm ramp-up continues to accelerate (now 25% of revenue), management is keeping its foot on the gas. Capital expenditure is trending toward the top end of the $52–$56 billion range for 2026. This aggressive spending serves as a warning shot to rivals like Intel. C.C. Wei pointedly remarked that there are “no shortcuts” to foundry leadership, emphasizing that manufacturing excellence and customer trust cannot be bought overnight.

Despite the blowout numbers, shares dipped slightly as investors digested potential macro risks. CFO Wendell Huang acknowledged that the conflict in the Middle East could drive up costs for specialized chemicals and gases, such as helium. While it is “too early to quantify” the exact impact on profitability, management remains confident in their supply chain resiliency and energy stability in Taiwan.

TSMC is also doubling down on its global footprint, with total US investment pledges now reaching $165 billion. As the firm prepares for a sequential 10% revenue jump in Q2, the narrative is clear: TSMC is the indispensable foundation of the AI era, and for now, its fabs are running hot with no significant competition in sight through the end of the decade.

Check out the earnings call transcript on Fiscal.ai here.

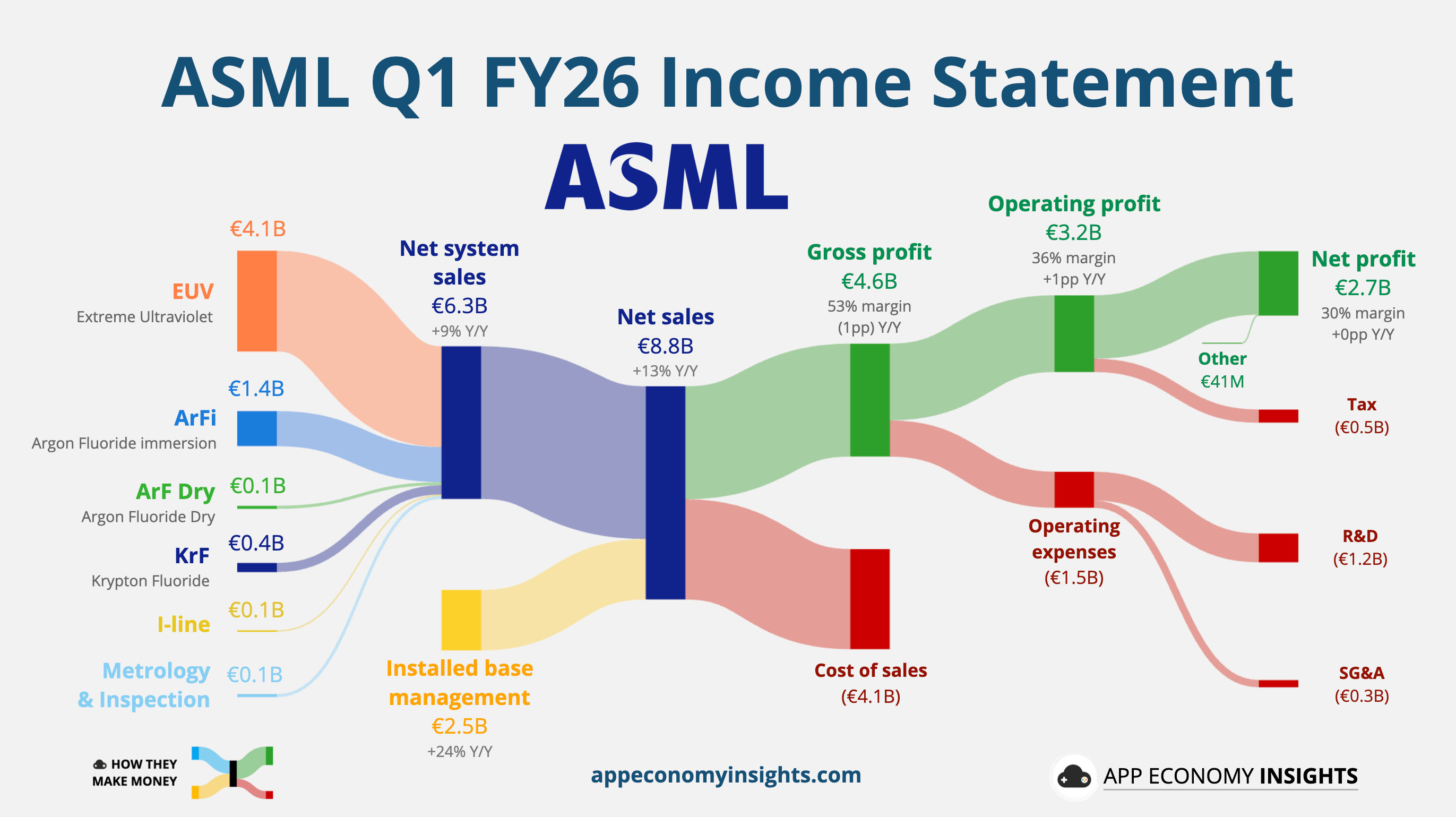

2. 🔬 ASML: AI Demand Boosts Outlook

ASML kicked off Q1 2026 with a solid beat, proving that the semiconductor industry’s lithography intensity is only increasing. Revenue rose 13% Y/Y to €8.8 billion (€110 million beat), while GAAP EPS of €7.15 comfortably topped estimates. Citing an insatiable appetite for AI infrastructure, management raised and narrowed its full-year 2026 sales guidance to €36-€40 billion (an improvement from €34-€39 billion previously).

The quarter’s bottom line was particularly robust, with a 53% gross margin that exceeded guidance. This was driven by a strong mix in the Installed Base business, where customers are paying for upgrades and services to squeeze more capacity out of existing tools while waiting for new systems to arrive.

The narrative remains dominated by demand for EUV (Extreme Ultraviolet). CEO Christophe Fouquet noted that customers are “sold out for 2026” and that ASML is racing to ensure it isn’t responsible for the bottleneck in global chip production. The firm expects to ship at least 60 Low NA EUV systems this year and has already mapped out a path to 80 units in 2027. Surprisingly, the older Immersion DUV business also showed resilience; previously expected to decline due to China trade tensions, demand has turned flattish as chipmakers potentially accelerate purchases ahead of new export curbs.

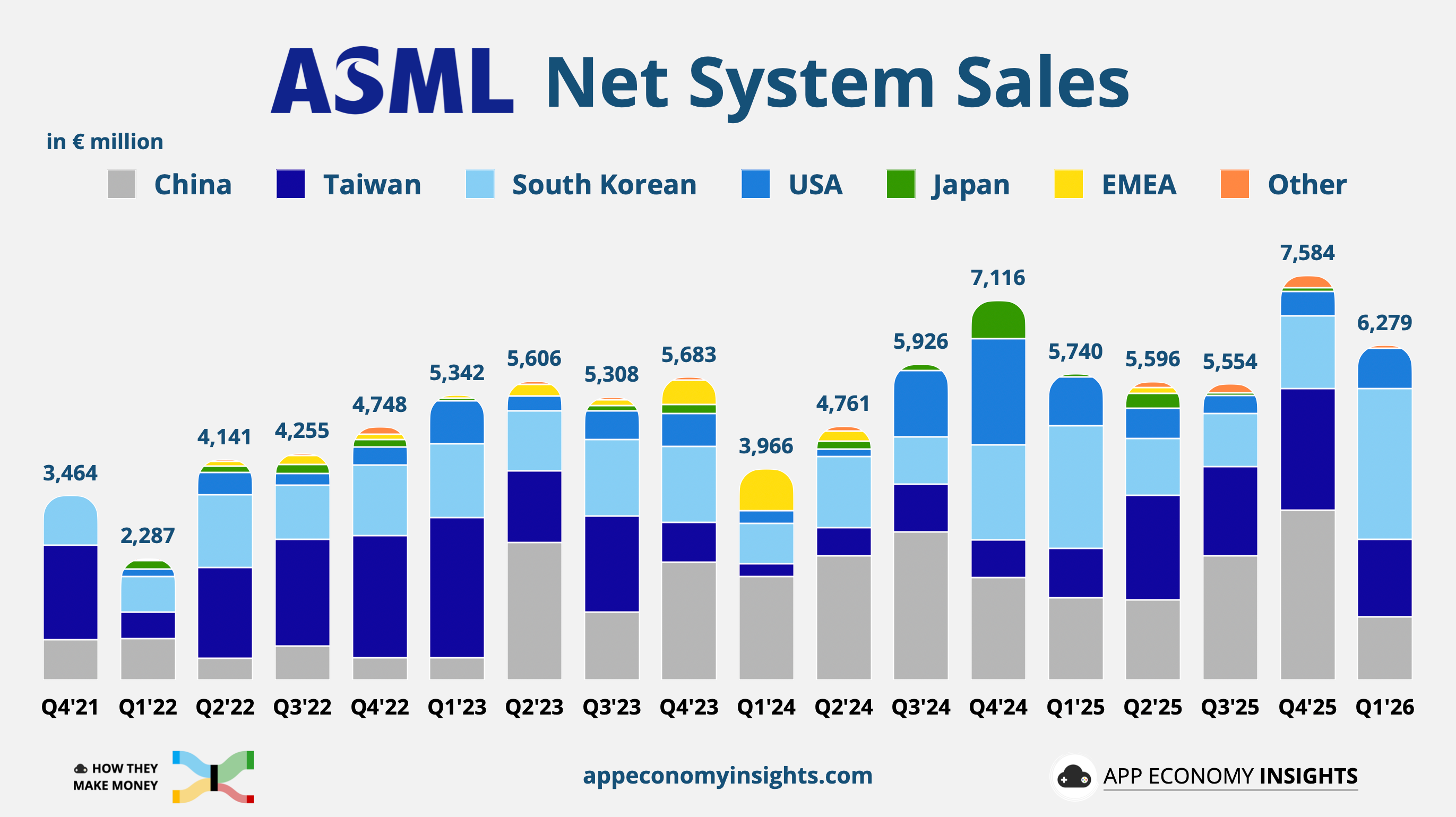

Geopolitics remains the primary overhang. China’s share of system sales dropped to 19% this quarter (down from 36% in Q4), aligning with management’s long-term target of 20%. While US lawmakers recently introduced the MATCH Act to further restrict equipment sales and servicing, management asserted that their new guidance range can “accommodate potential outcomes” of these export discussions. Despite the raised outlook, shares dipped 5% on the news as a slightly soft Q2 revenue guide of €8.4–€9.0 billion fell just shy of lofty analyst expectations for the bridge into the year’s second half.