🍿 Netflix: Life After Warner

The growth story shifts to ads and pricing power

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Netflix walked away from the Warner Bros. Discovery merger in February, avoiding a bidding war with Paramount Skydance. Investors initially cheered the discipline, and the failed deal delivered a $2.8 billion breakup fee that boosted Q1 results.

That relief didn’t last. Shares fell nearly 9% after earnings, as investors looked past the windfall and focused on what comes next: a business that now has to justify its premium valuation through price hikes, ad-tier scaling, and internal efficiency.

Its unchanged 13% revenue growth outlook for 2026 implies slower momentum from here. Now that the M&A shortcut is gone, Netflix must prove it can build the next leg of growth on its own.

Today at a glance:

🍿 Netflix Q1 FY26

🎯 3 Strategic Priorities

📈 Streaming Market Share

🛰️ Amazon: Buying the Spectrum

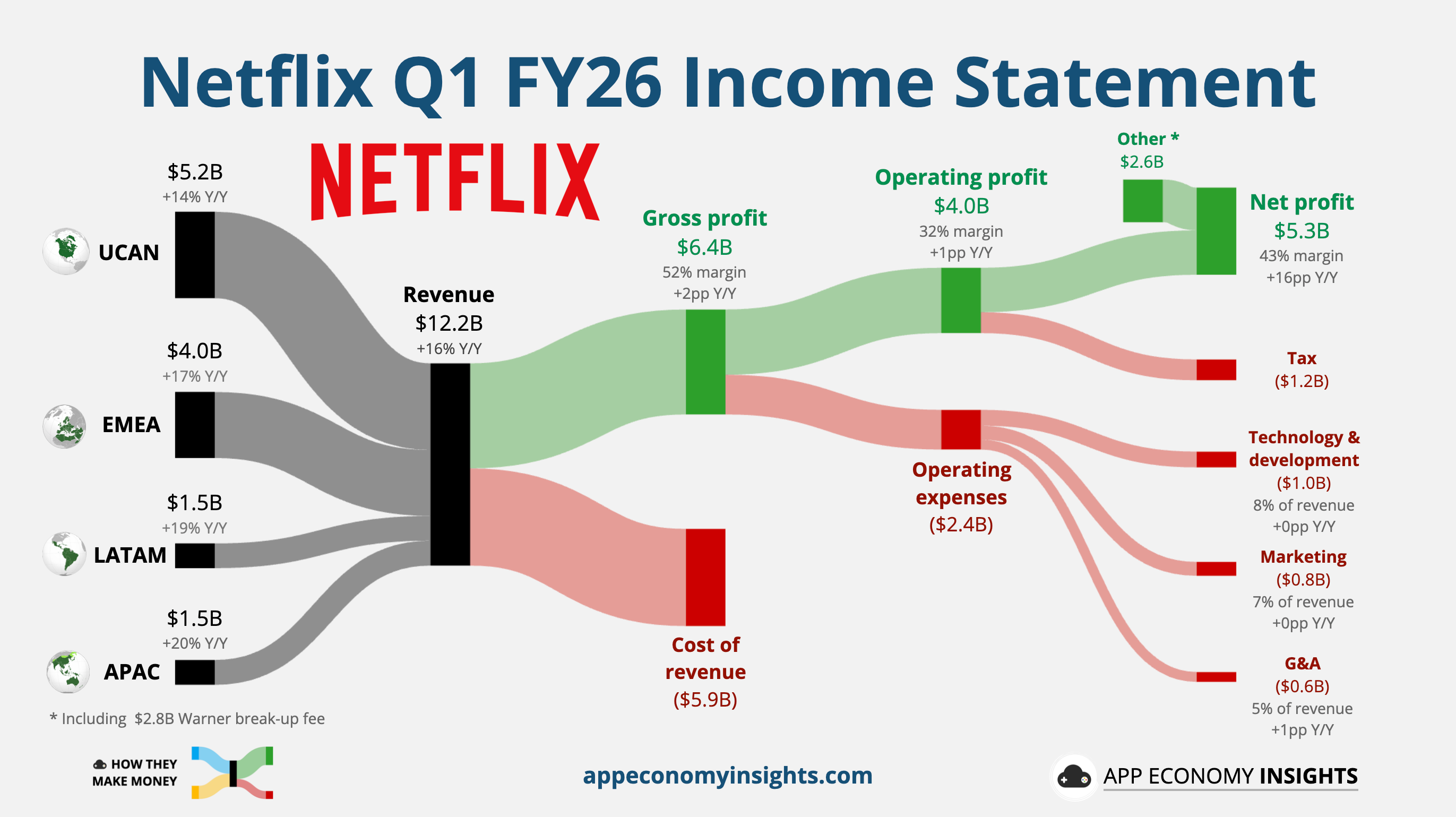

🍿 Netflix Q1 FY26

Income statement:

Revenue +16% Y/Y to $12.2 billion ($80 million beat).

Operating margin 32% (+1pp Y/Y).

EPS $1.23 ($0.11 miss).

Termination fee of $2.8 billion included in ‘other income’ (see visual).

Balance sheet:

Cash and short-term investments: $12.3 billion.

Debt: $14.4 billion.

FY26 guidance (unchanged):

Revenue +12%-14% to ~$51.2 billion.

Operating margin 31.5% (+2pp Y/Y).

So, what to make of all this?

📈 Top-line momentum: Revenue rose 16% Y/Y and was slightly ahead of expectations. While Netflix no longer provides subscriber counts, management attributed the beat to slightly higher-than-planned membership growth. The growth was global, with Latin America (+19%) and Asia-Pacific (+20%) growing the fastest.

📢 Ads on track: The advertising segment remains a primary growth engine. Netflix reiterated its projection for ad sales to double to ~$3 billion in 2026. This trajectory is essential to the multi-tier strategy, serving as a safety net against churn as inflation pressures consumers to cut back on non-essentials.

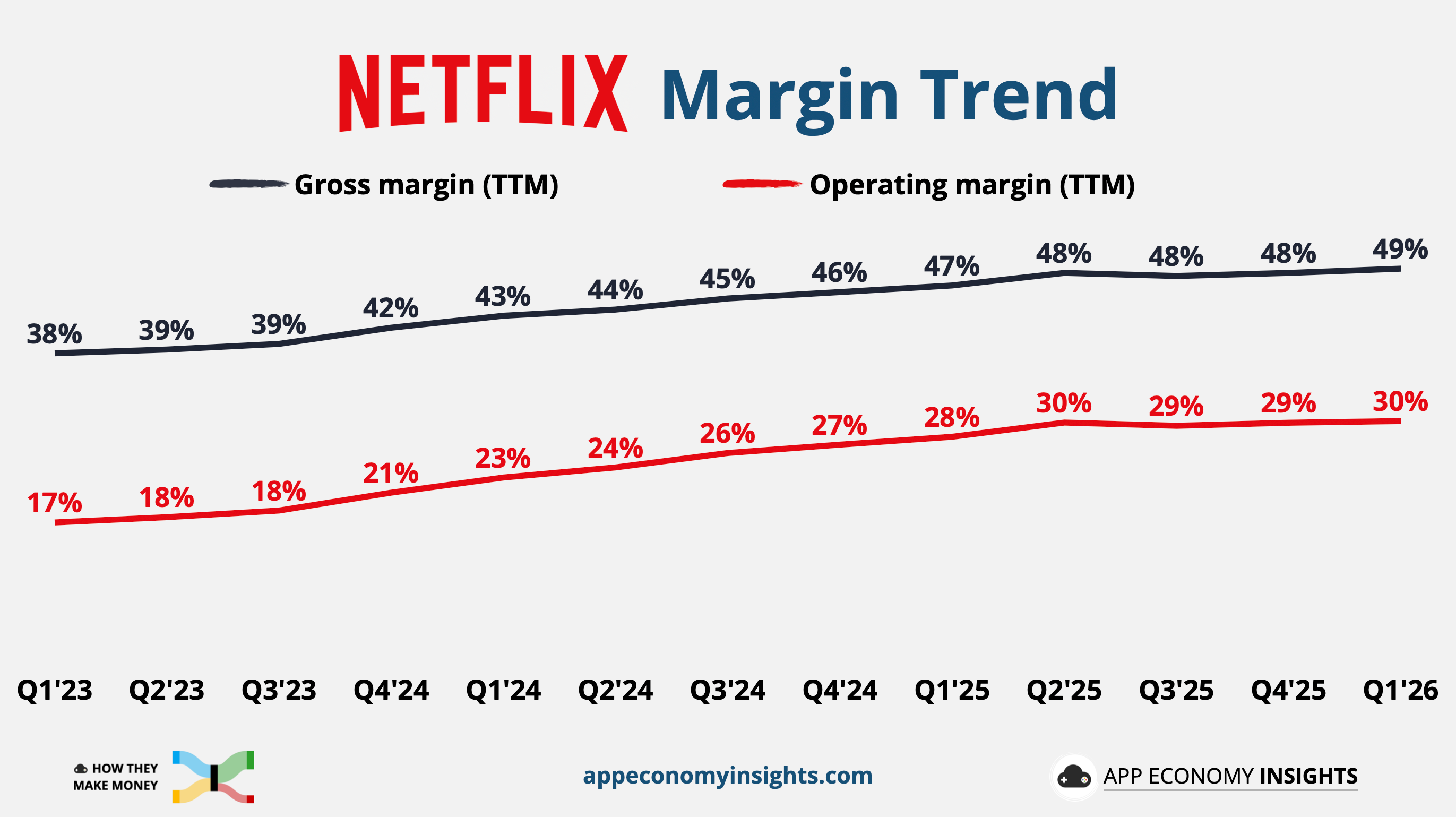

📉 Cautious Q2 guidance: Management guided for an operating margin of 32.6%, a 150bp decline Y/Y. The softer outlook reflects front-loaded content amortization, with margin expansion expected to resume in the second half. Netflix has been a story of steady margin expansion if we zoom out.

🏷️ Price increase kicks in: In March, Netflix hiked the price of its standard ad-free plan by $2 to $20/month. Since this was announced late in Q1, the financial impact was not reflected in these results but is expected to be a primary driver of revenue growth in the coming quarters.

👔 End of an era: Co-founder Reed Hastings announced he will step down from the board in June after 29 years. His departure marks the final transition to the Ted-and-Greg era of leadership. Symbolically, it reinforces that Netflix is now being judged less as a visionary disruptor and more as a scaled media platform expected to deliver steady growth and disciplined returns.

🎯 3 Strategic Priorities

Netflix is evolving into a diversified entertainment ecosystem. To compete with legacy media conglomerates and social apps like TikTok or YouTube, management is focusing on three fronts:

Content: Netflix is expanding beyond binge-worthy series to capture more “moments of truth.” Live events drove record sign-ups in Japan this quarter, while podcasts and games aim to make Netflix more of a regular destination rather than a weekend-only app.

Technology: Management is leaning on AI to improve efficiency and discovery. The acquisition of Ben Affleck’s AI startup, InterPositive, suggests Netflix wants to give filmmakers AI-powered production tools. On the consumer side, a vertical video discovery feed with TikTok-like browsing is coming later this month.

Monetization: Ads and pricing work together. The ad tier now drives 60% of new sign-ups, giving Netflix a lower-cost entry point, more room for targeted third-party bundling, and more flexibility to raise prices elsewhere.

Bottom line: Ads and pricing can support low double-digit growth, but investors may still want clearer evidence that Netflix’s rising content spend is generating the kind of returns that justify its premium multiple (well above 30x forward earnings).

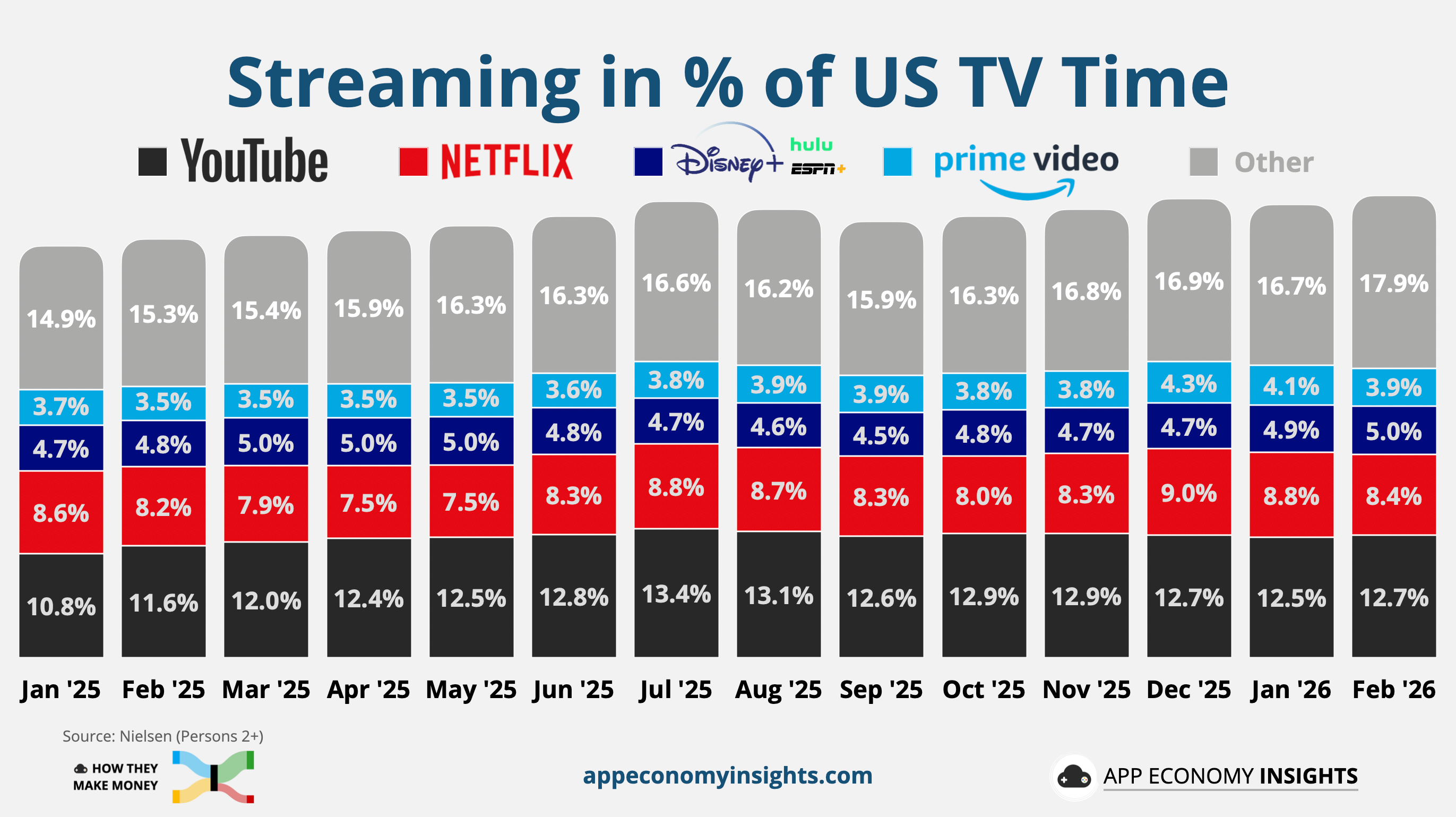

📈 Streaming Market Share

According to Nielsen, streaming accounted for 48% of US TV time in February, up from 43.5% a year ago and at an all-time high. The growth came at the direct expense of cable, which fell to a 20% share, down from 23% a year ago.

Netflix captured 8.4% of US TV time in February, slightly up from 8.2% a year ago. This somewhat flattish engagement has become a regular topic on the earnings calls. But co-CEO Greg Peters often points to retention as a better metric than hours watched to evaluate Netflix’s ability to steadily raise prices.

Warner + Paramount (part of ‘Other’) remained small at 3.4% market share in February if we combined them (+0.9pp Y/Y).

Peacock was a big winner in February, with 3.0% market share (up 2X from a year ago), thanks to the trifecta of Super Bowl LX, the Milan Cortina Winter Olympics, and the NBA All-Star Weekend. But these are one-off major sports events, and the share boost is likely to be short-lived. This is textbook cable-stealing, and not at the expense of other streamers.

YouTube remains the streaming king, with a 12.7% share of US TV time, up from 11.6% a year ago, but still below its July 2025 peak.

🛰️ Amazon: Buying the Spectrum

Amazon has spent years—and billions—trying to catch up to SpaceX in the low Earth orbit (LEO) satellite race. While Elon Musk’s Starlink already has a massive head start with 10,000 satellites, Amazon Leo is shifting its strategy from raw scale to strategic integration. Following a major partnership to bring Wi-Fi to Delta Air Lines, Amazon is now moving from the cockpit to the pocket.

Amazon’s $11.6 billion acquisition of Globalstar is a definitive play for the signal in your smartphone. By swallowing the satellite operator, Amazon is buying a regulatory shortcut to challenge Starlink’s direct-to-device (D2D) dominance, with plans to launch its own consumer service by 2028.

Why Globalstar?

The disparity in orbit remains massive: SpaceX has roughly 10,000 satellites to Amazon’s ~265 today.

However, Globalstar provides two things Amazon couldn’t get quickly:

Buying the spectrum: Access to radio frequency licenses that allow satellites to talk directly to unmodified smartphones.

Securing the customer: A “long and proven track record” with Apple, which uses Globalstar for its Emergency SOS features.

Ben Thompson notes that this deal might be less about Amazon becoming a phone company and more about Apple vs. Musk. In his view, Apple likely "made this deal happen" to avoid being forced to negotiate with SpaceX and to maintain control over its ecosystem. For Amazon, it's a win-win: they deepen their AWS relationship with Apple while gaining the infrastructure to track their own global logistics and drone fleets.

Why the Middling Assets Matter

Critics point out that Globalstar’s 24 satellites are aging “bent-pipe” relays—technology that simply bounces a signal without processing it. But for Amazon, the satellites are disposable; the regulatory rights are eternal.

Aparna Venkatesan, astronomy professor at the University of San Francisco, explained to Wired:

“It’s tapping into this package of already preapproved global spectrum rights [...] it’s going to get connected to this huge iPhone market. So I think that’s a very compelling business package.”

Bottom line: Starlink is building the fastest, largest network. Amazon is building the most integrated ecosystem. By controlling the spectrum that powers the iPhone's safety features, Amazon ensures that even if it loses the numbers game in space, it remains an essential service on the ground.

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own AMZN, META, and NFLX in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.