🧠 Anthropic Leapfrogs OpenAI

And Meta Superintelligence launches its new model

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Anthropic Leapfrogs OpenAI

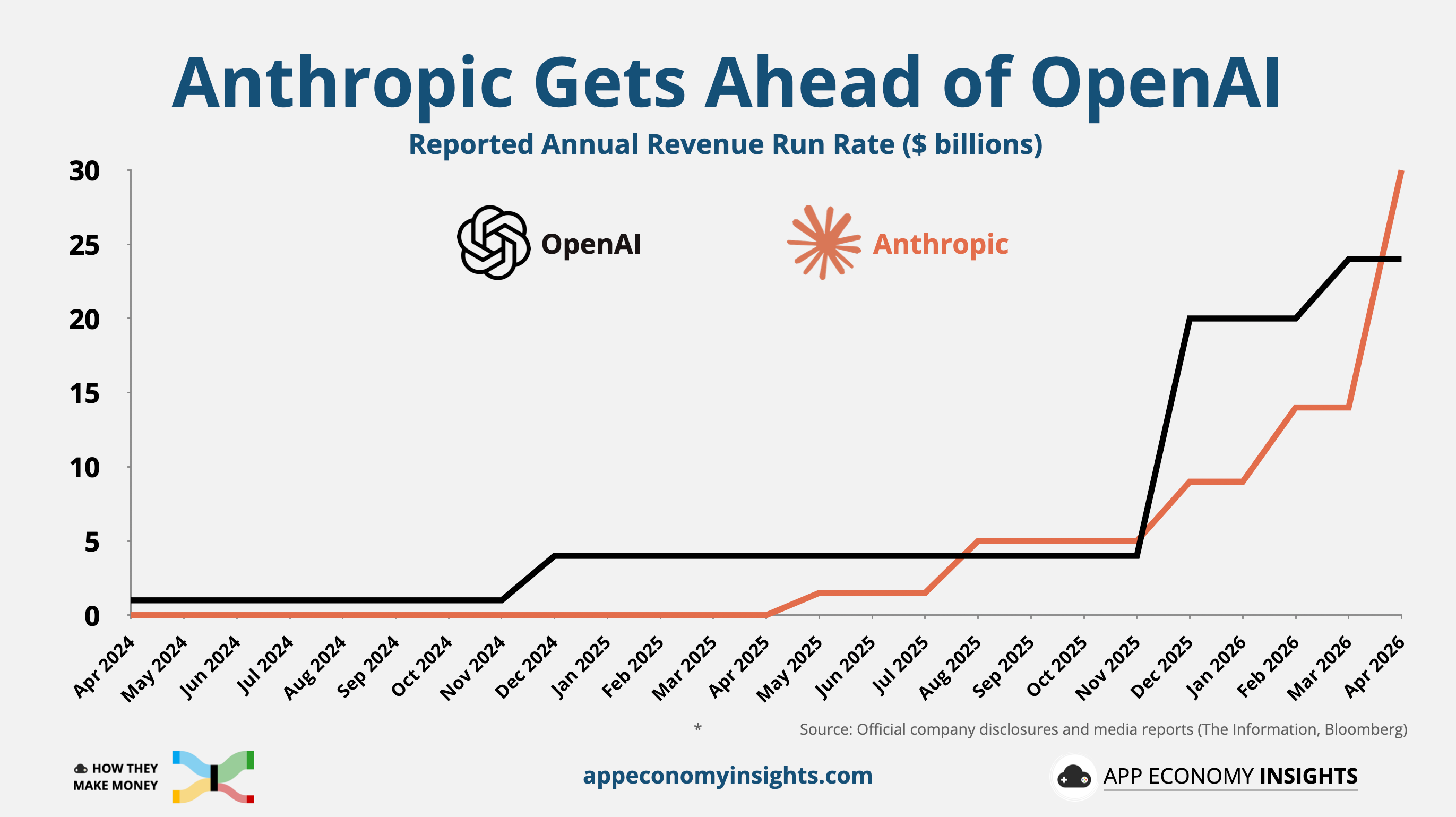

Earlier this week, the AI race leaderboard just saw a historic—and controversial—flip.

Anthropic announced its annual revenue run rate (ARR) has topped $30 billion. It was just a few days after OpenAI disclosed its ARR was roughly $24 billion. These numbers can be a bit confusing, but they are essentially the revenue from the past month multiplied by 12.

Founded by a team of former OpenAI employees, the safety-first AI lab has officially leapfrogged its competitor. While OpenAI is busy navigating C-suite volatility (more on that below), Anthropic has been catching up at breakneck speed.

Before we declare a new king of AI, we have to look at the accounting. Anthropic said the bigger number, but the two companies count their chips differently:

Anthropic’s gross method: They record the full amount a customer pays, then count the cloud provider’s cut (AWS/Azure/GCP) as an expense later.

OpenAI’s net method: They typically record only what they actually receive after Azure takes its share.

If we compared apples to apples, the gap would likely vanish. However, in the game of venture scale and market perception, Anthropic clearly has momentum in its favor.

The launch of its latest model, Mythos, doubles down on this enterprise-first strategy. The model, hilariously dubbed too powerful to be publicly released, is restricted to vetted partners at a 5x price premium ($125 per million output tokens). It’s a specialized tool for automated cybersecurity. In testing, Mythos autonomously uncovered thousands of previously unknown security flaws across every major operating system, including bugs that had survived decades of human review.

Anthropic now has over 1,000 enterprise customers spending $1M+ annually, and just secured a massive 3.5 gigawatt compute partnership with Google and Broadcom.

Today at a glance:

🏭 Intel: Team Blue Joins Musk’s Terafab

🤖 OpenAI: One Battle After Another

🥑 Meta: The Avocado Moment

🏭 Intel: Team Blue Joins Musk’s Terafab

Two weeks ago, we looked at Elon Musk’s audacious plan to solve his own chip supply constraints by building Terafab—a 100-million-square-foot vertical integration play in Austin. Our takeaway then was that while the vision was grand, the balance sheet was the ultimate bottleneck.

This week, the math changed. Intel has officially joined the Terafab joint venture.

After a high-profile handshake between Musk and Intel CEO Lip-Bu Tan at Intel’s campus last weekend, the chip giant is now a cornerstone partner alongside Tesla, SpaceX, and xAI. It’s a full-stack collaboration to restructure how silicon is built.

Why Intel? The Packaging Pivot

When we first discussed Terafab, the skepticism focused on how Musk could replicate decades of specialized foundry expertise from scratch. Intel’s entry provides two things Terafab was missing: 18A Node IP and Advanced Packaging (EMIB-T).

Intel is bringing its System Foundry approach to Austin. By integrating Intel’s packaging technology under the Terafab roof, Musk can achieve that “recursive design loop” he promised—linking logic, memory, and specialized space-hardened chips in a single, high-efficiency flow.

For Intel, this is the ultimate win for its foundry turnaround. Being the primary partner for Tesla’s Optimus and SpaceX validates Intel as the only US firm capable of leading-edge logic at this scale.

The new structure places Intel as the foundational brain, SpaceX as the bank, and Tesla/xAI as the primary customers.

Sovereignty Over Procurement

This partnership moves Terafab from a speculative moonshot to a serious sovereignty play. By anchoring the project with Intel’s 18A process, Musk is hedging against capacity constraints at TSMC and Samsung while keeping the entire supply chain within US borders.

Bottom Line: With Intel bringing its manufacturing muscle to the table, the Terafab is becoming more concrete. The question for investors shifts from “Can they build it?” to “Who owns the margins when the silicon starts rolling off the line?”

🤖 OpenAI: One Battle After Another

Between a brutal New Yorker expose and a sudden leadership vacuum, OpenAI is making moves that look more like brand defense than technological innovation.

The $100M+ Side Quest

OpenAI just acquired TBPN (Technology Business Programming Network), a niche tech talk show, for a price tag reportedly in the “low hundreds of millions.”

In context: In 2024, Spotify renewed its deal with Joe Rogan for $250 million to reach 20M+ people globally. OpenAI just spent a similar order of magnitude on a channel with roughly ~70,000 viewers per episode.

Wait, but why? According to Sam Altman, it’s a narrative play. By owning a builder-friendly media channel, OpenAI is attempting to bypass traditional journalism. They are buying a space to speak directly to the tech elite, free from the performative attacks of mainstream news.

Not so independent: The two hosts, John Coogan and Jordi Hays, will report to Chris Lehane, OpenAI’s chief political operative. They also now have an obvious financial stake in OpenAI’s success, even if the exact terms of the deal were not disclosed. OpenAI says the show will remain editorially independent. But once a media channel is owned by the company it covers, skepticism comes with the territory.

The New Yorker Reality Check

The timing of the TBPN deal follows a devastating 16,000-word New Yorker investigation this week that paints a grim picture of OpenAI’s internal culture.

Trust Gap: The report cites memos from former leaders (including Anthropic’s Dario Amodei) alleging a pattern of manipulation and deception by Sam Altman.

Safety claims vs. reality: While OpenAI publicly claims to prioritize AI safety, the report alleges that only 1%-2% of the company’s compute has gone toward safety research, often using older hardware.

Winning at all costs: Most startling, the report says OpenAI discussed a “prisoners’ dilemma” strategy that would pit world powers against one another to secure the hundreds of billions needed for its infrastructure buildout.

An Emptying C-Suite

While OpenAI is buying media companies, its executive bench is suddenly looking thinner. Several pillars of its leadership team came under pressure.

Fidji Simo (AGI Deployment Lead): Taking medical leave.

Kate Rouch (CMO): Stepping down to focus on cancer recovery.

Brad Lightcap (COO): Moved to “Special Projects” to help oversee a new private-equity joint venture.

Sarah Friar (CFO): The Information reports a growing rift with Altman over IPO timing. Friar has reportedly warned that a 2026 IPO may be too early given OpenAI’s projected cash burn, which could exceed $200 billion before the company reaches steady cash flow.

Bottom Line: When a company’s executive bench is thinning and its ethics face fresh scrutiny, optics management is starting to look as important as product development.

🥑 Meta: The Avocado Moment

After a year of playing catch-up and a series of high-profile Llama disappointments, Meta just threw its hat back in the ring. On Wednesday, the company debuted Muse Spark, the first model from Zuck’s new Meta Superintelligence Labs (MSL).

The market loved it as shares jumped 8%.

Closed For Now

For the first time, Zuck is walking away from his open source mantra.

Closed-Source Pivot: Muse Spark (internally known as Avocado) is a closed-source model. Its code and weights are staying behind Meta’s firewall. It will be available via Meta AI (both the app and the browser).

The Wang Era Begins: Muse Spark is the first major model tied to Alexandr Wang’s new superintelligence effort after Meta’s $14.3 billion Scale AI deal. Wang is a known proponent of closed models.

Monetization: Meta is inching closer to the commercial AI playbook with private API access, even if paid pricing hasn’t been announced yet. It would be a major development because virtually all of Meta’s revenue still comes from advertising.

Bloomberg reported that Muse Spark was trained using several third-party open-source models, including Alibaba’s Qwen. If accurate, that could raise fresh questions about model provenance and political optics in Washington.

How Does it Perform?

The Good: Muse Spark looks strong in science, math, health, and visual understanding. Meta says the upgraded assistant supports Instant and Thinking modes, with a more advanced Contemplating mode rolling out to boost reasoning through multiple subagents.

The Bad: It still trails frontier leaders in coding. Zuck himself has been managing expectations, calling this a “data point on our trajectory” rather than a final frontier.

Is Distribution Enough?

Meta is leaning into its greatest competitive advantage: distribution. The company is embedding Muse Spark into apps that reach 3.5 billion users. The model seems to target consumers over software engineers. Could Meta capture a meaningful share of AI queries simply by owning the apps already on everyone’s phones?

This puts OpenAI in a precarious strategic position. With Anthropic increasingly dominant in the high-margin enterprise market and Meta/Google owning the digital advertising world, OpenAI’s business looks stuck between a rock and a hard place.

Bottom Line: Meta is no longer the benevolent provider of free models. By closing the source and hiring the most expensive researchers in the world, Zuck has turned Meta into a direct commercial rival to the leading AI labs. For now, the market is valuing Meta primarily on its existing advertising business. That may be proven wrong if the company can start driving meaningful revenue from its proprietary models.

That's it for today.

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own AAPL, GOOG, META, NVDA, and TSLA in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.