📈 Broadcom: $100B AI Target

CrowdStrike shows cybersecurity demand accelerating

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights

In case you missed it:

Altman vs. Amodei

The AI race is heating up in unexpected ways.

This week, tensions spilled into the open between OpenAI and Anthropic. According to a report by The Information, a leaked internal memo from Anthropic CEO Dario Amodei accused OpenAI of “mendacious” messaging in its dispute with the Pentagon, even taking a swipe at Sam Altman’s ties to the Trump administration.

Speaking at the Morgan Stanley TMT conference on Wednesday, NVIDIA CEO Jensen Huang confirmed that OpenAI is preparing to go public later this year (stay tuned for our visuals!). Huang noted that this looming IPO is why NVIDIA finalized a $30 billion investment now, rather than a previously rumored $100 billion deal.

The AI boom is forcing companies to rethink everything, from geopolitics to infrastructure spending. Two earnings reports this week offered a glimpse into how the AI economy is taking shape.

Today at a glance:

📈 Broadcom: $100 Billion AI Target

🦅 CrowdStrike: AI Fears Reality Check

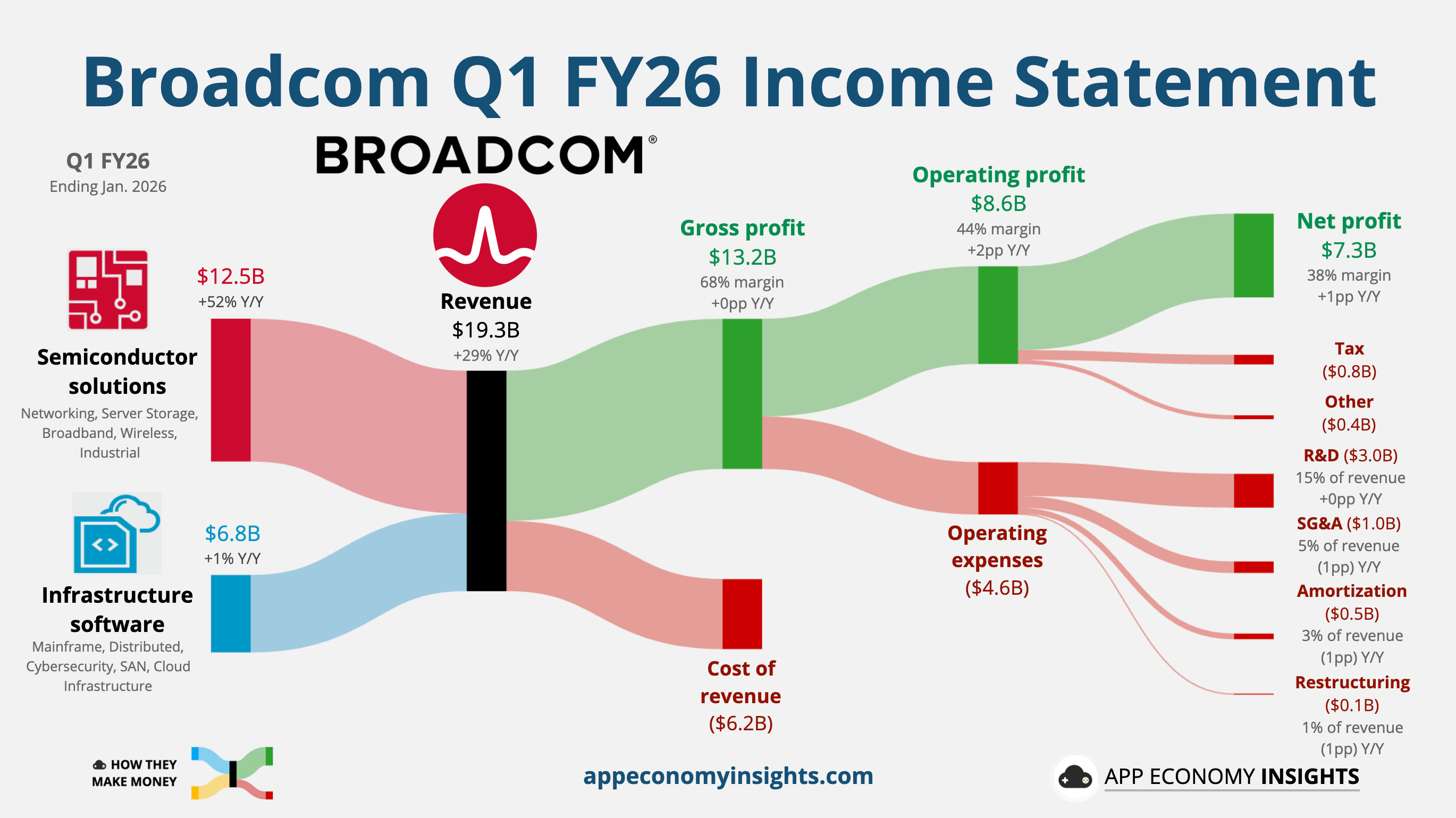

1. 📈 Broadcom: $100 Billion AI Target

Broadcom released its Q1 FY26 (January quarter) with a massive top-and-bottom-line beat and one of the most aggressive outlooks in the semiconductor space. Q1 revenue rose 29% Y/Y to $19.3 billion ($0.2 billion beat), and non-GAAP EPS reached $2.05 ($0.03 beat).

The AI growth engine is accelerating faster than anticipated.

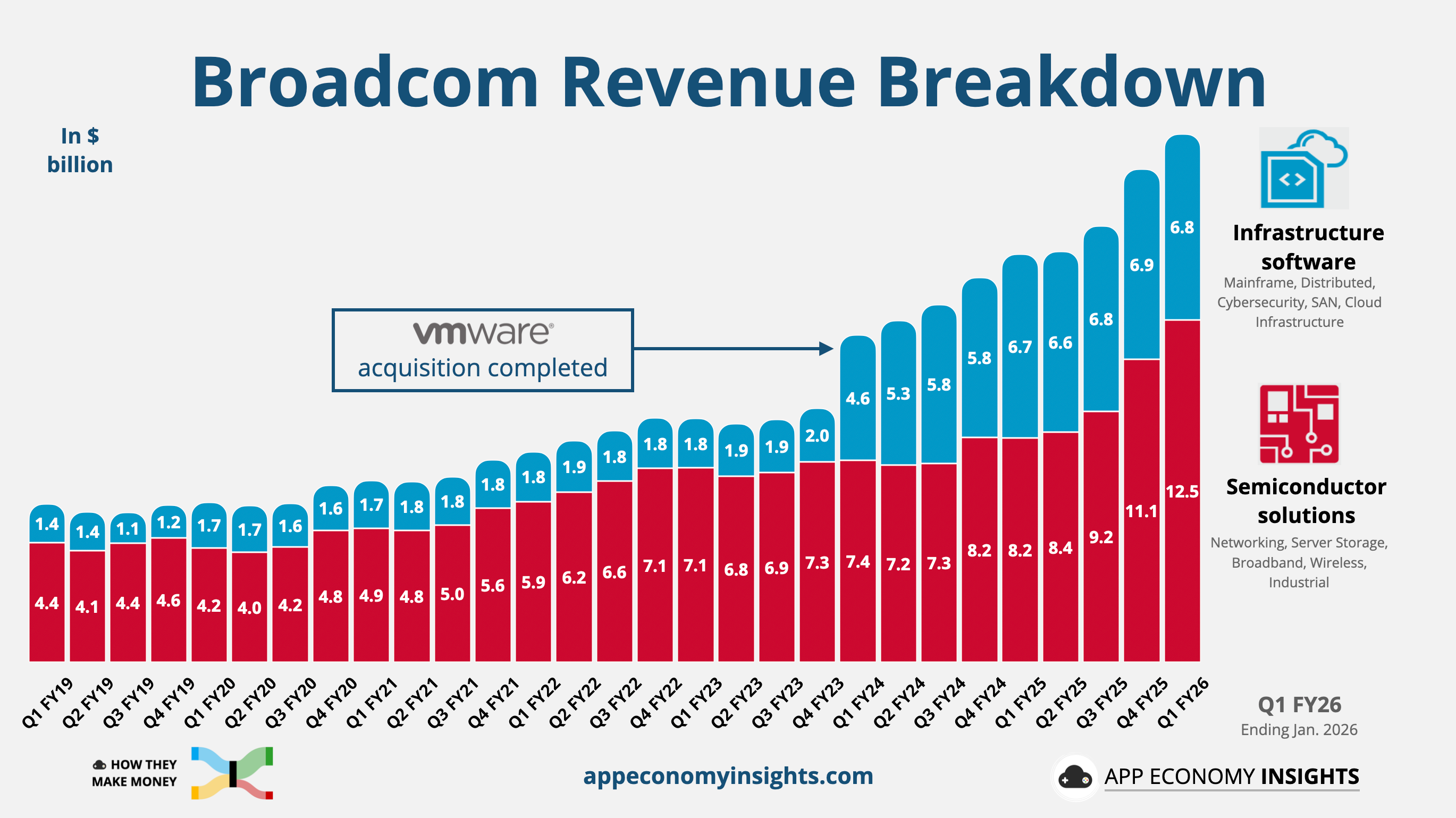

The Semiconductor solutions segment rose 52% Y/Y to $12.5 billion. Within that segment, AI revenue more than doubled (+106% Y/Y) to $8.4 billion

The Infrastructure software segment, housing VMware, contributed $6.8 billion (up 1% Y/Y).

CEO Hock Tan dropped a bombshell during the earnings call to dispel any fears of an AI slowdown. Broadcom expects its AI chip sales to top a staggering $100 billion in 2027. Tan assured analysts that the company already has the “line of sight” and the secured supply chain to hit this milestone.

If achieved, that would cement Broadcom as the premier alternative to NVIDIA for custom AI accelerators and networking chips.

Custom Silicon Gold Rush

Much of the momentum is coming from hyperscalers designing custom AI accelerators rather than relying solely on GPUs. Broadcom builds these chips—often called XPUs—for some of the largest AI companies in the world.

Management confirmed the company now has six major AI customers, with OpenAI recently joining the roster.

Together, they represent ~10 gigawatts of AI compute demand for 2027.

OpenAI alone is expected to deploy over 1 gigawatt of capacity by then.

Much of this demand is tied to inference workloads, as AI labs move from training models to deploying them into real-world products.

Networking Becomes the Bottleneck

Large AI clusters require enormous bandwidth to connect thousands of accelerators operating simultaneously. Broadcom is benefiting from that constraint.

The company is seeing strong demand for its 100-terabit networking switches, which are becoming essential components of modern AI systems.

Management expects AI networking to account for roughly 33% to 40% of total AI revenue over time.

Guidance

For Q2 FY26, Broadcom expects revenue of roughly $22 billion, far above the $20.5 billion consensus, with adjusted EBITDA margins holding steady near 68%. AI semiconductor revenue alone is projected to reach $10.7 billion next quarter (up 27% sequentially), highlighting the rapid ramp in hyperscaler AI deployments.

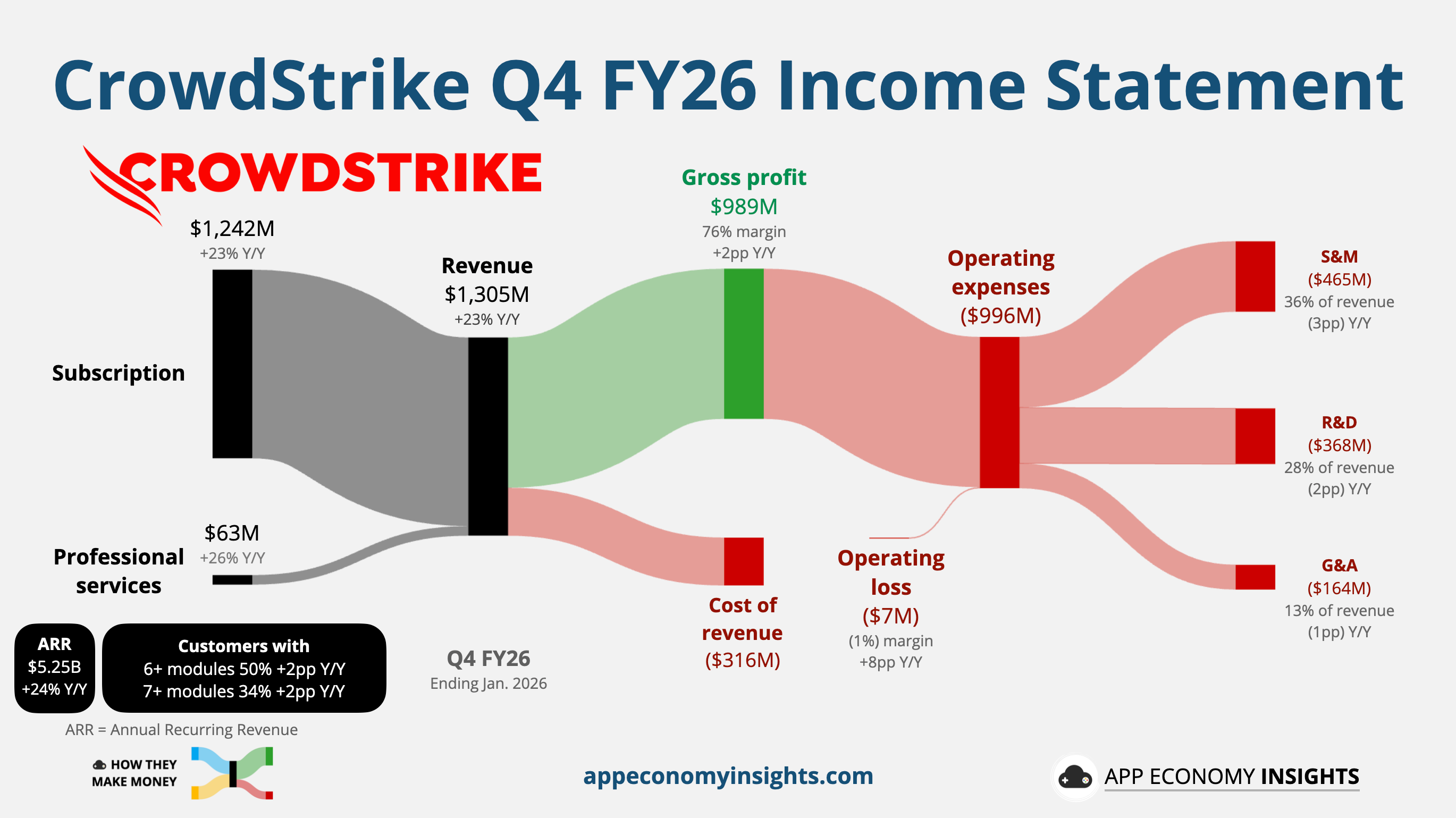

2. 🦅 CrowdStrike: AI Fears Reality Check

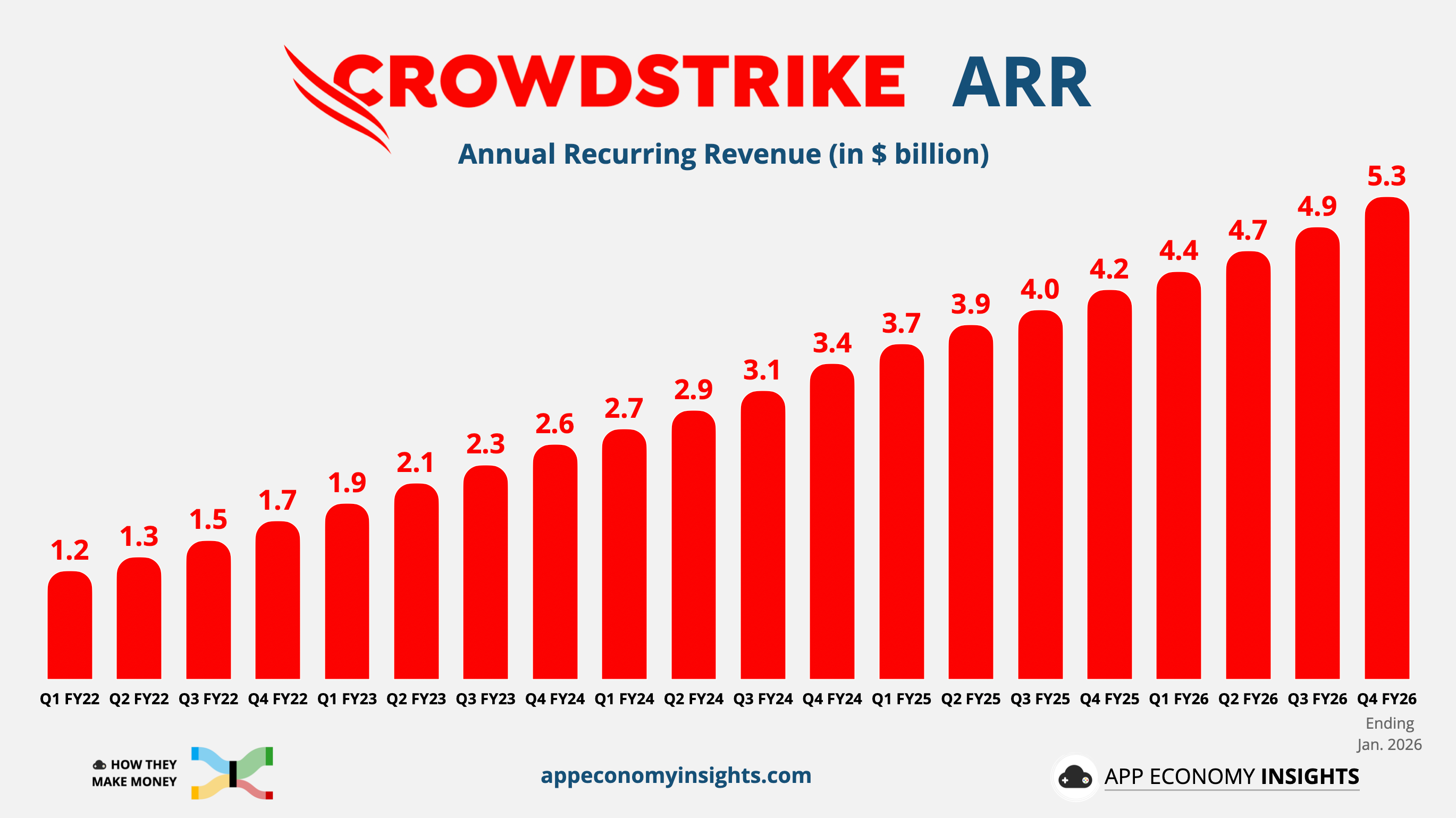

During its 2023 Fal.Con Investor Briefing, CrowdStrike set an ambitious target of $10 billion in Annual Recurring Revenue (ARR) within 5 to 7 years.

The company just crossed the halfway mark, surpassing $5 billion in ARR. That’s despite a massive IT outage in July 2024 that caused widespread disruption.

The milestone arrives at an interesting moment. Cybersecurity stocks have recently sold off on fears that advanced AI tools could disrupt traditional software models. CrowdStrike’s latest results suggest the opposite. AI may be expanding the threat surface faster than defenses can keep up.

Revenue in Q4 FY26 (January quarter) grew 23% Y/Y to $1.31 billion ($10 million beat), and non-GAAP EPS landed at $1.12 (a $0.02 beat).

Free cash flow surged 57% Y/Y to a record $376 million, representing a 29% margin. However, the figure is partially boosted by stock-based compensation (SBC).

CrowdStrike is nearly turning a GAAP operating profit, a milestone that remains elusive for many software companies that rely heavily on SBC. For CrowdStrike, SBC was 23% of revenue in FY26. That’s a very high level and hasn’t shown signs of going down over time.

The headline metrics confirm the post-outage recovery is fully complete and the company is back in growth mode.

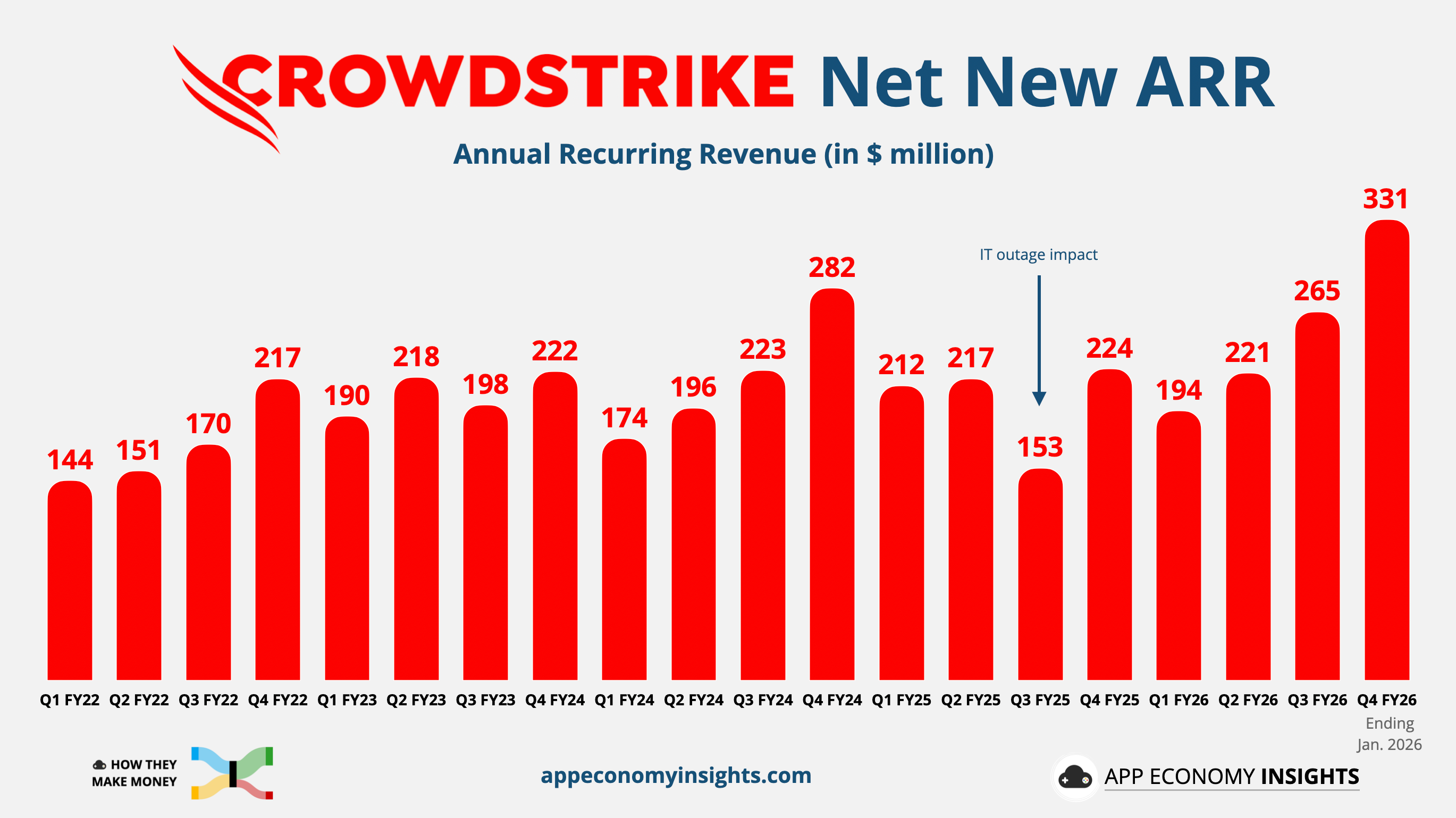

Ending ARR rose 24% Y/Y to $5.25 billion, accelerating from 23% Y/Y in Q3.

Net New ARR is a critical metric for business momentum. Q4 FY26 net new ARR hit $331 million, a massive 47% Y/Y rebound. Q4 is typically the strongest quarter seasonally. Compared to Q4 FY24 (pre-outage), net new ARR was up 17%.

The broader cybersecurity sector has been under severe pressure lately, driven by investor anxiety that advanced AI tools (like Anthropic’s new code-scanning features) will disrupt traditional software models. CEO George Kurtz aggressively pushed back against this narrative, stating that the AI revolution is weaponizing adversaries and creating a massive growth opportunity for CrowdStrike.

Instead of replacing cybersecurity software, AI is expanding the attack surface. CrowdStrike is responding by building tools designed specifically to secure the AI stack.

The company’s platform strategy is central to that response.

Flex Engine and Consolidation

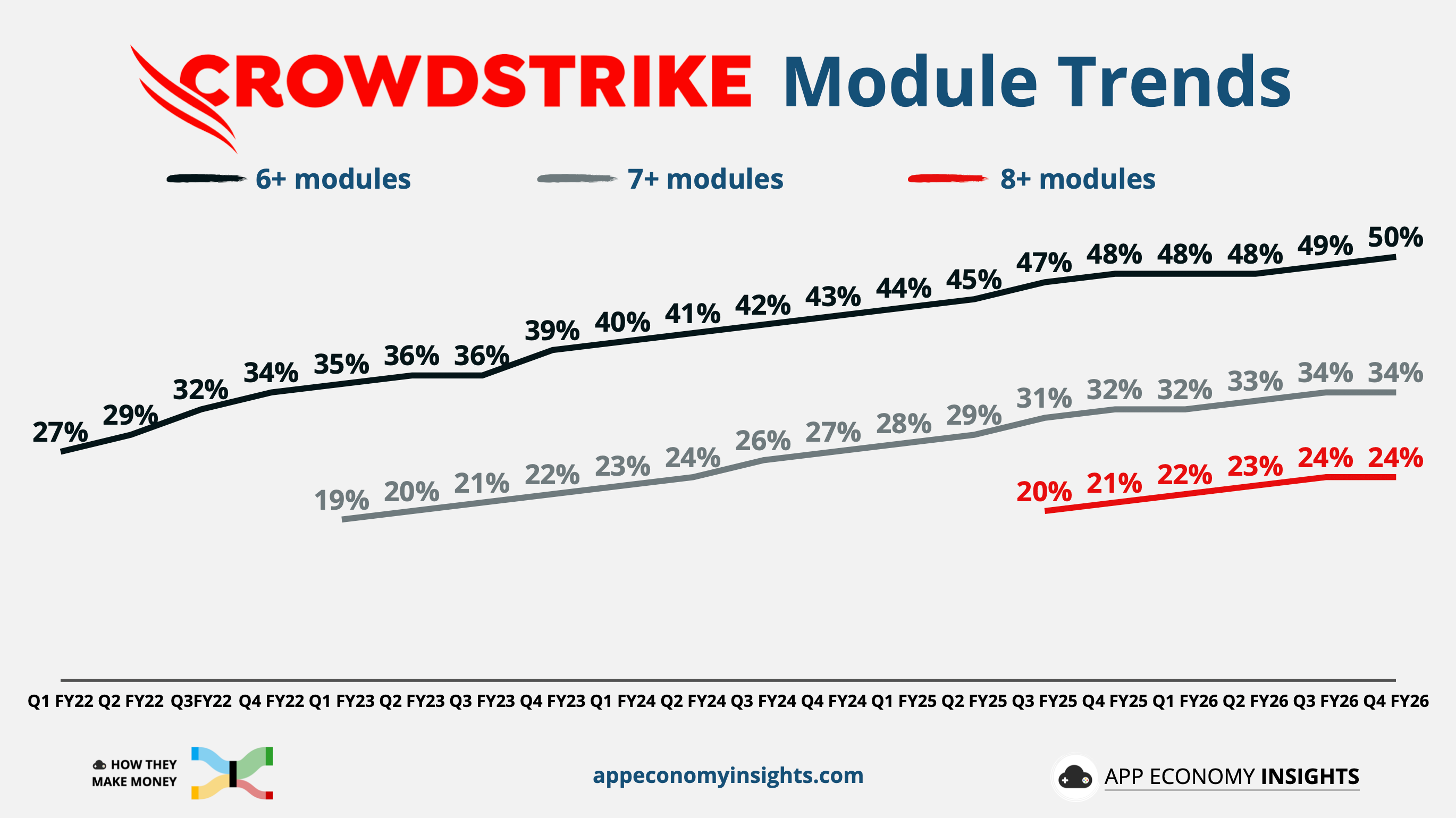

The Falcon Flex licensing model remains a powerful growth engine. Customers commit to a security budget upfront and allocate it over time across Falcon modules. CrowdStrike now counts over 1,600 Flex customers, each with an average ARR above $1 million. The model reduces purchasing friction and encourages platform consolidation:

50% of customers use six or more modules

24% use eight or more

380 Flex customers expanded commitments this quarter, lifting ARR by an average of 26%.

Securing the AI Stack

To address these new AI attack surfaces, CrowdStrike is rapidly expanding its platform footprint.

Next-Gen SIEM: The module grew by more than 75% Y/Y, reaching over $585 million in ending ARR, proving it is successfully disrupting legacy incumbents.

M&A Expansion: The company recently acquired SGNL to secure AI identities and Seraphic to protect the enterprise browser, viewing the browser as the primary gateway for AI applications.

AI-DR: The newly launched AI Detection and Response offering is seeing explosive demand, growing over 5x quarter-over-quarter as enterprises seek visibility into how employees use AI tools.

Guidance

For FY27, management expects revenue to grow 23% Y/Y to $5.9 billion, slightly ahead of consensus and implying no slowdown. Free cash flow margins are expected to exceed 30%, but investors will be watching whether stock-based compensation finally begins to normalize.

That’s it for today!

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own AVGO and CRWD in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.