🤖 NVIDIA's Tokenomics

Jensen Huang explains why he see an inflection point

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights

In case you missed it:

The Token Economy

Headlines are fixated on AI bubble skepticism, while NVIDIA’s numbers tell a story of a new world being built.

CEO Jensen Huang believes we officially moved past the era of experimental training and entered the era of the agentic inflection:

“In this new world of AI, compute equals revenues. Without compute, there’s no way to generate tokens. Without tokens, there’s no way to grow revenues. [...] I am certain at this point that we’ve reached the inflection point.”

Huang is framing NVIDIA’s chips not as a capital expense, but as the direct raw material (tokens) required for customers to make money.

The latest quarter highlights three structural pillars:

Tokenomics over CapEx: Compute is becoming a raw material. Because every AI-generated token (a word, a pixel, a line of code) has an immediate market price, higher performance-per-watt translates directly into higher net margins per token.

Systems over Silicon: The bear case argues that specialized custom chips would steal the inference market. NVIDIA’s response is a shift from selling individual chips to delivering entire AI Factories. By controlling the networking fabric and the software stack, NVIDIA is ensuring that the cost-per-token remains lower on its platform.

Multi-Generational Overlap: For the first time, NVIDIA is ramping two flagship architectures—Blackwell and Rubin—simultaneously. With Rubin samples already shipping to customers this week, the roadmap is designed to capture the bulk of the estimated $4 trillion in infrastructure build-out coming this decade.

Let’s break down the quarter.

Today at a glance:

NVIDIA’s Q4 FY26.

Business highlights.

Key quotes from the call.

What to watch moving forward.

1. NVIDIA Q4 FY26

NVIDIA’s fiscal year ends in January, so they just reported Q4 FY26.

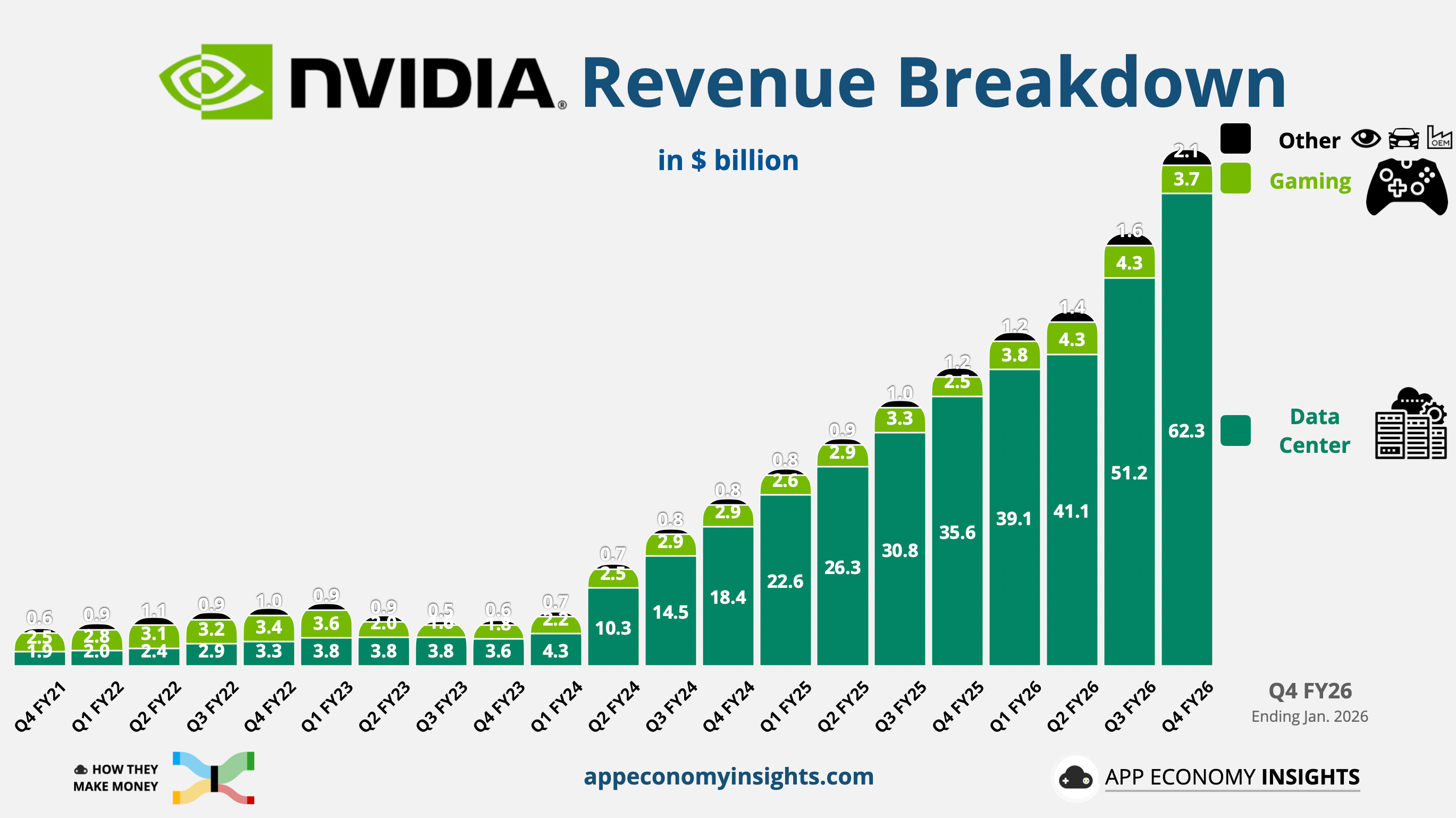

Data Center revenue remains off the charts, as illustrated below.

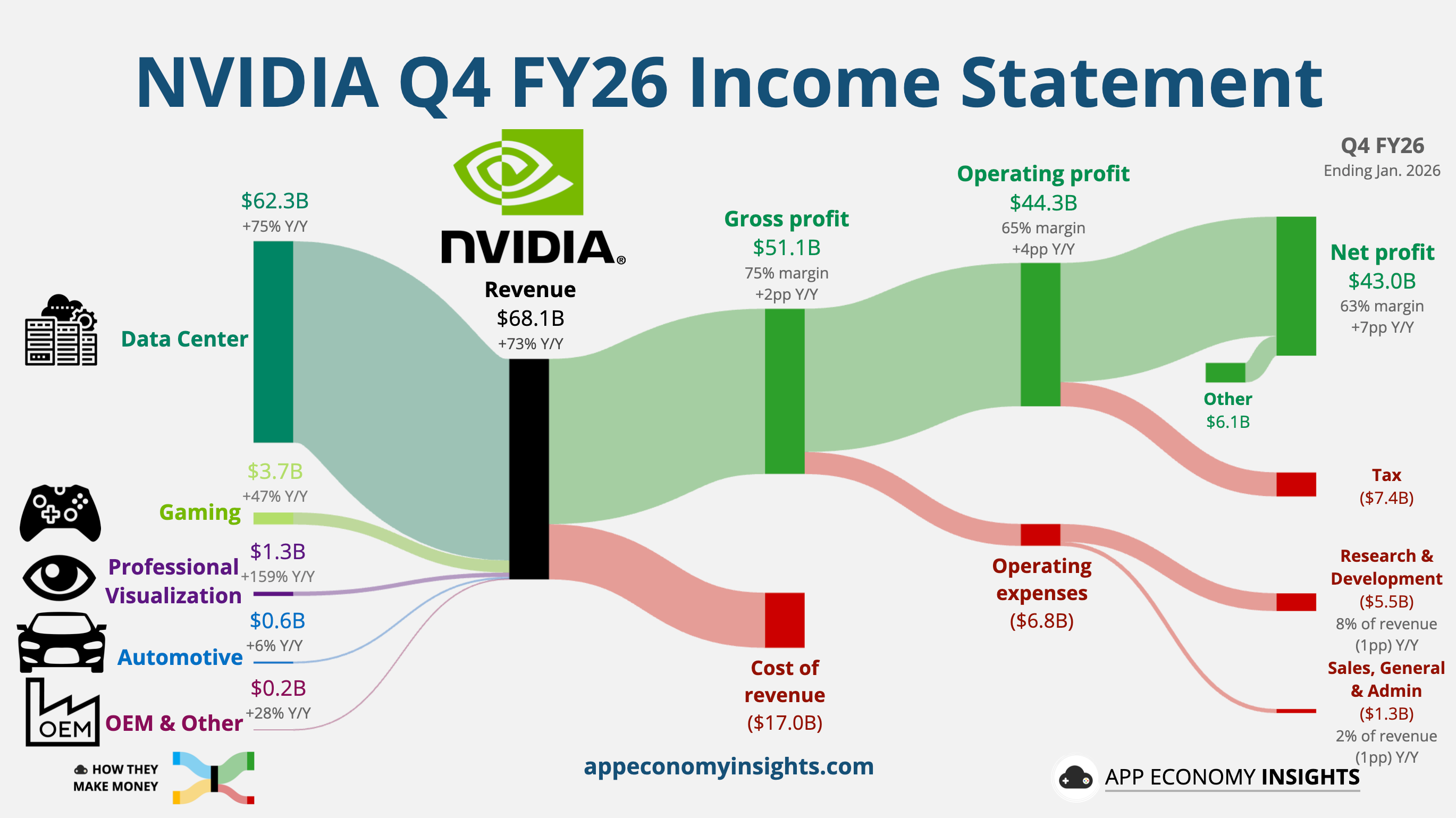

Income statement:

Revenue jumped +20% Q/Q and 73% Y/Y to $68.1 billion ($1.9 billion beat).

⚙️ Data Center +22% Q/Q and +75% Y/Y to $62.3 billion.

🎮 Gaming -13% Q/Q and +47% Y/Y to $3.7 billion.

👁️ Professional Viz +75% Q/Q and +159% Y/Y to $1.3 billion.

🚘 Automotive +2% Q/Q and +6% Y/Y to $0.6 billion.

🏭 OEM & Other -7% Q/Q and +28% Y/Y to $0.2 billion.

Gross margin was 75% (+2pp Y/Y).

Operating margin was 65% (+4pp Y/Y).

Non-GAAP operating margin was 68% (+1pp Y/Y).

Non-GAAP EPS $1.62 ($0.08 beat).

Cash flow:

Operating cash flow +118% Y/Y to $36.2 billion.

Free cash flow +58% Y/Y to $34.9 billion.

Balance sheet:

Cash and cash equivalents: $62.6 billion.

Debt: $8.5 billion.

Q1 FY27 Guidance:

Revenue +15% Q/Q and +77% Y/Y to $78.0 billion ($6.0 billion beat).

Gross margin 75% (flat Q/Q).

So, what to make of all this?

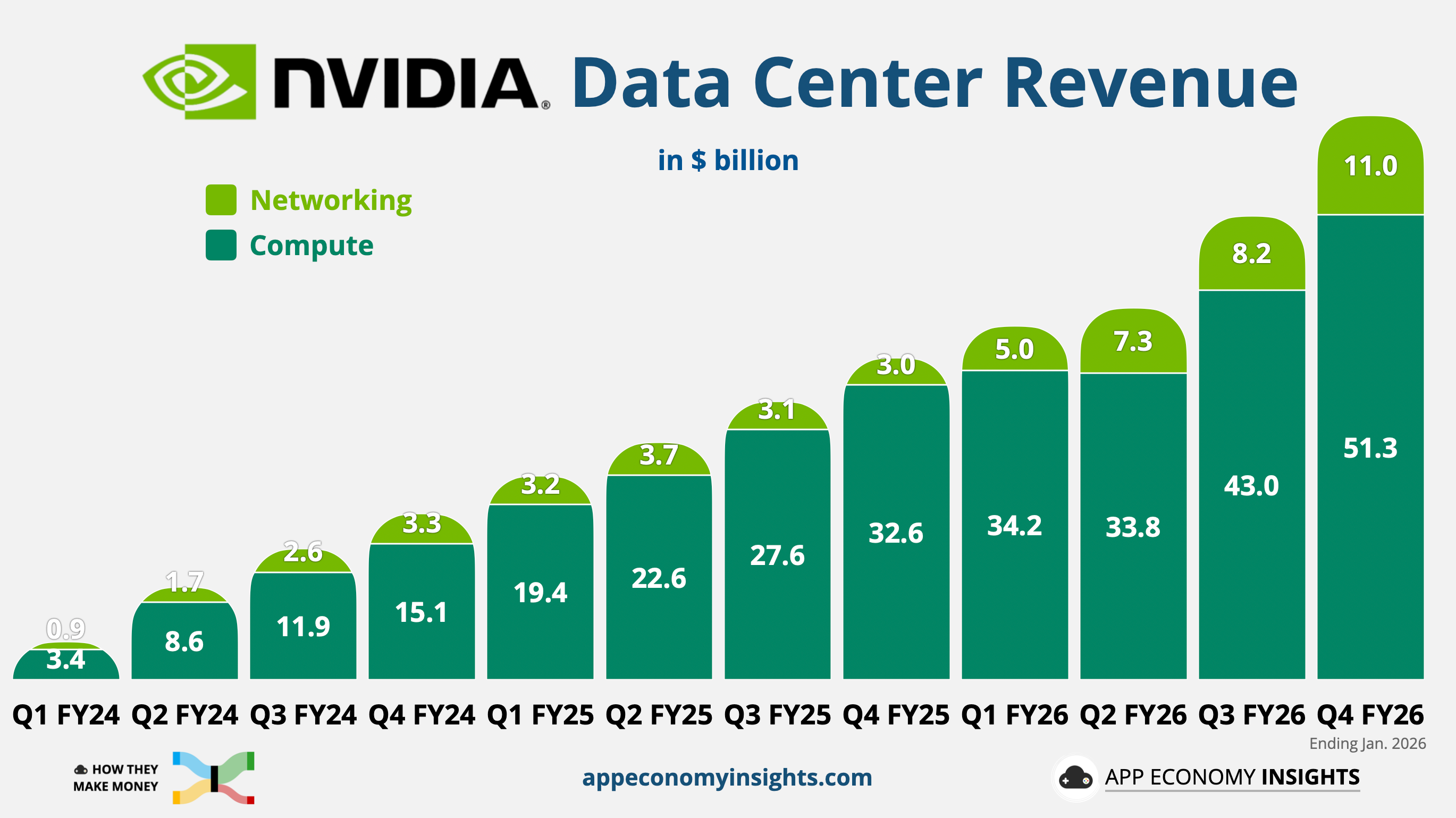

⚙️ Data Center is now 91% of the business: We are witnessing a fundamental shift from AI being a research project to a profit center.

⚡ King of inference: While bears argue that specialized chips (ASICs) might take share as the market moves from training to inference. The Grace Blackwell servers are proving to be the most efficient infrastructure for running live AI tools.

🔌 Networking as a moat: Networking revenue hit $11 billion. This is the glue that prevents customers from easily switching to rival chips. As clusters grow to millions of GPUs, the complexity of the networking fabric becomes a structural barrier to entry for competitors.

🎮 Gaming faces a supply squeeze: Revenue fell 13% Q/Q to $3.7 billion. While some of this is seasonal, the bigger story is the global shortage of memory chips. NVIDIA is currently prioritizing its high-margin Data Center business for these scarce components, leaving the Gaming division supply-gated for the foreseeable future.

👁️ Professional Visualization was the surprise star: It was the fastest-growing segment this quarter, jumping 75% Q/Q to $1.3 billion. This was driven by a massive enterprise refresh cycle as companies upgrade to Blackwell-based workstations to run AI agents and industrial digital twins locally rather than in the cloud.

📈 Margins are the ultimate lie detector: Despite the complexity of ramping liquid-cooled Blackwell racks and the surging cost of memory chips, gross margin improved to 75.2%. If demand were softening or competition were biting, this would be the first place we would see scuff marks. The warning of a "very tight" supply for the next few quarters could shake things up.

🔮 The $78 billion outlook: Q1 FY27 guidance was a massive $6 billion beat over analyst estimates. But the market’s tepid reaction proves that NVIDIA is now held to a very high standard. Some bulls were whispering for $80 billion, and any hint of a supply ceiling (like the memory crunch) is enough to make investors pause.

Big picture: NVIDIA’s engine is now powered by the Blackwell Ultra refresh, the explosive networking growth, and the agentic transition. With $95 billion in supply-related commitments on the books, NVIDIA is already manufacturing the next two years of the AI cycle.

2. Business highlights

🔄 Circular Economy Critique

The market is increasingly focused on the cozy relationship between NVIDIA and its largest customers. With nearly $97 billion in annual free cash flow, NVIDIA is becoming the venture capitalist of the AI age.

By participating in OpenAI’s latest $30 billion round and deepening ties with Anthropic and CoreWeave, NVIDIA ensures that the most advanced AI models remain optimized for CUDA. Critics argue that NVIDIA is funding its own customers.

Jensen Huang defended this by highlighting the diversity of the customer base. Hyperscalers now account for only 50% of revenue, and growth is shifting toward sovereign AI and enterprise ISVs. The circular risk is diluted as the ecosystem broadens.

He also doubled down on the idea that customers must keep spending to grow. It captures the tension of this moment. NVIDIA sees a new industrial revolution, while some on Wall Street see a CapEx binge.

↗️ AMD’s New Shareholders

A more immediate threat emerged recently, as some of NVIDIA’s largest customers became shareholders in a competitor.

Meta just announced a multi-generation agreement worth more than $100 billion to deploy up to 6 gigawatts (GW) of AMD compute capacity. To secure this capacity, AMD issued Meta performance-based warrants for up to 160 million shares—roughly a 10% equity stake in AMD.

It is a carbon copy of the OpenAI-AMD pact signed in late 2025, which also included a 6 GW commitment and a 10% equity incentive.

By aligning their financial interests with AMD, two of NVIDIA’s most important allies are now directly incentivized to see AMD’s MI450 architecture succeed. For every gigawatt they deploy, they not only solve their supply chain bottleneck, but they also potentially unlock billions in capital appreciation from their AMD holdings. They are ecosystem partners with a vested interest in a multi-polar GPU market.

🇨🇳 China/Trump Wildcard

The market is valuing NVIDIA as if China is permanently zero. That embeds an option into the stock.

The Trump administration’s decision to allow small-scale H200 shipments comes with a US inspection requirement and a 25% tariff. This effectively makes NVIDIA chips the most expensive way to build AI in China.

CFO Colette Kress was clear that they are guiding for $0 revenue from China Data Center compute. This conservative guidance means any surprise approval or easing of these inspections represents an upside. NVIDIA is currently winning without China.

3. Key quotes from the earnings call

Check out the earnings call transcript on Fiscal.ai here.

CEO Jensen Huang:

On the agentic shift:

“The wave that we’re seeing now is the agentic AI inflection [...] and it literally happened in the last couple of two, three months. [...] The agents are super smart, they’re solving real problems. Coding is obviously supported by agentic systems now.”

The latest catalyst is the shift from chatbots to autonomous agents that “run for minutes to hours” and consume massive amounts of compute.

On the “Dielet Tax” and architectural integrity:

“Every time you cross a dielet, you have to cross an interface. Every time you cross an interface, you add latency, you add power unnecessarily. [...] The dielet tax shows up in the architecture effectiveness of the competitors.”

Jensen is defending NVIDIA’s monolithic design (single piece) as a physical advantage in power efficiency that competitors using multi-chiplet designs can’t easily match. His bet is that architectural purity beats modular flexibility at hyperscale.

4. What to watch moving forward

NVDA has been mostly flat in the past 6 months, a period of consolidation. The latest 13F filings for Q4 2025 showed that some funds were still buying, such as Altimeter and Atreides. The stock remains one of the most widely held names, although many funds are still underexposed relative to its nearly 8% weight in the S&P 500.

At ~27x forward earnings, NVIDIA trades mostly in line with the rest of Big Tech. But with EPS surging 67% Y/Y, you could certainly argue it looks cheap. NVIDIA’s growth is supply-constrained. That means quarter-to-quarter noise matters less than understanding how long this cycle can run and what the business looks like when demand normalizes.

If you’re a regular reader, you already know the stakes:

Inference momentum: Will NVIDIA’s full-stack strategy (Networking + Vera CPUs) protect its 75% margins against the rising tide of custom hyperscaler chips?

Memory bottleneck: Watch for any signs that the memory supply chain is loosening. With Micron exiting the consumer chip business and Steam running out of handhelds, NVIDIA’s Gaming rebound depends entirely on the availability of RAM.

Rubin cadence: Jensen confirmed Rubin is already in production. Any delay in the Blackwell-to-Rubin transition could create a demand air pocket that the market isn’t prepared for.

China visibility: NVIDIA is maintaining a zero-China baseline. Any revenue recognized through the new inspection-based licenses would be a pure upside surprise to the current stock price.

Power-to-token ratio: As data centers hit the 1-Gigawatt ceiling, performance-per-watt is the new ROI. NVIDIA’s lead depends on being the most energy-efficient AI factory on the planet.

In a token economy, efficiency is profit.

That’s the battlefield NVIDIA intends to dominate.

That’s it for today!

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own AAPL, AMD, AMZN, GOOG, META, and NVDA in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.

This is exactly what we were watching. A perfect print across the board and the market sold it anyway. I dug into why the tape reacted the way it did in our latest piece if you want to compare notes. https://fulcruminsights.substack.com/p/nvda-a-perfect-print-a-perplexing