👔 Is Workday Cooked?

WDAY MELI AXON AS HPQ DPZ TEM DOCN HIMS AMC

Welcome to the Premium edition of How They Make Money.

Over 290,000 subscribers turn to us for business and investment insights.

In case you missed it:

🗓️ A flood of earnings is rolling in this week

We’re tracking the early standouts today.

Coming up later this week: NVIDIA, Salesforce, Snowflake, and more.

Anthropic’s announcement of Claude Code Security on Friday has triggered a sell-off in the last few software stocks that had been holding up. The tool scans codebases and patches vulnerabilities like a human researcher. It wiped billions in value off security leaders like CrowdStrike and Okta. It’s the latest reminder that if you are a software stock in 2026, you are only one Anthropic blog post away from calamity.

While Anthropic is busy terrifying SaaS investors, the company itself relies on Workday to manage its own global operations. It might surprise you since Klarna famously ditched the software in 2024 to build its own alternative internally. It seems even the creators of the world’s most advanced agents still need a reliable place to file their expenses and manage their headcount.

It’s the delicious irony of this moment. The largest AI disruptors are still writing checks to the incumbents for their HR and finance stacks. The AI revolution is still being run on the very software it’s supposed to be replacing. But it probably won’t change the bear case, which ignores the numbers today and focuses on the disruption tomorrow.

Today at a glance:

👔 Workday: Funding the AI Pivot

🤝 MercadoLibre: Playing the Long Game

⚡️ Axon: Surprise 2028 Target

⛷️ Amer Sports: Salomon Expansion

🖨️ HP: PC Strength Overshadowed

🍕 Domino’s: Taking a Bigger Slice

🧬 Tempus AI: Scaling Data Advantage

🌊 DigitalOcean: Rule of 50 by 2027

💊 Hims & Hers: Legal Headwinds

🍿 AMC: Attendance Drops

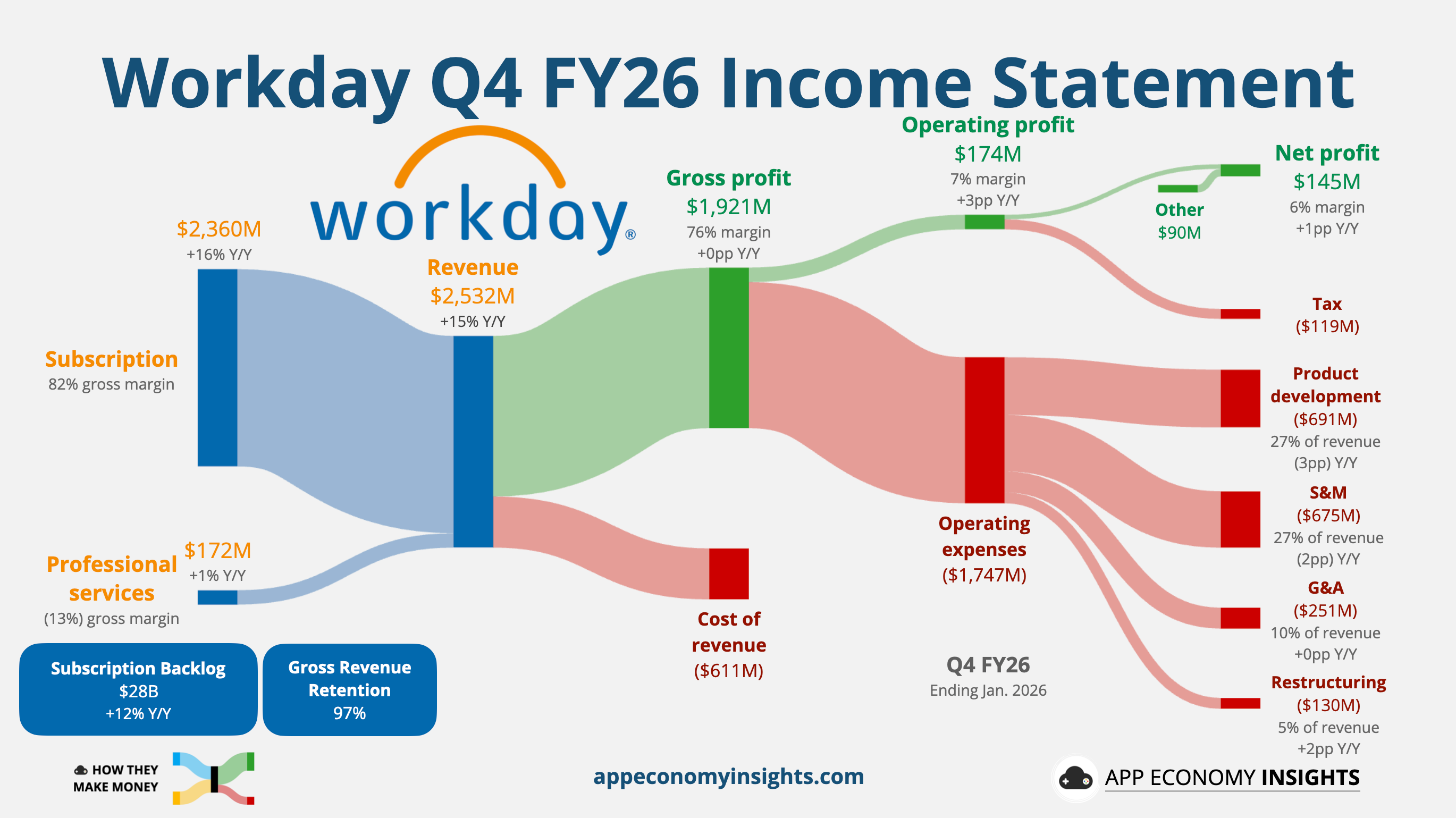

1. 👔 Workday: Funding the AI Pivot

Workday wrapped up FY26 (ending in January) with a fourth-quarter beat. But a soft outlook and a sudden CEO transition sent shares tumbling roughly 8% in after-hours trading. Q4 revenue rose 15% Y/Y to $2.53 billion ($10 million beat), and non-GAAP EPS reached $2.47 ($0.15 beat). Subscription revenue was the main driver, rising 16% Y/Y to $2.36 billion.

WDAY was already in a tough spot, with shares trading nearly 60% off their peak. The market reacted poorly to the company’s fiscal 2027 guidance. Workday expects full-year subscription revenue growth to slow to 12% to 13% ($9.925 billion to $9.950 billion), missing the $10 billion consensus estimate. This outlook matched the growth in subscription revenue backlog, up 12% Y/Y to $28.1 billion.

Adjusted operating margins are also forecasted to dip to 30% in FY27 (down from 30.6% in Q4 FY26) as the company prioritizes AI investments over near-term margin expansion. Management also noted that large enterprise deals in the federal and healthcare sectors are taking longer to close.

Workday is spending heavily to buy its way into immediate AI capabilities. In quick succession, they integrated Sana (conversational AI and enterprise connectivity) and acquired Pipedream (a startup with tools to connect AI agents to external services), following the recent close of Paradox (an AI recruiting platform).

The ROI on this approach is starting to show. In Q4 alone, Workday generated over $100 million in new Annual Contract Value (ACV) strictly from emerging AI products (over 100% Y/Y growth). Overall Annual Recurring Revenue (ARR) from these AI solutions has now crossed $400 million. Internally, the company has completely overhauled its engineering infrastructure. Over 75% of Workday's software engineers now use AI coding assistants, resulting in more than 50% of newly committed code being AI-generated and boosting overall engineering output by 22%.

The quarter featured a major leadership change. Carl Eschenbach stepped down earlier this month, bringing co-founder Aneel Bhusri back to the CEO role. Bhusri used the earnings call to push Workday’s Chapter Four strategy, focusing heavily on integrating agentic AI directly into HR and finance workflows. To monetize this shift, the company is transitioning to a consumption-based Flex Credits pricing model for its AI offerings.

These clear AI tailwinds are not doing much for the stock. For now, the market is keeping WDAY in the penalty box and isn’t giving the new management team the benefit of the doubt. The company is trading at a forward EBITDA multiple below 10x.