🏔️ The $111B Hollywood Gamble

Netflix takes the cash as the Ellisons go all-in for Warner

Welcome to the Premium edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

If you are experiencing a severe case of déjà vu, don’t worry.

Just a few weeks ago, we were breaking down the seismic $83 billion deal that was supposed to turn Netflix into the ultimate entertainment conglomerate. We analyzed the spin-offs, incoming regulatory steps, and the future of Warner Bros. without the cable anchor. It felt like a done deal.

As of today, that deal is officially dead.

In a move straight out of a prestige HBO drama, Paramount Skydance hiked its bid to $31 per share in cash to swallow the entire company, including its linear channels and massive debt.

On the same day, Netflix co-CEOs Ted Sarandos and Greg Peters officially walked away, refusing to engage in a bidding war.

It’s a total reversal for the industry.

Netflix wanted to cherry-pick the IP and leave the legacy TV business behind.

Paramount is doubling down on the old-school studio model, embracing the linear bundle, and promising a theatrical-first future.

Today, we’re unpacking the new $111 billion acquisition. We’ll look at the massive debt pile, the $7 billion regulatory insurance policy, and why this shotgun wedding has California’s Attorney General reaching for his briefcase.

Let’s unpack the deal, the drama, and the data.

Today at a glance:

Why Netflix Walked

What Para+Warner Looks Like

Eye-popping Leverage

Regulatory Gauntlet

Winners & Losers (updated)

1. Why Netflix Walked

Netflix officially pulled the plug right after WBD’s board declared Paramount’s $111 billion bid a “superior proposal” on February 26. The company ultimately chose its balance sheet over a bidding war.

In a joint statement, Sarandos and Peters candidly explained:

“We’ve always been disciplined, and at the price required to match Paramount Skydance’s latest offer, the deal is no longer financially attractive. This was always a ‘nice to have’ at the right price, not a ‘must have’ at any price.”

The gap between the two offers was not only about value, but also about the nature of the deal. Netflix was only interested in the clean assets (Studios and HBO Max), requiring a complex spin-off of the declining linear networks into Discovery Global.

David Ellison, backed by his billionaire father Larry, made it easy for WBD’s board. They took everything. For WBD management, a clean cash exit at $31/share was simply too good to pass up compared to the messy, tax-intensive spin-off Netflix required.

Netflix investors cheered the move. The stock jumped 14% immediately after the announcement. By walking away, Netflix avoids the winner’s curse of overpaying for no-growth assets.

While Paramount inherits a mountain of debt, Netflix walks away with its balance sheet intact and a $2.8 billion cash consolation prize. This break-up fee was immediately paid by Paramount to Netflix to clear the board.

2. What Para+Warner Looks Like

What happens when two debt-heavy media companies facing structural decline merge? Let’s take an educated guess.

Paramount is buying the entire house, creating a media colossus that looks more like a 20th-century conglomerate than a 21st-century tech platform.

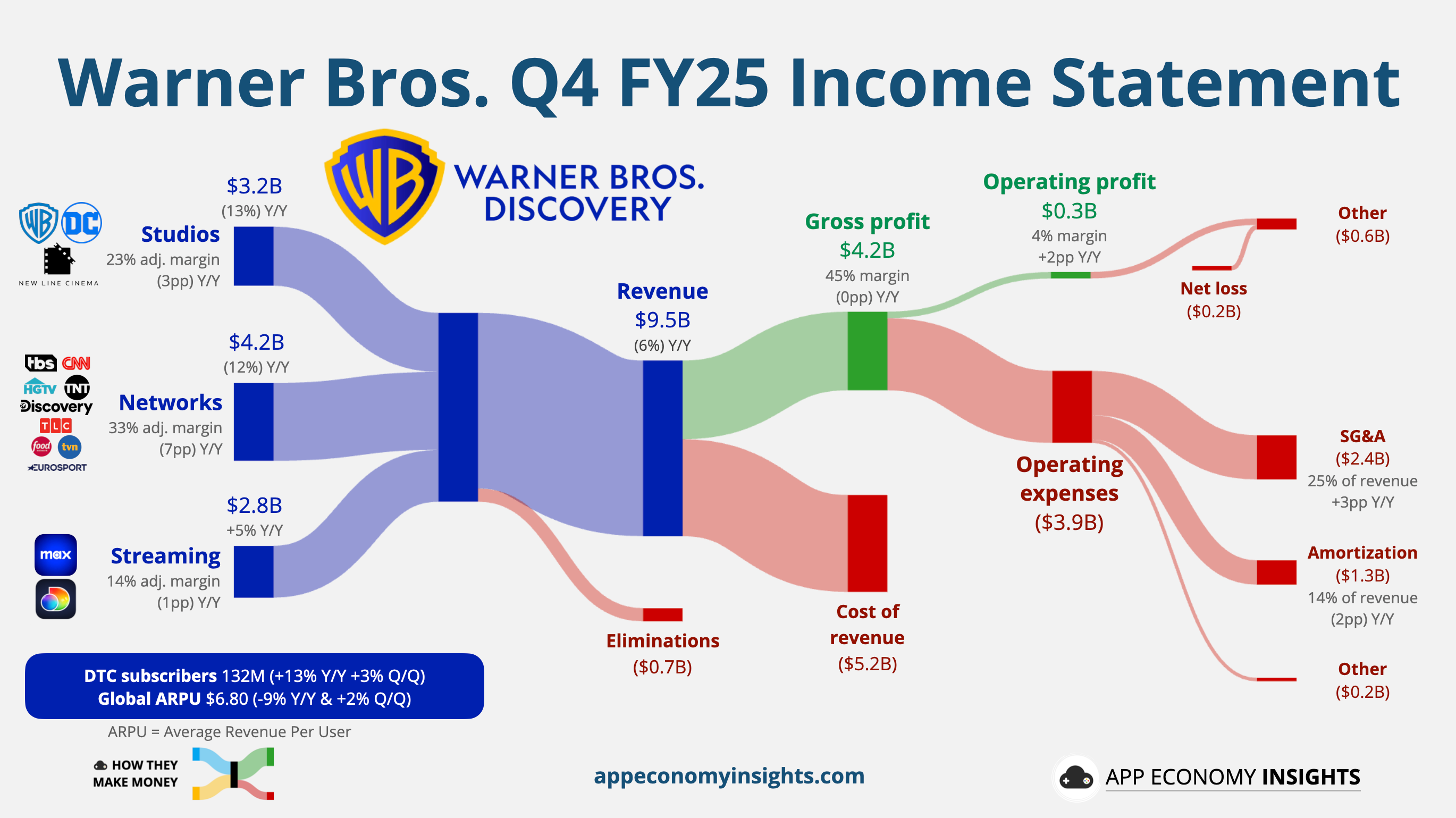

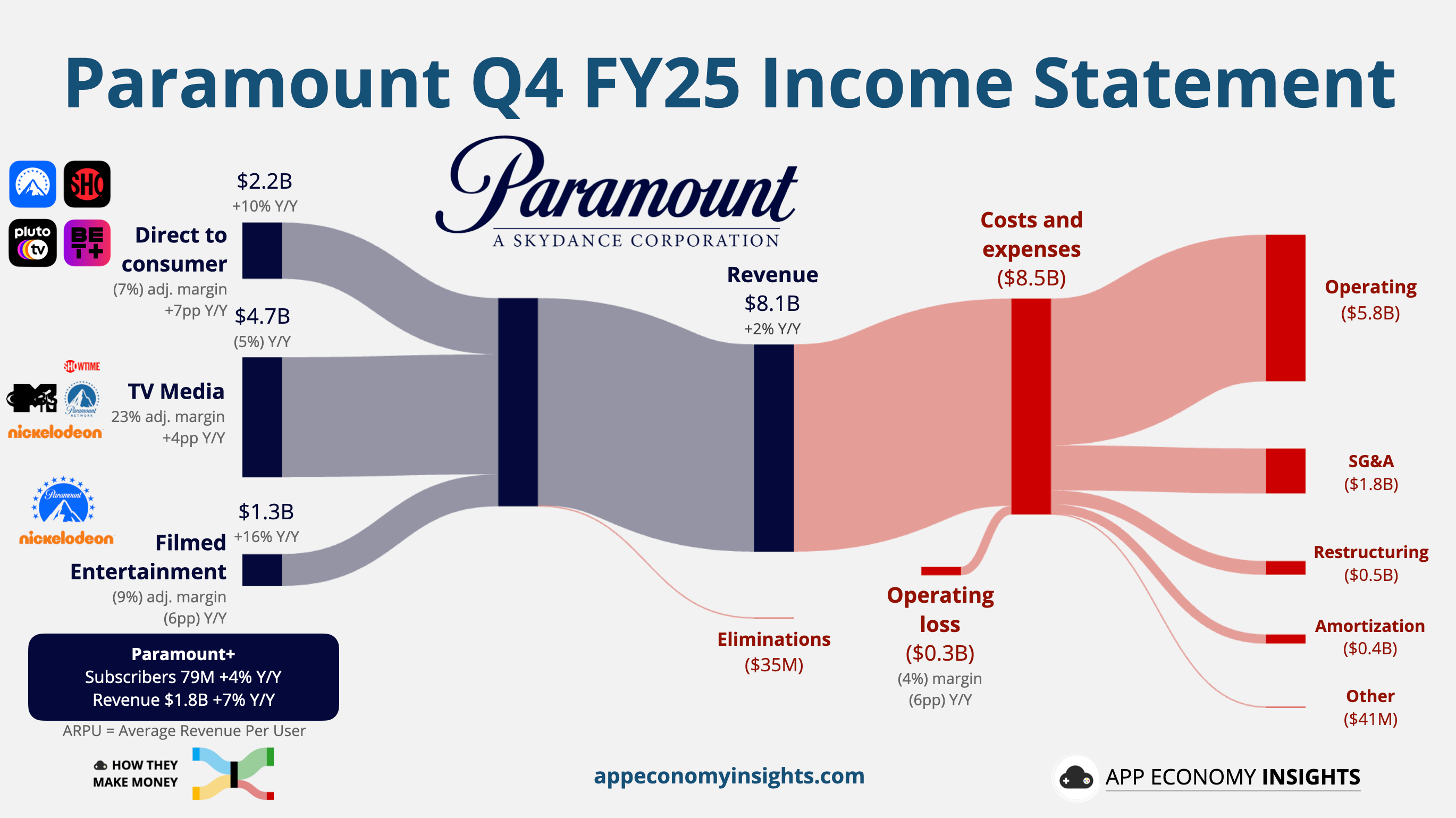

Let’s visualize the two companies:

3 similar segments:

📺 Linear TV: The lion’s share of revenue & profit, but declining.

🎥 Studios: Hit or miss based on new theatrical releases.

📱 Streaming: Slow-growing and low-margin for now.

Over 211 million direct-to-consumer (DTC) subscribers:

HBO Max & Discovery+: 132 million (+13% Y/Y).

Paramount+ 79 million (+4% Y/Y).

~$96 billion in net debt. This includes $39 billion in combined net debt as of December, $54 billion in new debt commitments, and the $2.8 billion breakup fee paid to Netflix. While Paramount claims a $79 billion pro forma net debt figure, that likely reflects creative accounting and aggressive exclusions.

Under $12 billion in adjusted EBITDA in FY25:

WBD: $8.7 billion, slowly declining in the past two years.

PSKY: $2.7 billion (with a $3.8 billion outlook for FY26).

In their official merger announcement, Paramount asked for a leap of faith.

Paramount is asking investors to trade on a 4x leverage hypothetical future while living in an 8x leverage present. The bridge between those two numbers starts with a staggering $6 billion in promised synergies. In an industry where integration is notoriously messy, it’s a high-stakes bet.

Are we supposed to believe EBITDA will leap from less than $12 billion to more than $20 billion while the core profit centers (linear networks) are in a freefall?

WBD and Paramount combined for ~$15 billion in SG&A expenses last year. In an industry with iron-clad union contracts and massive marketing requirements, cutting ~40% of overhead is a bold claim.

Netflix, the masters of tech efficiency, believed it could only find $2.5 billion in savings. Paramount is claiming it can find $6 billion. This $3.5 billion gap has our BS-meter working overtime.

It’s possible management is double-counting synergies across Paramount Skydance and the WBD merger. Warner has already been restructured multiple times and ultimately chose to sell itself. Finding another massive round of savings won’t be easy.

How many times can you make an organization leaner before something breaks?

The bull case pitched to investors

To justify the debt mountain, Paramount is pitching a very specific vision of the future.