👟 Nike: Topsy Turvy Turnaround

And Amazon Leo enters Starlink's orbit

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Anthropic’s Claude Code Leak

Anthropic just handed competitors a rare look under the hood of one of its most important products. During a software update, human error exposed roughly 500,000 lines of Claude Code-related source code, and the files were quickly mirrored across the internet.

Importantly, the leak did not expose Claude’s model weights. What spilled out was the product layer around Claude Code, including architecture details and unreleased features, giving rivals a clearer view into how Anthropic built one of the hottest coding agents in AI. Claude Code generates $2.5 billion in annual revenue, a figure that has doubled since January.

The timing is brutal. Anthropic is reportedly targeting a $380 billion IPO later this year. This lapse is especially awkward for a company that has tried to differentiate itself on safety and operational discipline.

It also comes as Anthropic fights the US government over its designation as a supply-chain risk after refusing certain military uses of its models. A federal judge has temporarily blocked that designation, but the broader clash with Washington remains an overhang.

Anthropic’s core pitch was never just model quality. It was also trust. Now it has to prove that trust can survive a very public operational failure.

Today at a glance:

👟 Nike: Topsy Turvy Turnaround

🛰️ Amazon: Delta Bets on the Underdog

🤖 OpenAI: The $122 billion Round

👟 Nike: Topsy Turvy Turnaround

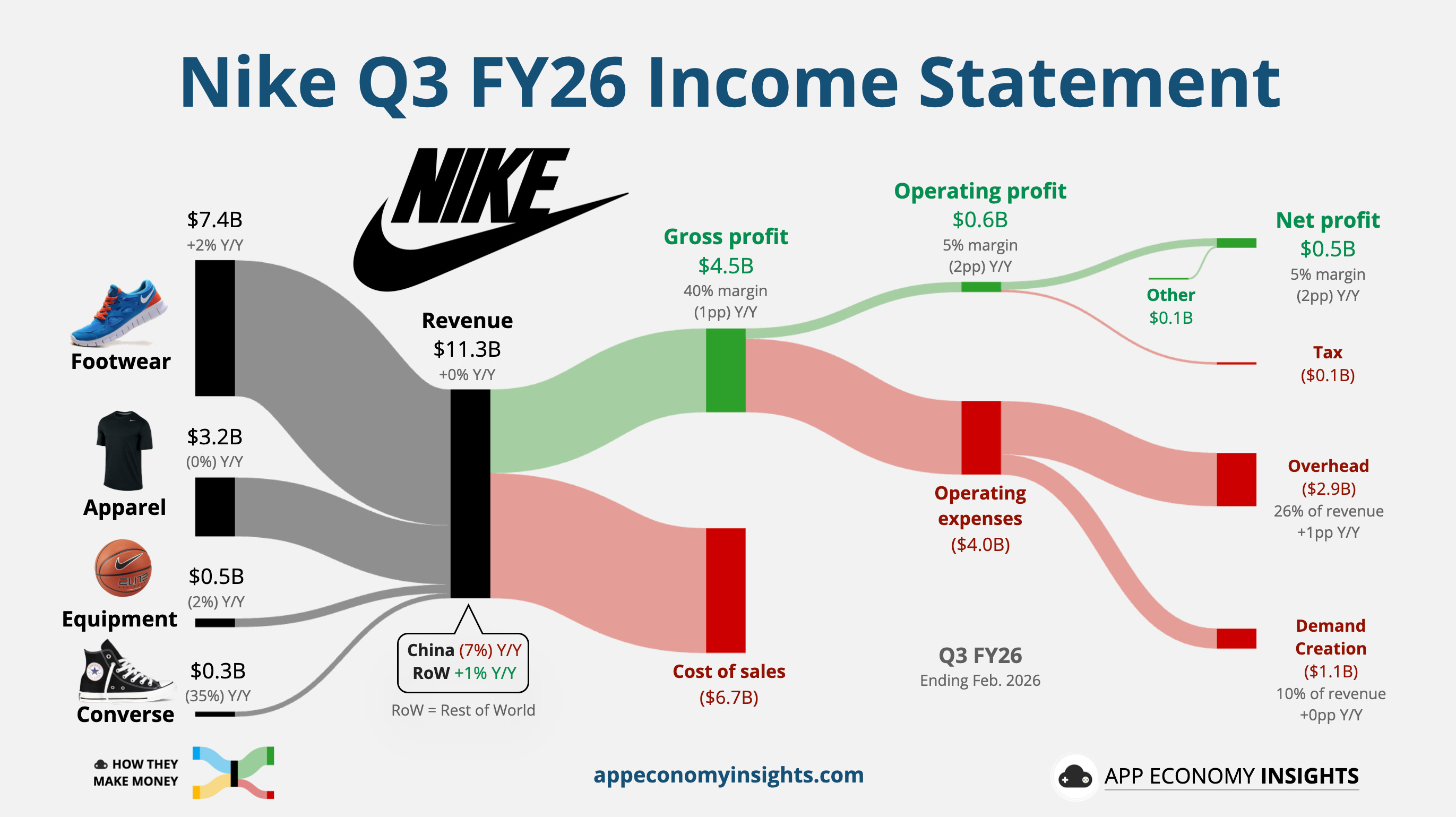

Nike’s February quarter looked better on the surface than underneath. Revenue was flat Y/Y at $11.3 billion ($50 million ahead of expectations), and earnings per share also cleared the consensus. But the stock still fell 15%, a sign investors remain unconvinced that the turnaround is gaining real traction.

The revenue beat deserves an asterisk. While reported revenue growth was flat, the top line actually declined 3% Y/Y in constant currency.

The bigger problem is margins. Gross margin fell to 40% as Nike leaned harder on wholesale (up 5%) and stepped back from higher-margin direct sales (down 4%). In other words, Nike’s product sales are steady, but moving through less profitable channels.

Nike is effectively trading direct sales for wholesale volume to clear inventory. While this keeps the Swoosh on shelves, it is a significant drag on the bottom line that has now persisted for six straight quarters.

International remains the bigger headache.

China sales fell 7% Y/Y as local competitors like Anta and Li-Ning continued to take share.

Meanwhile, the EMEA growth of 2% Y/Y missed estimates. The current quarter (Q4) will have to contend with the war in Iran, but Q3 results show Nike was already losing momentum in the region well before the conflict began.

North America showed a modest 3% gain, but it wasn’t enough to offset the persistent weakness elsewhere.

The weakness also goes beyond the core Nike brand. Converse revenue plunged 35% to just $264 million, another sign the company’s innovation and brand issues are broader than performance running alone.

Nike remains a ‘show me story.’ CEO Elliott Hill has been in the seat for 18 months. His comment that "the pace of progress is different across the portfolio" suggests a recovery taking much longer than anticipated. The stock just hit its lowest price since 2014, but ongoing earnings compression means it remains richly valued, well above 20x forward earnings. Until Direct stabilizes, this turnaround still looks incomplete. For now, Nike is still asking investors for patience.

🛰️ Amazon: Delta Bets on the Underdog

The space race used to be about national pride and planting a flag on the moon. In 2026, it’s all about who can stream 4K videos at 35,000 feet.

This week, Delta Air Lines announced a massive partnership with Amazon Leo (formerly known as Project Kuiper), a low Earth orbit satellite constellation. The plan is to bring high-speed Wi-Fi to 500 aircraft starting in 2028. For Amazon, this is a critical validation of its $10 billion satellite bet.

Amazon Leo is, of course, in direct competition with SpaceX’s Starlink. The disparity in raw infrastructure is almost comical. Starlink currently has over 10,000 operational satellites and has already signed up United, Southwest, and Air France. Amazon Leo has roughly 200. That said, Amazon is authorized to launch thousands more, aiming for a total network size that could eventually exceed 7,700 satellites.

Delta CEO Ed Bastian chose an ecosystem over a pure connectivity provider. By tapping Amazon, Delta integrates with AWS to personalize seat-back screens and bring Amazon’s content and shopping library directly into the cabin.

Earlier this year, Elon Musk publicly clashed with Ryanair’s Michael O’Leary after Ryanair passed on Starlink. Delta’s move shows that as competition expands, airlines may value broader commercial alignment as much as raw satellite scale.

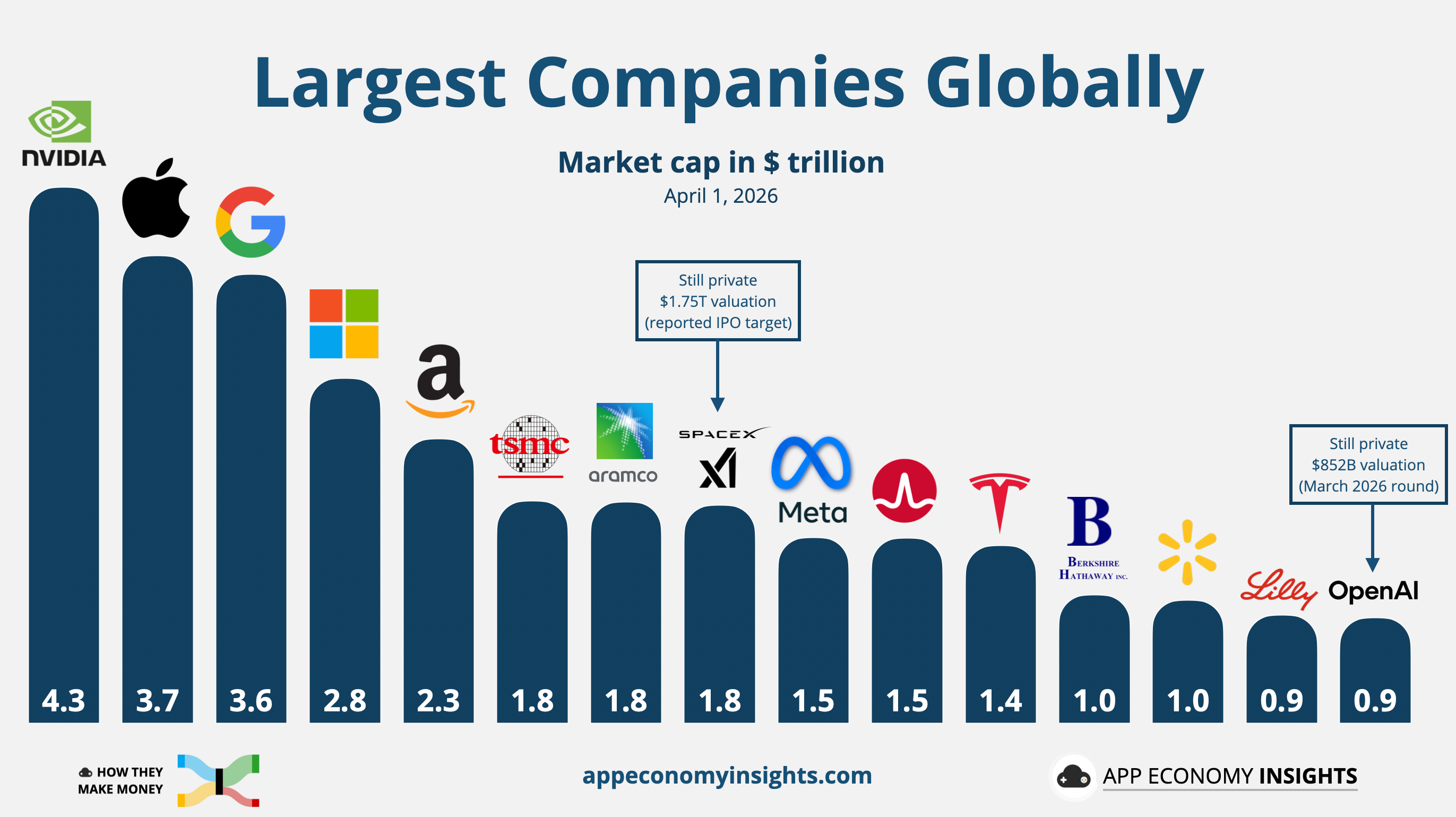

This deal arrives as SpaceX prepares for a historic 2026 IPO. Following its February merger with xAI, SpaceX is reportedly seeking a $1.75 trillion valuation and aiming to raise up to $75 billion. Starlink’s first-mover advantage is central to that bull case. But Delta’s decision shows Amazon does not need to match SpaceX satellite for satellite to win important customers. If AWS relationships, commerce, and content can help close the gap, the Starlink monopoly narrative starts to weaken.

🤖 OpenAI: The $122 Billion Round

OpenAI closed a staggering $122 billion funding round, catapulting its valuation to $852 billion. To put that in perspective, Sam Altman’s firm is now worth more than JPMorgan Chase and already sits among the 15 most valuable companies in the world.

OpenAI’s announcement read less like a press release and more like a draft for an IPO prospectus. The company touted:

900 million weekly active users (on track to hit 1 billion in 2026).

50 million paying subscribers.

$2 billion in monthly revenue (implying ~$24 billion ARR).

Growing 4x faster than Google or Meta did at the same stage.

Perhaps the most notable shift is in the revenue mix. Enterprise sales now account for 40% of the business and are on track to reach parity with consumer subscriptions by year-end. That helps explain the pivot to enterprise and coding.

This new war chest is meant to fund an AI infrastructure roadmap expected to require roughly $1.4 trillion over time.

The biggest checks came from three players. Amazon committed $50 billion, although $35 billion is tied to IPO or AGI milestones. NVIDIA and SoftBank each committed $30 billion.

Amazon and NVIDIA are not investing purely for financial return. They both benefit if OpenAI remains a major buyer of compute and infrastructure in a market where heavy AI spending lifts the whole ecosystem.

In a move typically reserved for public companies, OpenAI raised $3 billion directly from individual investors through bank channels and secured placement in Cathie Wood’s ARK ETFs. Bringing individual investors into the round does two things: it creates a larger base of brand evangelists and helps frame a future IPO valuation.

Still, private-market enthusiasm does not guarantee public-market upside. Plenty of companies that went public in 2022 ended up trading below their last private valuations. OpenAI may still command enormous demand when it lists, but what happens after the IPO debut is far less certain.

OpenAI now has the market cap of the incumbents and a CapEx plan that rivals the Mag 7. What it lacks is an incumbent-like cash machine. Quite the opposite: cash burn for 2026 alone is expected to exceed $14 billion.

That’s where the economics start to matter. Sacra estimates OpenAI’s gross margin was just 33% in 2025, well below the 46% target. Inference costs (the chips and electricity required to answer prompts) rose almost as fast as revenue. This is not the kind of high-margin model that powered Meta and Google in their early years.

To justify its latest valuation, OpenAI would need to generate $24 billion in profit, not in revenue. With margins like these, that points to a business closer to $250 billion in annual revenue, or about 10x today’s run rate.

That leaves little room for strategic misfires like Zuck’s Metaverse. Capital-intensive businesses cannot afford too many expensive detours, and OpenAI does not have Meta’s luxury of funding moonshots from a wildly profitable core business. The recent Sora stumble is a reminder that not every big bet will land, even with strong execution.

The $852 billion question is whether OpenAI can start generating real cash before investors start challenging the multiple.

That's it for today.

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own AAPL, GOOG, META, NVDA, and TSLA in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.

I just posted DCF valuation on my page, shares not undervalued

The flat margin growth makes sense, we’ve been seeing dozens of smaller names that are end-suppliers to Nike dilute their shares like crazy this year. Has been damn profitable shorting the cohort though haha