🕵️ Palantir: Tokens Are the New Coal

Why cheaper AI could boost demand

Welcome to the Premium edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

🗓️ It’s peak earnings season!

This week, we’ll visualize more than 50 reports ranging from Airbnb to Zillow.

Today, we break down some of the companies that already reported on what was an unusually busy Monday.

Today at a glance:

🕵️ Palantir: Tokens Are the New Coal

🦉 Duolingo: Top of Funnel Goes Flat

🛵 Grab: The Indonesia Overhang

📌 Pinterest: Buyback for the Ages

🕵️ Palantir: Tokens Are the New Coal

Palantir’s US business doubled in twelve months, and CEO Alex Karp says the company cannot meet demand.

CTO Shyam Sankar gave the framing of the quarter:

“Tokens are the new coal; AIP is the train.”

Inference costs are collapsing. GPT-4-equivalent performance is now roughly 1,000x cheaper than three years ago. As a result, the universe of agent workflows that make economic sense is expanding fast. That’s Jevons paradox. But it also comes with the risk of unreliable model output.

Now, Palantir’s AIP (Artificial Intelligence Platform) and the underlying ontology are the harness that makes raw model output safe enough to put into production. Every agent action is governed, attributed, and traceable. In short, the more abundant cheap tokens become, the more valuable the layer that turns them into deployable work.

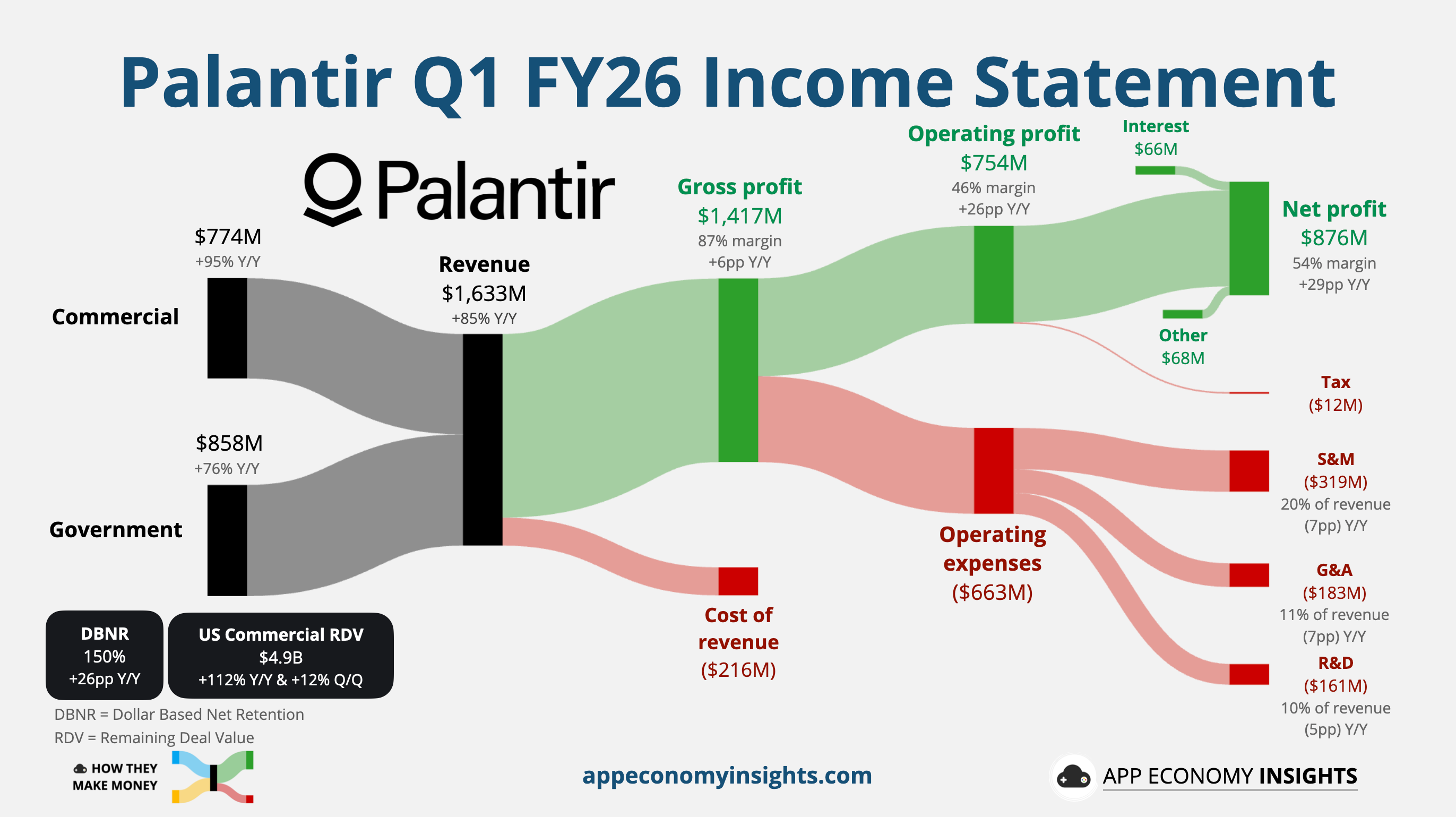

Q1 revenue grew 85% Y/Y to $1.63 billion ($90 million beat), Palantir’s fastest growth as a public company, and the 11th consecutive quarter of acceleration. Adjusted EPS came in at $0.33 ($0.05 beat). The Rule of 40 score hit 145, up from 127 last quarter, putting Palantir in rarefied air alongside NVIDIA, Micron, and SK Hynix.

Net dollar retention jumped to 150% (up from 139% in Q4 FY25), and adjusted free cash flow hit $925 million at a wild 57% margin.

The US is the story

The US now accounts for 79% of total revenue and surged +104% Y/Y.

💼 US Commercial: $595 million (+133% Y/Y, +18% Q/Q).

🪖 US Government: $687 million (+84% Y/Y, +21% Q/Q).

Management noted US Commercial growth would have been +143% Y/Y absent a large customer transitioning from commercial to government. International commercial, by contrast, grew just +26% Y/Y to $179 million — Europe remains the laggard, and Karp’s call commentary made clear he has limited patience for it.

The pipeline behind the print

Bookings matter more than revenue at this stage of the curve.

RDV (Remaining Deal Value) is Palantir’s total committed but not yet recognized revenue, indicating the visible runway. RDV nearly doubled to $11.8 billion. US Commercial RDV alone surged 112% Y/Y to $4.92 billion. That’s the cushion under FY26 guidance and the reason management keeps raising its outlook.

FY26 revenue is now expected to grow 71% Y/Y to $7.7 billion (compared to 61% previously). That includes a 120% growth to $3.2 billion for US Commercial.

Bottom Line: Palantir fundamentals have improved so much that even the nosebleed valuation has come down to ~70x forward EBITDA. That’s still high compared to the rest of the market, but not outrageous for a company expected to nearly double free cash flow this year.