📊 PRO: This Week in Visuals

AAPL MSFT META SAMSUNG LLY V MA ABBV KO AZN MRK KLAC TMUS VZ AMGN AIRBUS QCOM SNDK BKNG SPOT CDNS UPS HLT HOOD MDLZ GM F SBUX CMG RBLX SOFI TEAM RIVN ALGN DPZ ETSY TDOC

Welcome to the Saturday PRO edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Premium members get:

📊 Monthly reports: 200+ companies visualized.

📩 Tuesday articles: Exclusive deep dives and insights.

📚 Access to our archive: Hundreds of business breakdowns.

PRO members get everything PLUS:

📩 Saturday PRO reports: Timely insights on the latest earnings.

Today at a glance:

📱Apple: The Ternus Setup

☁️ Microsoft: The AI Bottleneck

🕶️ Meta: CapEx Spooks Wall Street

📱 Samsung: AI Chip Profits Explode

💊 Eli Lilly: GLP-1 Volume Engine Roars

💳 Visa: Fastest Growth Since 2022

💳 Mastercard: Cross-Border Cracks Show

⏳ AbbVie: Skyrizi and Rinvoq Deliver

🥤 Coca-Cola: Affordability Momentum

🧬 AstraZeneca: Oncology Carries Again

🦠 Merck: Bridge Drugs Show Traction

🔬 KLA: Demand Visibility Extends

📶 T-Mobile US: Accounts Over Lines

📡 Verizon: Schulman's Early Win

🧬 Amgen: Growth Outrun Patent Cliff

🛩️ Airbus: Engine Shortage Bites

📲 Qualcomm: Data Center Lights Up

💾 Sandisk: Memory Trade

🏝️ Booking: Middle East Cuts the Cycle

🎧 Spotify: Guidance Hits the Skip Button

💡 Cadence: Hexagon Mutes the AI Tailwind

📦 UPS: Transition Quarter

🏨 Hilton: US Demand Snaps Back

🪶 Robinhood: Crypto Drag, Prediction Surge

🍪 Mondelez: Cocoa Cost Hangover Lingers

🚗 GM: Iran Cost Spike

🚙 Ford: One-Time Boost Lifts Guide

☕️ Starbucks: The Turn Arrives

🌯 Chipotle: Comps Turn Positive Again

👾 Roblox: Safety Hits New Users Growth

🏦 SoFi: Strong Quarter Wrong Reaction

☁️ Atlassian: Cloud Reaccelerates Hard

⚡ Rivian: R2 Production Begins

🦷 Align: Volume Holds But US Softens

🍕 Domino’s: Macro Bites Into Comps

📦 Etsy: Marketplace Returns to Growth

🩺 Teladoc: BetterHelp Insurance Scales

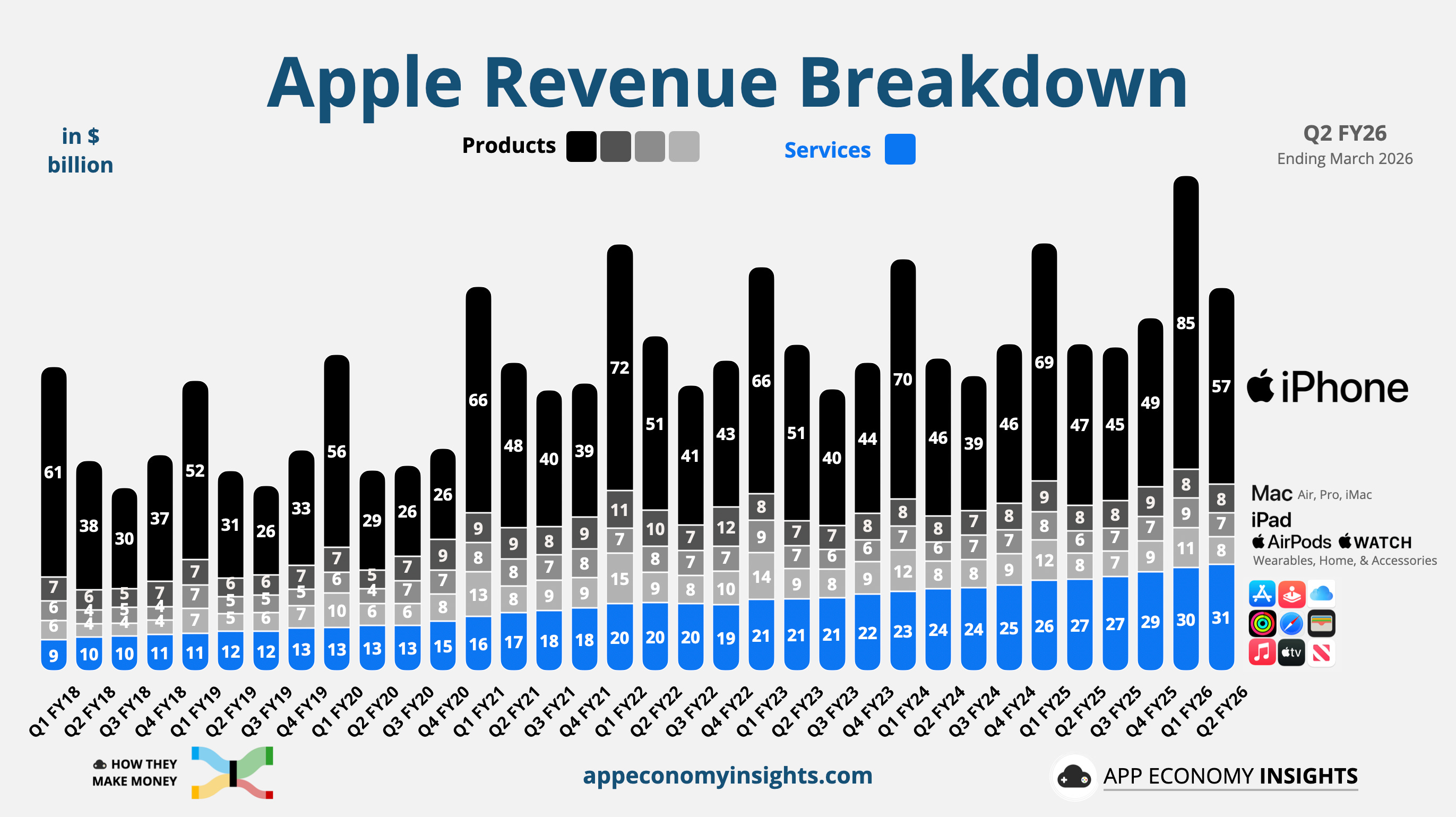

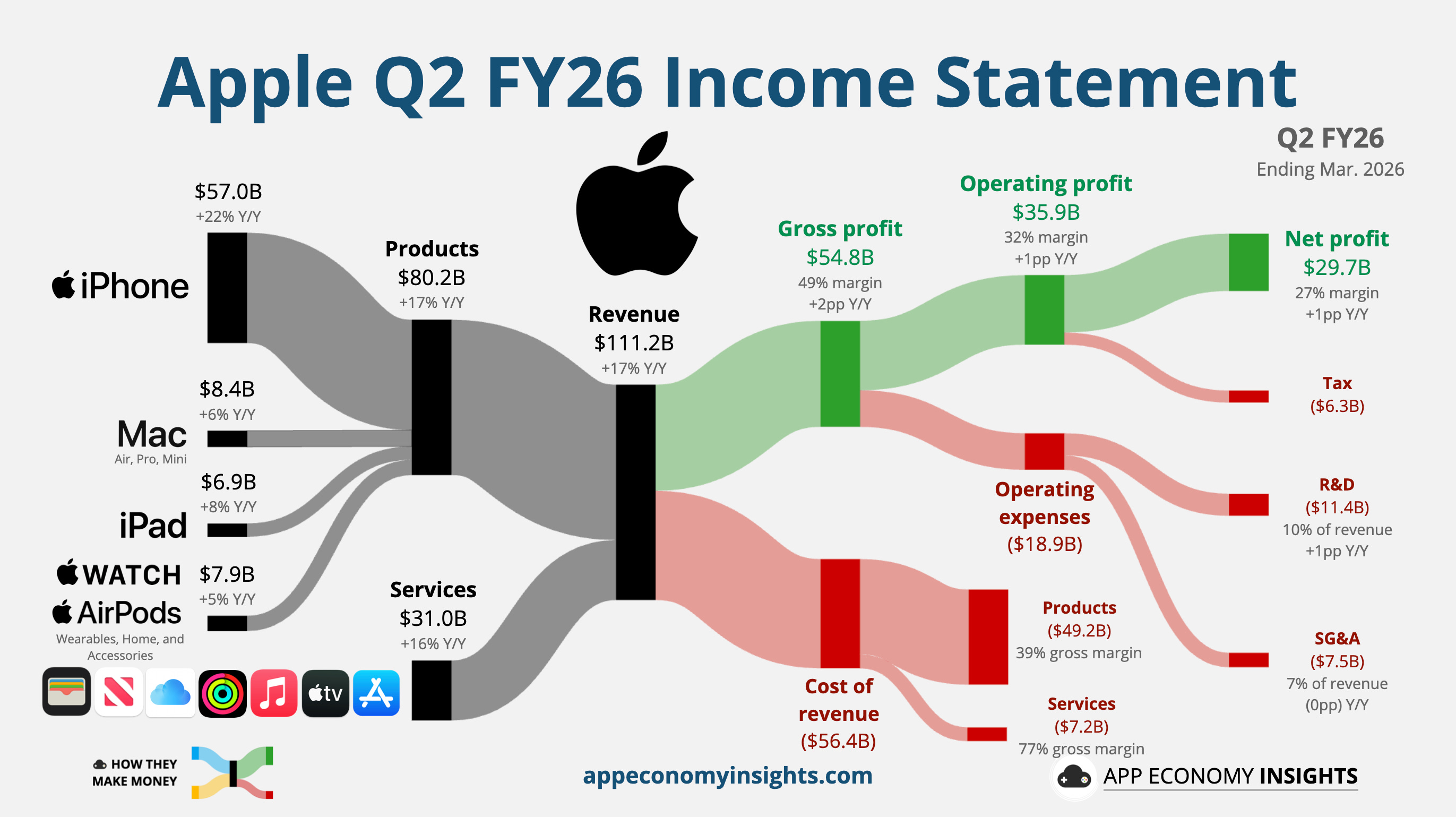

1. 📱Apple: The Ternus Setup

Apple's Q2 revenue rose 17% Y/Y to $111.2 billion ($1.6 billion beat) and adjusted EPS was $2.01 ($0.07 beat). These were March quarter records despite supply constraints.

iPhone revenue grew 22% to $57.0 billion.

Services accelerated 16% to a record $31.0 billion.

China rebounded 28% to $20.5 billion.

As we covered last week, CEO Tim Cook will step down on September 1, with hardware chief John Ternus taking over.

Two structural shifts arrived alongside the print:

First, Apple ended its "net cash neutral" capital return policy. It was a 2018 pledge to return every excess dollar to shareholders until cash on hand matched debt. That commitment shrank Apple's net cash from $151 billion in 2018 to $62 billion today. Going forward, Apple will manage cash and debt independently and will no longer be obligated to return excess cash. The board still authorized $100 billion in fresh buybacks and a 4% dividend hike, but Q2 buybacks were cut in half despite free cash flow growing 28% Y/Y, signaling Apple wants to deploy its cash differently for the first time in years.

Second, R&D spending jumped 34% Y/Y. Historically, Apple has run lean on R&D, and the surge suggests the company might be ready to ramp up its spending.

Cook said memory costs will be “significantly higher” in Q3 (June quarter) and worsening beyond, a growing margin headwind. He didn’t commit to whether Apple will raise prices. Mac supply constraints (Mac Mini, Mac Studio, MacBook Neo) are expected to last “several months.” Despite all that, Apple guided Q3 revenue growth to 14%–17%, well above the ~9% consensus.

The setup for the Ternus era is becoming clearer. Apple has a record installed base of 2.5+ billion devices, a balance sheet with more flexibility, and a growing need to catch up in AI. Ending the net-cash-neutral policy gives the company more room to maneuver. The obvious question: is Apple preparing to deploy more capital toward AI, M&A, or a broader product reset?

The next iPhone cycle may reset expectations, but only if the Gemini-powered Siri overhaul convinces users that Apple’s AI gap is finally closing.

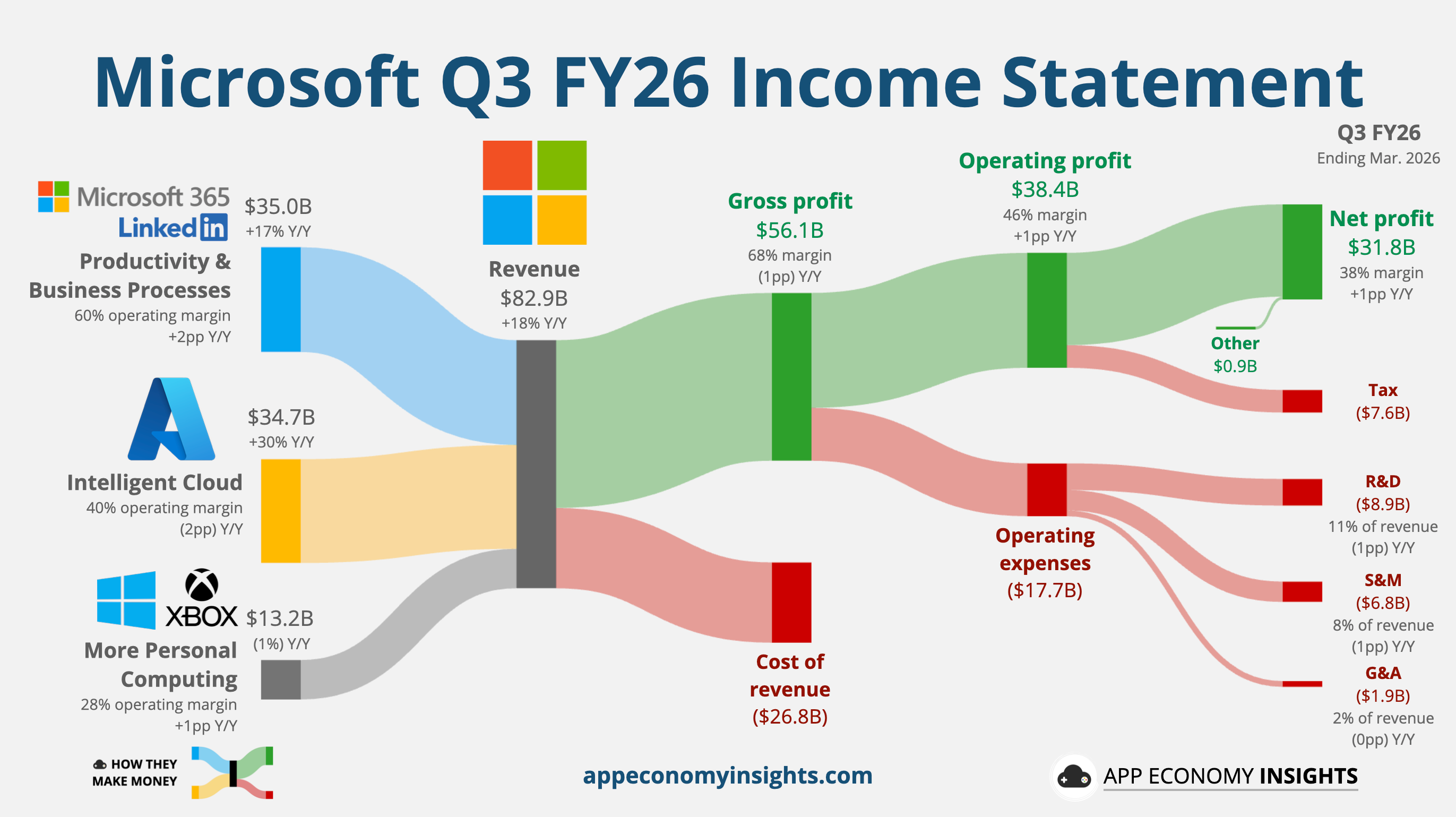

2. ☁️ Microsoft: The AI Bottleneck

Microsoft’s quarter was strong, but the AI story is shifting from demand to deployment. Q3 revenue rose 18% Y/Y to $82.9 billion ($1.5 billion beat), and GAAP EPS was $4.27 ($0.22 beat).

Azure grew 39% Y/Y in constant currency, narrowly ahead of consensus.

The AI business reached $37 billion in ARR, up 123% Y/Y.

Copilot paid users rose to 20 million, still only ~4% of Microsoft’s 450+ million paid M365 commercial seats.

OpenAI stake: Unlike Alphabet and Amazon, Microsoft didn’t show a massive “other income” windfall from its private equity bets this quarter. OpenAI’s historic $122 billion round valuing the company at $852 billion closed too late to be booked in the March quarter. This means Microsoft’s 27% stake is due for a massive upward adjustment that will likely distort GAAP net income in the June quarter, similar to the “Anthropic bump” Alphabet and Amazon just booked.

The CapEx story is the dominant narrative. Q3 CapEx was $31.9 billion, 8% below projections due to timing, not lower ambition. Management also disclosed a ~$190 billion CapEx outlook for calendar 2026, including $25 billion tied to higher component pricing. The implied ramp is steep, raising a simple question: Can Microsoft turn spending into usable capacity fast enough?

Two strategic shifts occurred this quarter.

Microsoft and OpenAI signed a revised agreement that ends OpenAI's revenue-share payment to Microsoft after 2030, in exchange for extending Microsoft's royalty-free access to OpenAI's frontier models through 2032. It resolves months of tense negotiations that had led OpenAI to consider antitrust action.

CEO Satya Nadella signaled a structural pricing model shift: per-seat licensing is migrating toward “per user and usage”, with GitHub Copilot already transitioning. This could be a boon for monetization.

The company is also adapting its organization. Hood flagged ~$900 million in Q4 one-time costs from a voluntary retirement program covering ~7% of US-based employees.

Microsoft guided Q4 revenue growth of 13–15%, with Azure expected at 39–40% in constant currency. The contrast with cloud peers matters: AWS and Google Cloud both reported stronger acceleration this week, so at face value, it makes Microsoft look like an AI laggard.

The nuance lies in capacity. Nadella and Hood were explicit: demand for AI and cloud services continues to exceed supply. Microsoft appears sold out in several key regions, so Azure’s ~40% growth may be less a demand ceiling than a physical ceiling. The company can’t plug in GPUs and open data centers fast enough. That’s the AI Power Grid problem.

The bull case remains intact. Microsoft has $627 billion in remaining performance obligations, nearly doubling Y/Y. But the next phase depends on execution: converting backlog into revenue, bringing capacity online, and proving that AI monetization can outpace the infrastructure bill.