🤖 NVIDIA: Gone Parabolic

Agentic AI fuels the token economy

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

🚀 SpaceX just published its S-1 filing, so we’ll spend the next few days digging into what could become the biggest IPO ever. Stay tuned for our full breakdown next week with the signature visuals you know and love.

“Demand has gone parabolic.”

That was Jensen Huang’s closing message after NVIDIA’s Q1 FY27 earnings call.

His explanation was simple: agentic AI has moved from promise to production, turning token generation into a revenue stream.

That’s the clearest expression yet of NVIDIA’s token economy thesis. Compute is no longer just infrastructure spending. It is becoming the raw material for AI revenue.

Let’s break down the quarter.

Today at a glance:

NVIDIA’s Q1 FY27

Business highlights

Key quotes from the call

What to watch moving forward

FROM OUR PARTNERS

“The Biggest Gold Mine…in History”

That’s what NVIDIA’s CEO just said about today’s AI roll-out. And stock market experts say it could send AI and robot companies’ shares soaring on a “multiyear supertrend.”

The problem? Most of these companies are already priced for the hype in the public markets.

But 40K+ investors are finding a different, early way in through Miso Robotics, a still-private company that NVIDIA handpicked to collaborate with on AI robots for the $1T fast-food industry.

Miso’s Flippy fry station AI robot can boost restaurant profits by up to 3X, and it’s already fried 5M+ baskets of food in real kitchens for brands like White Castle. Now, with new customers like Jersey Mike’s, Cinnabon, and Jamba, Miso is going after a huge $4B/year US revenue opportunity.

Industry powerhouse Ecolab already invested. Hurry to join them as a Miso shareholder today.

This is a paid advertisement for Miso Robotics’ Regulation A offering. Please read the offering circular at invest.misorobotics.com

1. NVIDIA Q1 FY27

NVIDIA’s fiscal year ends in January, so the April quarter was Q1 FY27.

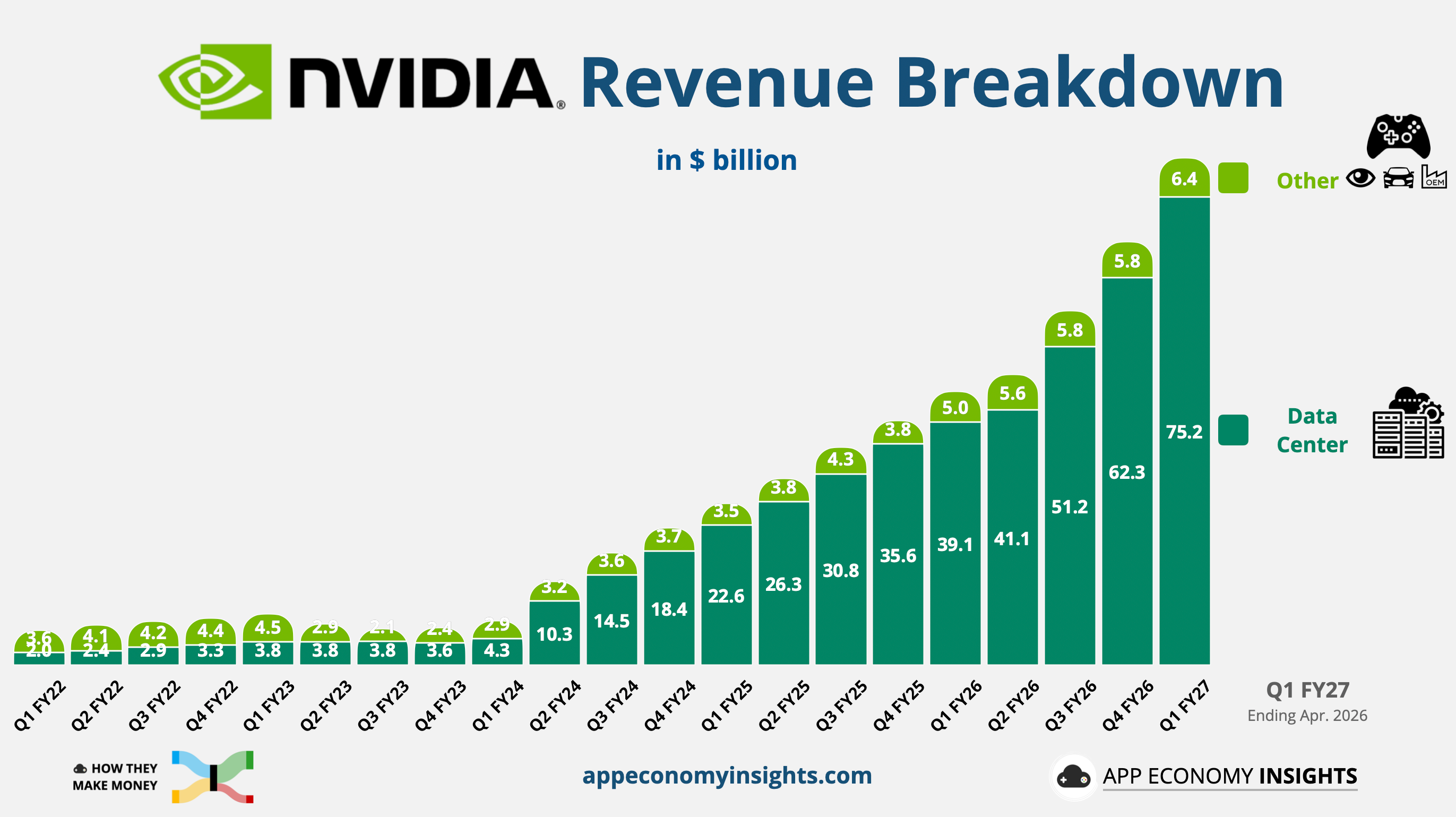

Data Center revenue remains off the charts, as illustrated below.

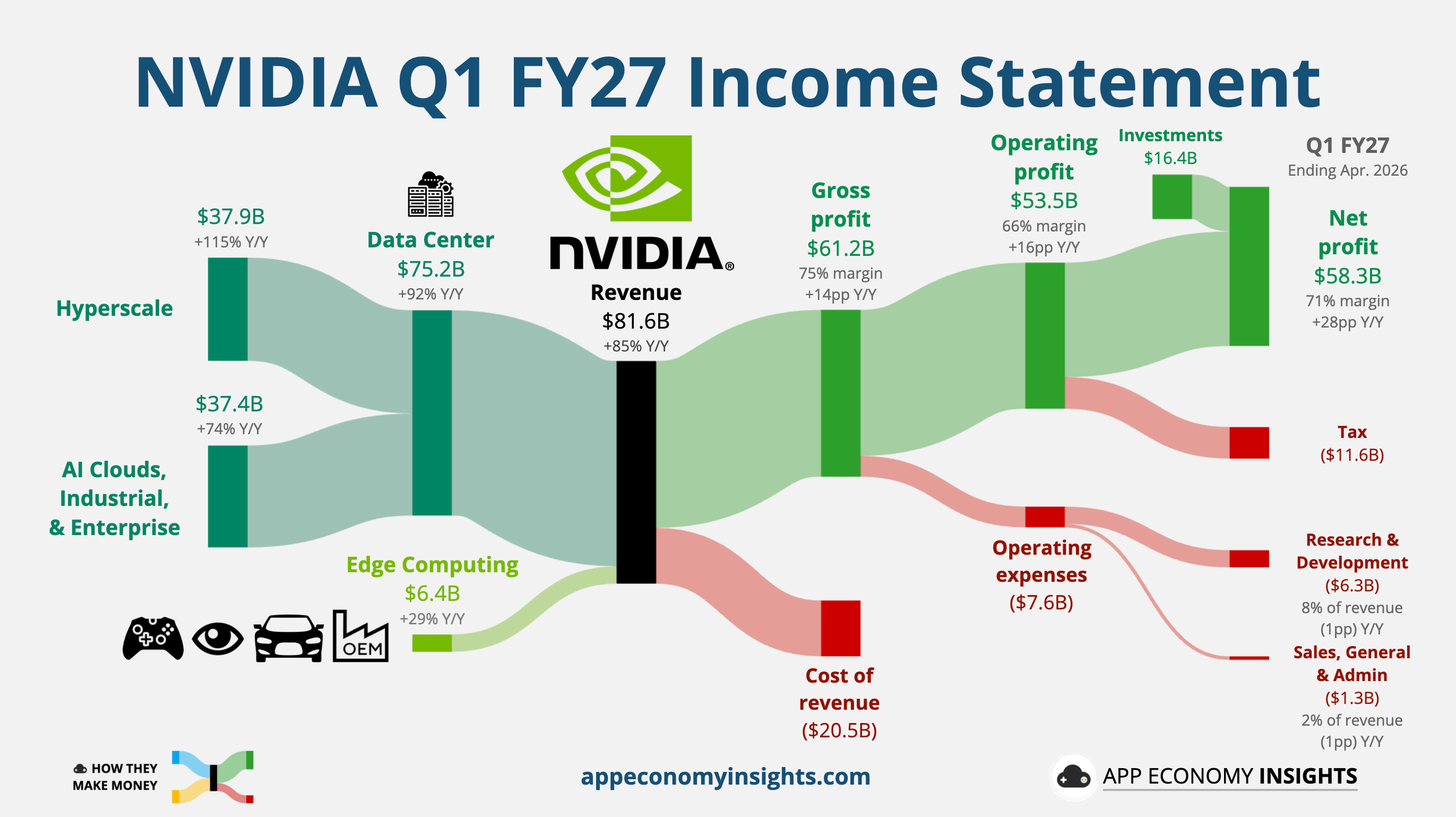

Income statement:

Revenue accelerated +85% Y/Y to $81.6 billion ($2.6 billion beat).

Data Center +92% Y/Y to $75.2 billion.

Edge Computing +29% Y/Y to $6.4 billion.

Gross margin was 75% (+14pp Y/Y).

Operating margin was 66% (+16pp Y/Y).

Non-GAAP EPS $1.87 ($0.10 beat).

Cash flow:

Operating cash flow +84% Y/Y to $50.3 billion.

Free cash flow +86% Y/Y to $48.6 billion.

Balance sheet:

Cash and cash equivalents: $80.5 billion.

Debt: $8.5 billion.

Q1 FY27 Guidance:

Revenue +11% Q/Q and +95% Y/Y to $91.0 billion ($3.0 billion beat).

Gross margin 75% (flat Q/Q).

So, what to make of all this?

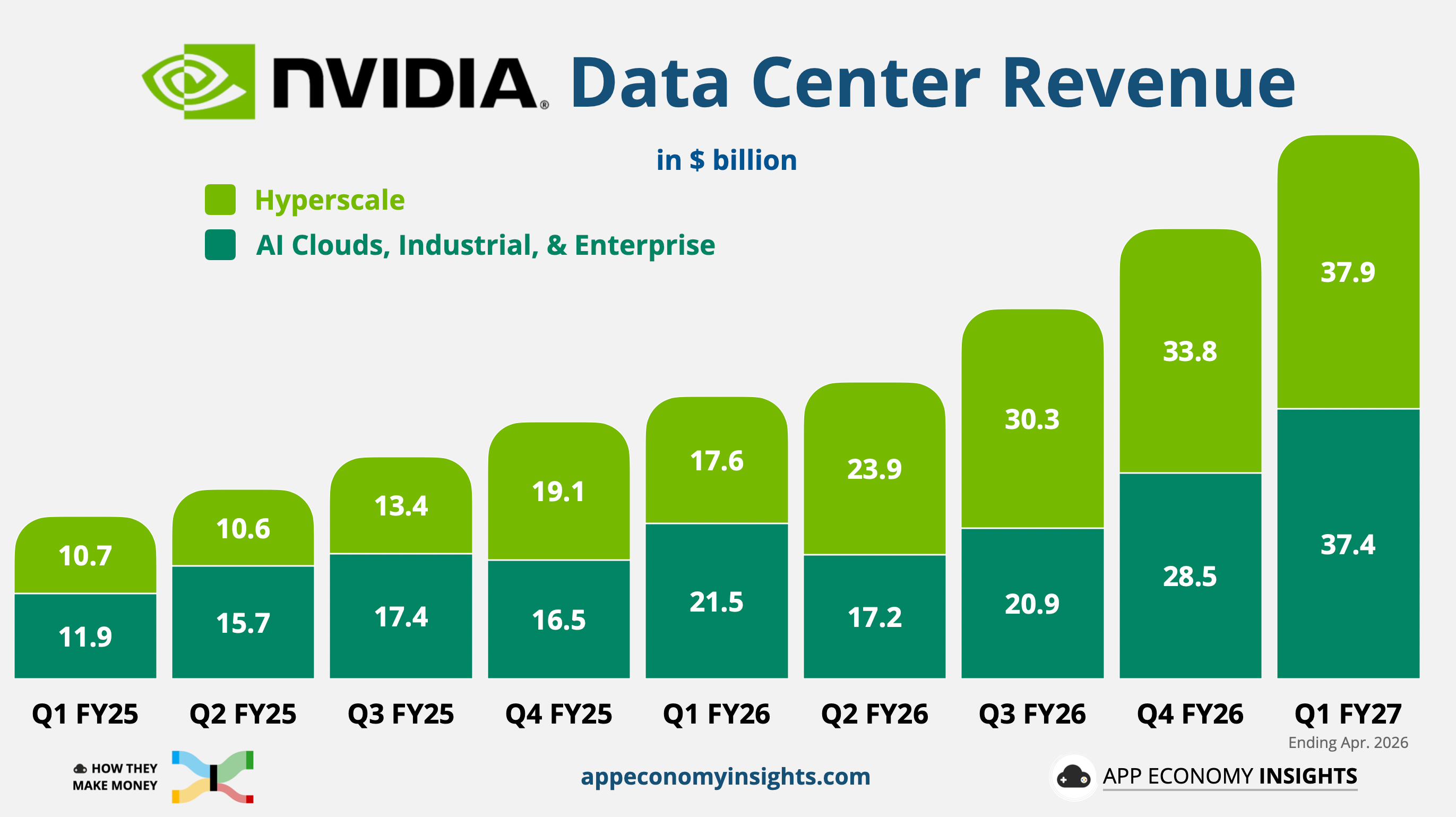

⚙️ Data Center is still the whole story: Data Center revenue surged 92% Y/Y to $75.2 billion and now represents 92% of the business. NVIDIA also changed its breakdown (previously Compute vs. Networking), shifting the focus from what it sells to who is building AI factories:

Hyperscale surged 115% Y/Y to $37.9 billion, driven by customers like AWS, Azure, and Google Cloud.

AI Clouds, Industrial, and Enterprise was nearly as large, rising 74% Y/Y to $37.4 billion. This segmentation helps counter the notion that NVIDIA relies solely on a handful of Big Tech buyers. Demand is broadening across neoclouds, sovereign AI, industrial deployments, and enterprise customers.

🧠 Inference is becoming the engine: NVIDIA’s growth is no longer just about training bigger models. As AI apps move from chatbots to agents, every query, image, video, and coding task requires real-time compute. That is why Jensen keeps framing AI infrastructure around tokens, not chips.

📈 Margins remain the lie detector: Gross margin stayed at 75% despite the complexity of the Blackwell ramp, higher memory content, and the shift toward full rack-scale systems. If competition were biting or demand were softening, margins would likely show it first.

💰 Cash flow is becoming absurd: Free cash flow nearly doubled to $48.6 billion in a single quarter. NVIDIA is not just growing revenue. It is converting that growth into cash at a scale that provides strategic flexibility for supply-chain investments, partnerships, and ecosystem support.

💼 Investment gains flattered reported profits: Net profit of $58.3 billion included nearly $16 billion in equity investment gains. NVIDIA did not break them out by company, but the large publicly disclosed holdings include Intel, CoreWeave, and Coherent, with Intel likely the biggest contributor in Q1.

🔮 The $91 billion guide raises the bar again: Guidance implies an 11% sequential increase and 95% Y/Y growth. The bigger NVIDIA gets, the harder it should be to keep compounding at this pace. Yet guidance still implies faster Y/Y growth.

Big picture: NVIDIA’s Q1 FY27 results support the same message Jensen delivered at GTC. The AI boom is moving from training clusters to full AI factories built for inference, agents, and token generation. The numbers suggest the cycle is still expanding, not digesting.

2. Business highlights

🇨🇳 China becomes a call option

China is no longer a clean zero, but it is not back either.

The US has reportedly cleared H200 sales to roughly 10 Chinese companies, including Alibaba, Tencent, ByteDance, and JD.com. But the chips have not shipped yet because Beijing has not given the green light, partly because it wants local companies to rely more on domestic alternatives.

NVIDIA is still assuming no China Data Center compute revenue in its outlook. That creates an unusual setup. The business is accelerating without China, while any actual restart would become incremental upside.

The key point is that NVIDIA is winning without China. If China reopens even partially, it becomes a call option on top of an already booming business.

🧠 Vera opens a new growth layer

The most surprising development from the call may have been NVIDIA’s CPU ambitions.

Management said Vera opens a $200 billion TAM and that NVIDIA has visibility to nearly $20 billion in standalone CPU revenue this year. That would push NVIDIA into a market it has never meaningfully addressed before.

Vera is more than a companion chip for Rubin. It could become a new growth pillar across AI factories, storage, security, and confidential computing.

🏭 AI factories go physical

NVIDIA announced a strategic partnership with IREN to support the deployment of up to 5 gigawatts of NVIDIA DSX-aligned AI infrastructure across IREN’s data center pipeline. NVIDIA also received a five-year right to buy up to 30 million IREN shares at $70. Since the stock trades below that level, this is less a near-term investment than an upside kicker if IREN becomes a major partner.

This is the AI factory thesis in action. The bottleneck is no longer just access to GPUs. It is power, land, cooling, networking, deployment speed, and operating know-how.

The deeper NVIDIA moves into the factory layer, the more its moat depends on the entire deployment stack rather than any single chip.

3. Key quotes from the earnings call

Check out the earnings call transcript on Fiscal.ai here.

CEO Jensen Huang:

On the token economy:

“AI can now do productive and valuable work. Tokens are now profitable. Model makers are in a race to produce more. In the AI era, compute capacity is revenue and profits.”

Jensen says the AI boom has shifted from experimentation to monetization. If tokens can be produced profitably, compute becomes the constraint on revenue growth. Bears see hyperscaler spending as a cost. Jensen sees compute as the input required to generate AI revenue.

On the CPU opportunity:

“The world has billions of human users. My sense is that the world is going to have billions of agents. [...] Every one of those agents are going to spin off sub-agents, and every time they spin these off, you're going to need to do inference. That's where the thinking happens. All of the thinking happens on GPUs. All of the orchestration essentially runs on CPUs.”

This is the simple mental model for Vera: GPUs do the thinking, while CPUs coordinate the work. As agents use tools, browse the web, call compilers, manage memory, and spin up sub-agents, NVIDIA sees a growing need for CPUs built specifically for agentic AI.

4. What to watch next

NVDA is up nearly 20% YTD, still outperforming the S&P 500 by a wide margin. The index is less than 8%. The latest 13F filings for Q1 2026 showed that some funds were still buying, such as Altimeter and Tiger Global. The stock remains one of the most widely held names, although many funds are still underexposed relative to its 8% weight in the S&P 500.

At ~27x forward earnings, NVIDIA continues to trade mostly in line with the rest of Big Tech. With adjusted EPS surging 140% Y/Y, you could certainly argue it looks cheap. NVIDIA’s growth is supply-constrained. That means quarter-to-quarter noise matters less than understanding how long this cycle can run and what the business looks like when demand normalizes.

Here’s what I’m watching:

ACIE growth: NVIDIA’s new disclosure shows that AI Clouds, Industrial, and Enterprise are nearly as large as Hyperscale, and growing faster sequentially. If this continues, it would support the idea that the AI buildout is broadening beyond hyperscaler CapEx.

Rubin cadence: Vera Rubin production shipments are expected to begin in Q3 and ramp into Q4. A clean handoff from Blackwell to Rubin would support NVIDIA’s $1 trillion Blackwell and Rubin revenue outlook through 2027. A delay could create the demand air pocket that bears have been waiting for.

Token economics: Jensen says tokens are now profitable, but the real test is whether AI labs and AI-native companies can turn token revenue into durable profits after compute, R&D, and customer acquisition. NVIDIA is proving the infrastructure demand. Some customers still need to prove the business model.

📉 The bear case is that AI infrastructure demand eventually normalizes.

📈 The bull case is that agentic AI turns compute into a new industrial base.

NVIDIA is building for the latter.

That’s it for today!

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own AAPL, AMD, AMZN, GOOG, META, MSFT, and NVDA in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.