🔒 Micron: Locking In the Boom

The memory crunch reaches your pocket

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Apple is raising iPhone prices, and the culprit is memory.

For decades, memory was the invisible commodity inside every device: cheap, abundant, and easy to ignore. Not anymore. A brutal memory crunch is quietly pushing up the price of nearly every device you own, as the world’s top tech giants fight for supply and leave smartphones, PCs, and automotive lines competing for what remains.

That squeeze has a winner on the other side.

Micron just reported the most extraordinary quarter in its history.

Here’s what stood out.

Today at a glance:

☁️ Micron’s blowout quarter

🔒 Trying to break the cycle

🌐 The squeeze everyone else feels

🔭 What to watch next

FROM OUR PARTNERS

Cloud Created AWS. AI is Building the Next Empire.

AWS built an infrastructure for the cloud and became one of the most valuable businesses in history. The segment made $128 billion in sales for 2025.

Now, another company is building what could be an equivalent infrastructure: a new highway for AI.

Traditional AI data centers are massive, take 3 to 7 years to build, and disrupt communities. But BluSky AI has designed a prefabricated SkyMod system: small footprints, powerful, and purpose-built for AI workloads. These data centers take months to stand up, not years.

Hundreds of thousands of enterprises use AWS to power their business. BluSky AI’s robust portfolio of sites will create new onramps for AI’s urgent needs. Invest in BluSky AI as they unlock a power source for 417M+ companies using AI.

This is a paid advertisement for BluSky AI Regulation A offering. Please read the offering circular at https://invest.bluskyaidatacenters.com/

☁️ Micron’s blowout quarter

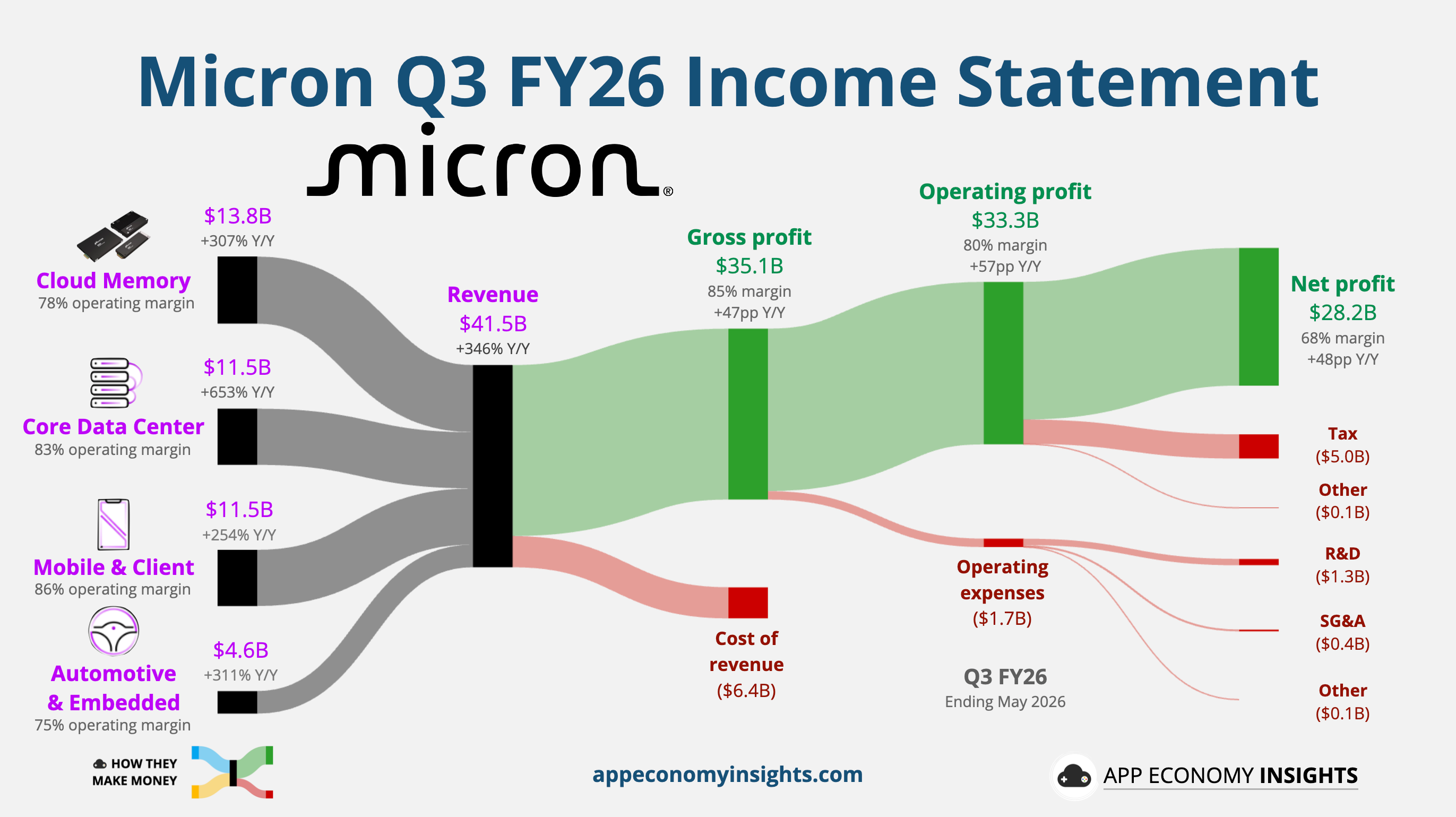

Micron’s fiscal Q3 (ended May 28) was extraordinary by any standard.

Revenue: The top line surged +346% Y/Y to $41.5 billion ($5.6 billion beat).

☁️ Cloud Memory: $13.8 billion (+307% Y/Y).

🖥️ Core Data Center: $11.5 billion (+653% Y/Y).

📱 Mobile & Client: $11.5 billion (+254% Y/Y).

🚗 Automotive & Embedded: $4.6 billion (+311% Y/Y).

Margin trends: Gross margin was 85% (more than doubled Y/Y). Operating margin was 80% (+57pp Y/Y). These NVIDIA-esque margins drove earnings per share up 106% sequentially to $25.11 ($4.25 beat).

Cash flow: Operating cash flow was $25.4 billion (+451% Y/Y). Adjusted free cash flow was $18.3 billion (vs. just $1.9 billion a year ago).

Balance sheet: Cash, marketable investments, and restricted cash reached $30.2 billion. Long-term debt was $5.1 billion (down from $14.0 billion a year ago).

Q4 FY26 guidance: Revenue ~$50.0 billion (~$6 billion above consensus). Gross margin ~86%. EPS ~$31 (vs ~$25.72 expected).

Almost none of the outperformance came from selling more chips. DRAM bit shipments rose only in the low single digits, yet DRAM prices jumped more than 60% in a single quarter, and NAND prices rose in the mid-80s%. Micron is already capacity-constrained, so the shortage isn’t showing up in units. It’s showing up in price.

Now step back and look at the scale.

Micron booked more revenue in three months ($41.5 billion) than in any full fiscal year through 2024, and its data center business alone cleared a $100 billion annualized run rate. A year ago, total quarterly revenue was $9.3 billion.

The market has noticed. Shares are up more than 8X over the past 12 months and jumped as much as 16% after this print. A company worth roughly $150 billion a year ago is now worth close to $1.3 trillion. It’s the kind of move investors usually associate with platform companies, not memory cycles.

🔒 Trying to break the cycle

The numbers are staggering. The strategy behind them is the actual story.

Memory has always been boom-bust: demand surges, the survivors overbuild, prices crater, everyone bleeds. The cycles culled the field to three main players: Micron, Samsung, and SK Hynix. Their shared discipline on supply is what keeps it tight. For 40 years, the industry’s curse was that every boom financed the next bust. This quarter, Micron tried to turn customer panic into a new floor.

The mechanism is the Strategic Customer Agreement (SCA). It’s a multi-year, take-or-pay contract locking in both volume and price, unlike the one-year handshakes the industry has always run on. Micron has now signed 16, typically five-year deals running through 2030. They already cover ~20% of its DRAM and a third of its NAND, with management targeting 40%+ of total revenue. Customers are backing them with ~$22 billion in deposits and guarantees, including roughly $18 billion of it in cash.

The largest deals set a ceiling at today’s prices, and a floor beneath them. Micron says that even at the floor, gross margins would sit well above its prior cyclical peak of ~60%. For the covered volumes, the old ceiling is effectively the new floor. The minimum value of these contracts is ~$100 billion, which management calls a conservative number, not a forecast.

The most telling example is Anthropic, with a memory and storage supply agreement paired with Micron’s investment in the AI lab’s Series H round. A memory maker buying equity in the very demand it’s trying to lock down.

The pricing power makes those floors believable. Micron’s Mobile and Client unit — the part most exposed to squeezed phone and PC makers — ran an 87% gross margin, up from 24% a year ago.

Why it matters

Business model: Take-or-pay volumes and price floors smooth the industry’s most violent variable. The balance sheet already reflects the boom, and Micron now holds $24.4 billion in net cash. All three agencies upgraded Micron’s credit rating to BBB+.

Competitive moat: The counterparties are the hyperscalers and NVIDIA — the same names that decide HBM allocation. Locking them in deepens an engagement already hard to displace.

Investor angle: The bear case is always about what happens when the cycle turns. A floor margin above the old peak is the most direct rebuttal Micron has ever offered. The caveat is that upfront customer deposits are not free money. They come with future supply obligations.

For decades, Micron's curse was that good times invited the bust. By getting customers to commit volume, price, and cash years out, it's betting it can keep the boom without the hangover.

🌐 The squeeze everyone else feels

Micron’s 85% gross margin is someone else’s cost line.

The same shortage minting records in Boise is rippling through the rest of tech. Apple is raising prices, and HP’s memory bill doubled. Micron CEO Sanjay Mehrotra said on the call that there’s “no line of sight” to when supply catches up with demand. He pushed the crunch past 2027, a sharp reversal from earlier guidance that had it easing by next year.

It won’t ease quickly, because adding new supply is genuinely hard. Greenfield fabs take years and run into construction lead times, scarce skilled labor, permitting, and power. Meanwhile, each new node yields fewer incremental bits, and HBM’s heavier wafer appetite eats into everything else. Data-center memory is on track to top half the industry’s total bit demand for the first time this year. Everything non-AI is the residual.

But the edge isn’t only a victim of the crunch. Agentic platforms like OpenClaw and NVIDIA’s NemoClaw are pushing more AI workloads onto devices themselves, where better economics, privacy, and latency all matter. Micron expects that shift, paired with pent-up upgrade demand, to lift the memory inside each phone and PC over time. Today’s squeezed buyers could become the next source of memory demand.

The competition is sprinting after the same wave. SK Hynix, which leads the HBM market, just filed for a ~$29 billion US listing to fund its expansion, and Jensen Huang confirmed NVIDIA will source HBM4 for its next-gen Vera Rubin platform from all three memory makers. The allocation fight among Micron, Samsung, and SK Hynix is far from settled.

The real long-run wildcard sits in China. CXMT and Yangtze Memory are scaling fast, and standard DRAM is fungible enough that OEMs can qualify different suppliers across regions, product tiers, and configurations. Chinese suppliers still trail at the high end, especially in HBM, so this is not the 2026 story. But volume is how that gap closes.

🔭 What to watch next

🪜 The margin ceiling: Management itself flagged “a meaningful moderation in the rate of price increases” behind the ~86% gross margin guide for Q4 FY26. The step-up shrank to roughly +1.4pp from the ~+6pp it guided a quarter ago. Some read that as early price softening in 2H26 as SK Hynix adds supply and PC and phone volumes keep contracting. The counter is the SCA floor, which Micron says still clears its old peak.

🔒 How far above the floor: The contract terms are now largely public. Five years, take-or-pay, ~$100 billion minimum. The open questions are concentration (four large customers carry most of it) and how far actual revenue runs above that floor.

🌐 China and policy: Watch whether US export controls on China’s semiconductor equipment access tighten or loosen, and whether CXMT lands design wins at Western OEMs for Asia-bound products.

🏗️ The cost of staying ahead CapEx will jump to ~$10 billion in Q4 (~$27 billion for full-year FY26) and will step up again in FY27, with operating expenses set to rise ~$1 billion as R&D expands. The test will be whether Micron can fund the build without surrendering the balance-sheet discipline it just earned.

Bottom Line: Micron is trying to answer the oldest objection to memory stocks: the boom always invites the bust. This time, customers are locking in supply years in advance because AI has turned memory into a strategic bottleneck. For consumers, that means higher device prices. For Micron, it means margins even NVIDIA would envy.

That's it for today.

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own AAPL, AMD, GOOG, and NVDA in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.

Very interesting insight into a part of the industry that is highly specialised and largely flew under the radar - until now. What a difference a longer-term contract can make.