📈 How to Invest in IPOs

Here's what 40 years of data says

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights

In case you missed it:

So, you want to invest in a hot IPO?

SpaceX just pulled off the largest IPO in history. The rocket maker was priced at a fixed $135 per share on June 12 and surged more than 50% in its first three days of trading, briefly touching an astounding $2.6 trillion valuation.

More are on the way. Anthropic and OpenAI filed confidentially earlier this month. The most valuable private companies on earth are racing toward public markets.

The temptation to invest is obvious.

These are the companies investors have been waiting years to own: rockets, AI models, frontier labs, category leaders. The kind of names that can make every other stock in your portfolio feel boring.

But there’s an old market joke that IPO stands for “It’s Probably Overpriced.”

The hotter the IPO, the more erratic the early trading can become.

Should you take the plunge?

Four decades of IPO history point to a boring answer: probably not yet.

Today at a glance:

📉 The IPO pop mirage

📊 What 40 years of data say

🧭 The five-rule playbook for IPOs

🚀 SpaceX, OpenAI, or Anthropic?

📉 The IPO pop mirage

The IPO pop you read about in the headlines is almost never yours.

The offering price and the opening price are two different numbers. In most hot IPOs, individual investors pay the second one.

That gap is often celebrated as a successful IPO. But it also means the company could likely have sold shares at a higher price. The first-day upside went to whoever received an allocation, not to the business or most public investors.

In traditional IPOs, banks often underprice the deal, allocated investors capture the first-day pop, and the company effectively eats the difference. Most individual investors buy in the open market after the pop.

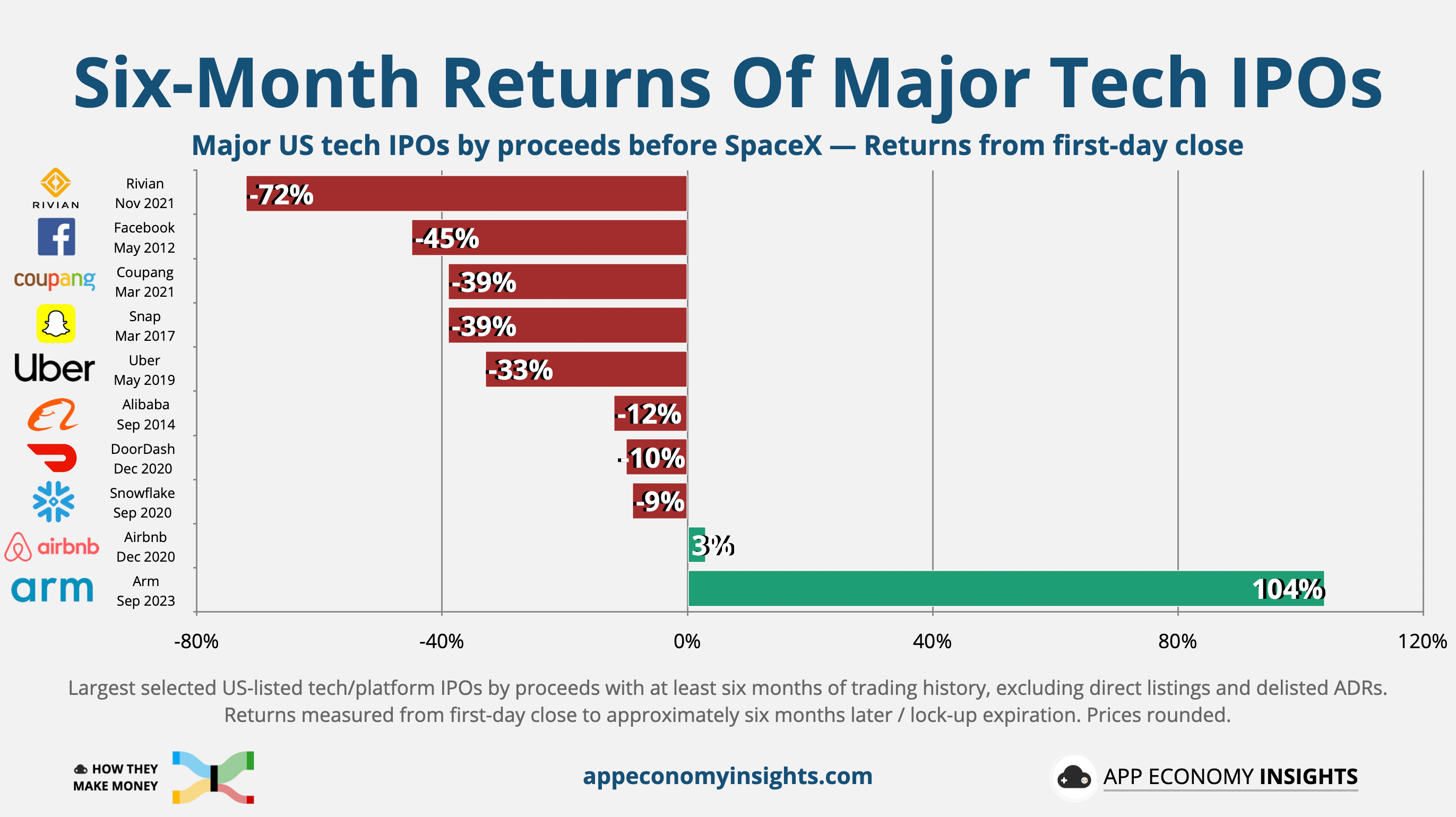

That difference can be extremely short-lived. Rivian priced its IPO at $78, closed its first day at $101, and kept climbing. A week later, it hit $172, up 70%, making it briefly the third-most-valuable automaker on the planet, ahead of Ford and GM. In retrospect, it was the peak. The stock is down more than 80% from that first-day close, near $16 today.

Cerebras priced its AI listing at $185 and closed its first day at $311, up 68%. Spectacular for whoever got the allocation. Much less helpful for anyone buying after the move, when the valuation already reflected the excitement. A month later? The stock is nearly 30% off its peak.

A monster pop is not necessarily a triumph. Sometimes it is simply a temporary mispricing, and the buyer at the open is on the wrong side of it.

SpaceX tried to make the process fairer. It skipped the usual book-building theater and reserved an unusual 30% of the deal for individual investors.

The stock rose more than 50% in its first three days of trading anyway. The valuation now reflects even more future success than the IPO price did, leaving less room for error for new investors.

Takeaway: The first-day spike is usually a transfer of wealth to people who are not you. The smaller the pop, the fairer the deal. But a fairer price and a good investment are not the same thing.

📊 What 40 years of data say

IPOs tend to underperform. And by a lot.

Why? IPO investing has three built-in disadvantages:

Limited operating history: The S-1 shows the past, not how the company behaves under public-market pressure.

Insider selling: Lock-ups often expire after ~6 months, when employees and early investors can finally sell.

Information edge: The best investors often saw the company years earlier, at much lower valuations, with better access.

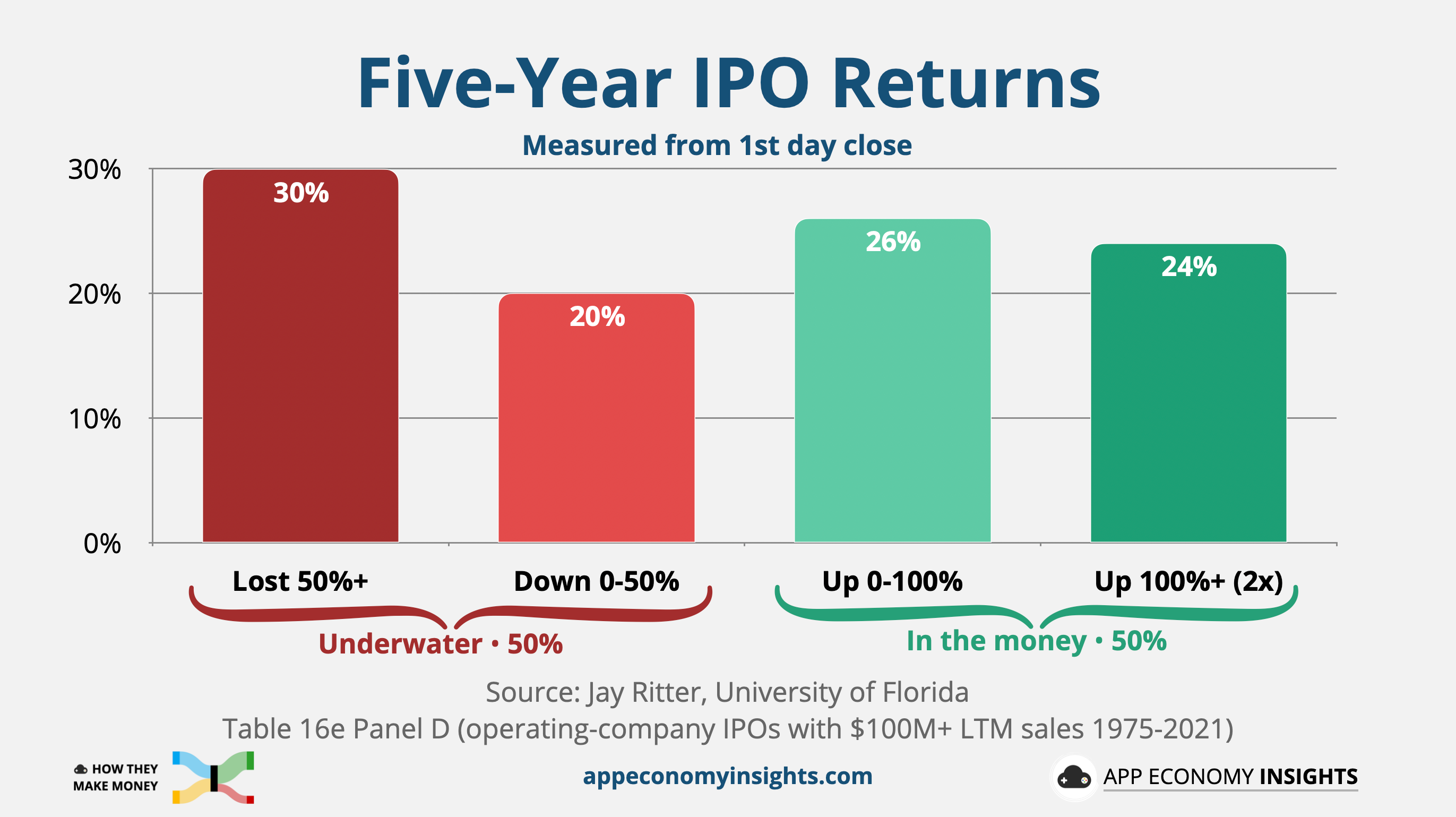

Jay Ritter has tracked new listings for decades. The University of Florida finance professor built one of the definitive IPO datasets.

Across thousands of operating-company IPOs with at least $100 million in sales, measured from the first-day close, the five-year record is sobering:

50% posted negative returns over the five years after their first-day close.

30% lost half their value or more.

Only 24% became multi-baggers, meaning they gained 100% or more.

This data excludes the smallest IPOs, those with less than $100 million in trailing sales. Including those would make the record look even worse, but also less relevant to the kind of large, category-defining companies most investors care about.

Finishing above the first-day close is not the same as beating the market. A stock that rises 20% over five years may look fine in isolation, but it still failed as an allocation if the S&P 500 did much better over the same period.

That’s why IPO researchers also look at market-adjusted returns. On that basis, the IPO record is even less forgiving. Larger IPOs do much better than tiny speculative listings, but on average, they still underperform comparable public companies after the first-day pop.

The damage clusters in a specific window: IPOs lag comparable companies most from 6 to 24 months after listing, around the time the lock-up expires and insiders are finally allowed to sell.

As the novelty fades and the selling pressure lands, expectations come back to earth, and so does the price.

If we expand to a 3-year window, several patterns show up again and again in Ritter’s 40-year data set:

Size matters: IPOs with under $100M in sales trailed the market by ~34%, while those with over $500M in sales trailed by just ~4%.

Profitability helps: Profitable issuers underperformed by ~13%, while unprofitable ones underperformed by ~31%. None of the megacaps heading for IPOs are profitable.

VC backing boosts the odds: Venture-backed names trailed by ~14% — better than the ~25% for everyone else, but still behind.

Takeaway: A new listing is usually a stock priced for the long-term growth story, at the time of maximum execution risk. Time separates the winners from the wreckage. Buying a great business can be sound, but the IPO is often the worst moment to do it.

🧭 The Five-Rule playbook for IPOs

Warren Buffett has long been skeptical of IPOs. His view is simple: IPOs come to market when sellers choose the timing, not when buyers are likely to get the best deal. He once put it bluntly:

“It isn’t worth spending five seconds thinking about IPOs.”

Of course, an IPO is merely a moment in time, not an asset class. What looks uninvestable at the IPO price can eventually become a compelling idea.

That’s why having a clear process matters.

Here are a few rules I’ve created for myself:

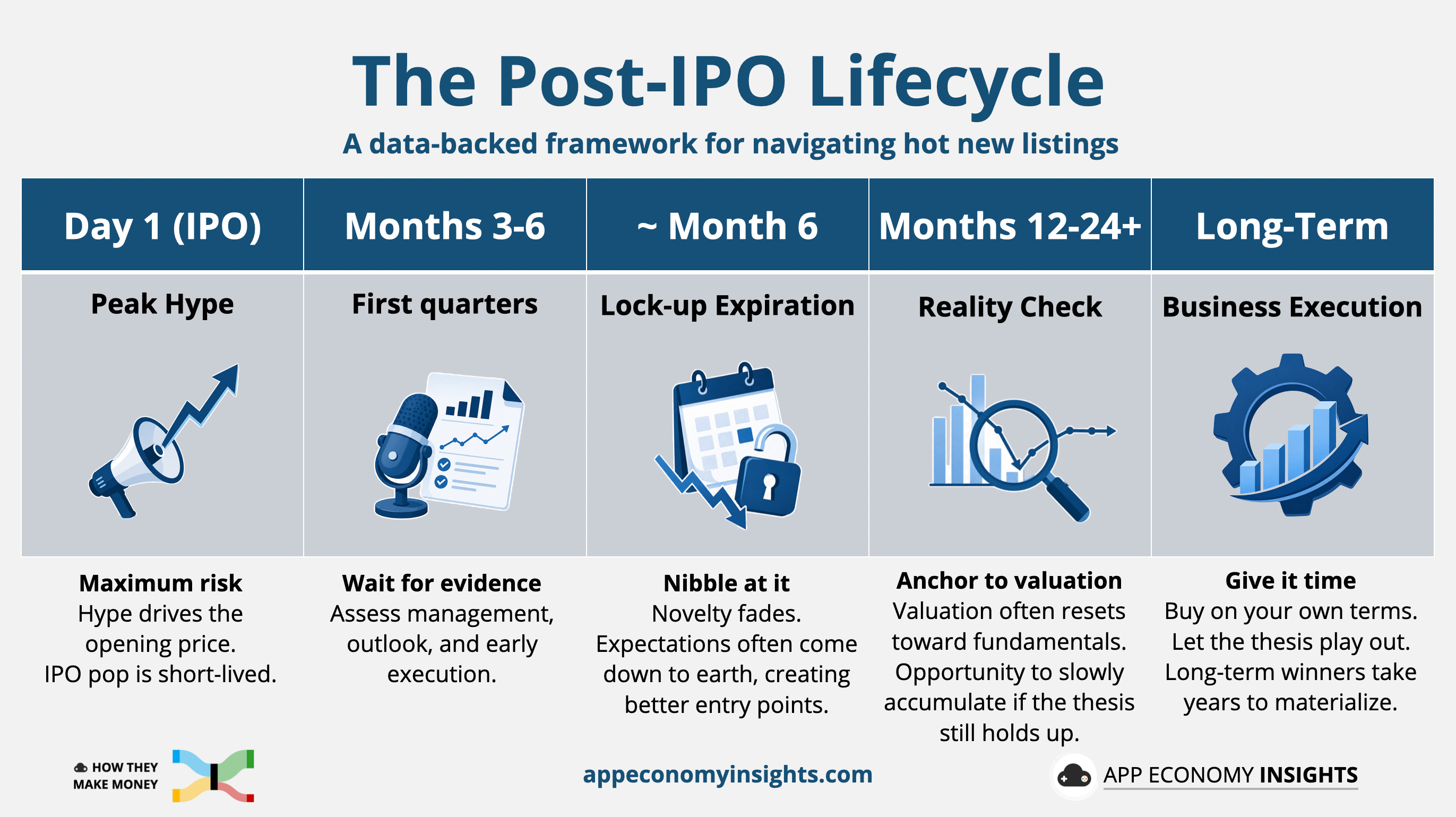

Avoid the IPO hype: The first-day pop mostly belongs to investors who received the allocation, not to open-market buyers. Rushing in on Day 1 forces you to pay a hype-driven premium at the moment of maximum risk. The rule is simple: let the initial open-market volatility pass without touching it.

Wait for the second earnings call: The S-1 is a snapshot. Public markets are the test. The first earnings call shows how management talks to investors. The second shows whether they can forecast appropriately. Are the right KPIs improving? Is growth accelerating or decelerating? Did guidance hold? Did the lock-up create selling pressure? Two quarters help draw a trendline. Anything earlier is closer to buying blind.

Nibble in year one: The first year is usually the noisiest. The stock is absorbing new shareholders, lock-up expirations, analyst coverage, guidance resets, and the first real tests of public-market expectations. A small starter position lets you follow the company closely without making the IPO price your entire cost basis. If a 50% drawdown would damage your portfolio or your sleep, the position is too big.

Anchor to valuation: Missing a 20% move is not a disaster. Buying a great company at a price that already assumes perfection can be. The question is not whether the company is exceptional. It is whether the valuation leaves room for error. Don’t sweat daily movements; instead, focus on valuation relative to fundamentals.

Give it time: Many great stocks go nowhere in their first few years as public companies. That doesn’t mean the business is broken. It means the market is still figuring out the right multiple, the right expectations, and the right shareholder base. Multi-baggers rarely require buying on day one. They require surviving the early volatility.

Takeaway: The playbook is boring on purpose. Wait for public evidence, size small, and let the lock-up cycle pass. Boring is how you beat the IPO base rates.

🚀 SpaceX, OpenAI, or Anthropic?

Neither of the new-frontier IPOs has demonstrated how the business behaves under public-market pressure. Their margins at maturity are still uncertain, and their future growth is far from guaranteed.

None of this means the companies are bad. It means the setup is hard.

These may become some of the defining franchises of the next decade. The case for owning the leaders of AI and space is real. But the case for owning them on the first day, at peak-euphoria valuations, before a single public quarter, is much weaker.

The better move is boring: put them on your watch list.

Let them report. Let the first wave of excitement pass. Let insiders sell. Let expectations move from story to numbers. Then decide whether the business is getting stronger and whether the valuation leaves room for error.

Some of these stocks may compound for a decade. The playbook is not to ignore them entirely. It’s to invest on your own terms, at a price set with a clearer head.

Bottom Line: The 2026 IPO wave is a readout of how hot the market has become, not a buy signal. SpaceX, OpenAI, and Anthropic belong on the watch list, not the impulse-buy list. The best businesses give you years to get in. The IPO only sells you the urge to rush.

Once Anthropic and OpenAI’s S-1s are available, you can expect our breakdowns and signature visuals. Stay tuned for that!

That’s it for today!

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own ABNB, BABA, CPNG, DASH, META, SNOW, and UBER in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.