❄️ Snowflake: AI Consumption Wins

While Salesforce shows the seat-based SaaS dilemma

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Software is splitting in two

AI is forcing investors to rethink which software models deserve a premium.

Two enterprise software giants reported earnings on the same evening this week.

Snowflake surged 38% after hours.

Salesforce kept sliding, extending a painful year-to-date decline.

The market is drawing a new line in software between companies that get paid more when AI works harder and companies built around seat licenses for humans who may no longer need as many seats. Consumption businesses can grow as usage rises. Traditional SaaS companies must prove AI can replace seat expansion rather than erode it.

Today at a glance:

☁️ Salesforce: AI Metrics Bury the Lede

❄️ Snowflake: The Clean Sheet Advantage

FROM OUR PARTNERS

Apple Update Sparks Huge Earning Opportunity

Most people brushed off Apple’s new Starlink integration for iPhones.

Mode Mobile saw something bigger: billions of new users suddenly within reach.

Mode’s EarnOS already reaches 490M+ users that have earned and saved over $1B, and that’s before global satellite coverage. With SpaceX eliminating “dead zones,” Mode’s earning technology can now reach billions more in unbanked and rural populations worldwide.

Their global expansion is perfectly timed, and investors like you still have a chance to invest in their pre-IPO offering at $0.50/share until the end of the day.

With their recent 32,481% revenue growth and newly reserved Nasdaq ticker, Mode is edging closer to a potential IPO. Last chance to lock in current pricing – share price changes at 5:00 PM ET.

This is a paid advertisement for Mode Mobile Regulation A+ offering. Please read the offering circular at https://invest.modemobile.com/

*Mode Mobile recently received their ticker reservation with Nasdaq ($MODE), indicating an intent to IPO in the next 24 months. An intent to IPO is no guarantee that an actual IPO will occur.

*Mode cumulative revenue includes full year revenue of businesses acquired in 2025.

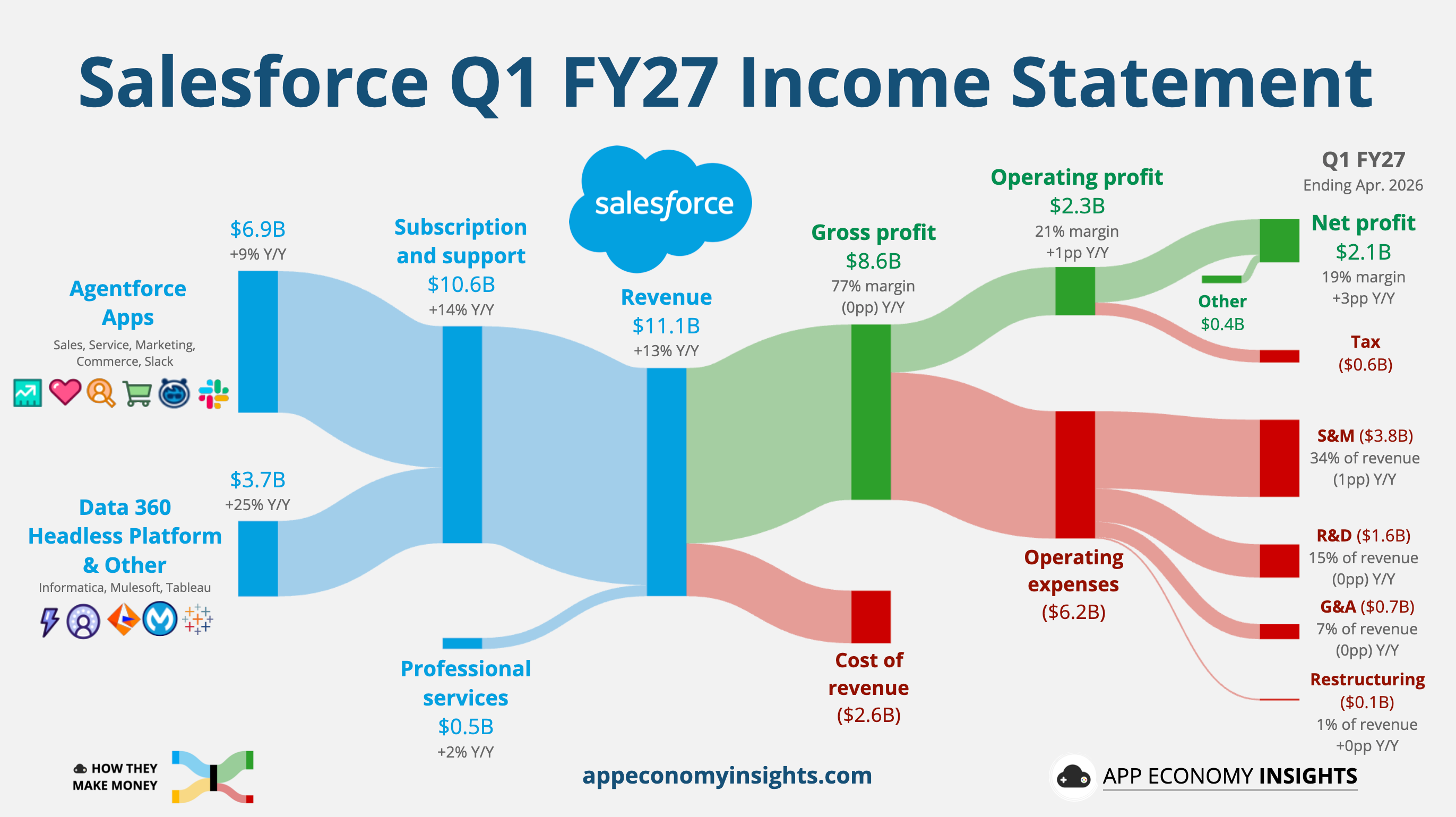

☁️ Salesforce: AI Metrics Bury the Lede

Salesforce buried its earnings announcement under an avalanche of AI metrics. Tokens processed. ‘Agentic Work Units’ delivered. Records ingested. Big numbers, but still no clear consumption revenue line.

Agentforce ARR crossed the $1 billion mark in roughly 18 months, making it one of the fastest ramps in enterprise software history. But management slightly raised the low end of full-year revenue guidance.

The market has not given the company the benefit of the doubt, with the stock already cut in half from its previous peak. That probably explains why Salesforce announced the largest accelerated share repurchase in company history, valued at $25 billion.

The number that matters to shareholders is harder to find. Strip out Informatica, acquired for $8 billion in November, and organic revenue grew roughly 9% Y/Y. Nothing to write home about.

There’s a lingering disconnect. Salesforce sells the apps that AI agents are supposed to operate on top of, and the market is no longer sure whether that makes the company indispensable or expendable.

The quarter in numbers:

Revenue +13% Y/Y (9% organic) to $11.1 billion ($70 million beat).

Operating margin reached 21% (+1pp Y/Y).

Non-GAAP EPS jumped 50% to $3.88 ($0.75 beat).

Current RPO +14% Y/Y $33.6 billion, missing the $34+ billion consensus.

FY27 guidance:

Revenue: $45.9–46.2 billion (low end raised by $100 million).

Operating and free cash flow growth: cut to 4–5%, from 9–10%, due to debt issuance for the buyback.

Q2 revenue guide: $11.27–11.35 billion, with a midpoint below the $11.36 billion consensus.

So, what to make of all this?

🤖 Agentforce is real, but still small: Agentforce ARR reached $1.2 billion, up 205% Y/Y, with net new ARR inflecting to roughly $400 million from $260 million and $100 million in the prior two quarters. At most enterprise software companies, that would be the headline. At Salesforce, it’s a footnote because the legacy base is so large.

📉 The second half remains a show-me story: Salesforce needed current (next 12 months) RPO growth above 15% to validate the pitched re-acceleration story. It came in at 13% in constant currency. Agentforce is ramping fast, but the broader growth inflection is still a second-half promise.

🛒 Marketing, Commerce, and Tableau are dragging: Management explicitly cited “ongoing weakness in Marketing and Commerce and increased softness in Tableau bookings and renewals.” These are products Salesforce paid billions to acquire. They are now the drag offsetting Agentforce momentum. The product portfolio looks more fragmented every quarter.

💸 The $25 billion buyback came with a financing cost: Salesforce used debt to accelerate its repurchases, deploying half of its $50 billion authorization at once. Diluted share count fell 10% Y/Y, but higher interest expense led management to cut operating and free cash flow growth guidance. Borrowing to buy back stock can be smart if the shares are cheap and the business re-accelerates. If growth keeps slowing, it adds leverage without solving the core growth problem.

🔍 Usage metrics dazzle but monetization is unclear: Salesforce disclosed 28.6 trillion tokens processed (+152% Q/Q), 3.8 billion Agentic Work Units (+111% Q/Q), and 52 trillion records ingested into Data 360. These are strong signs of adoption, but they still leave investors wondering how much of this usage will turn into durable revenue, and on what terms.

The New Segmentation: Two Buckets Instead of Six

This was the first quarter under Salesforce’s new disclosure framework.

The old six-cloud breakdown collapsed into two buckets:

Applications: +9% Y/Y or +7% Y/Y in constant currency.

Infrastructure & Data: +25% Y/Y or +23% Y/Y in constant currency.

Management says Agentforce is now embedded across every application, so the old cloud-level view no longer reflects how customers buy. That’s defensible. It’s also convenient.

Marketing Cloud weakness and Tableau softness used to be easier to track. Now they show up as call commentary while Informatica helps lift the broader Infrastructure & Data bucket.

Less granularity makes the portfolio look cleaner, just as investors need more visibility.

The Headless 360 Question

The most revealing exchange on the call was Goldman’s Gabriela Borges asking how Salesforce will charge for Headless 360, a new offering that lets external AI agents, including Anthropic’s Claude Code, access data stored in Salesforce apps.

Headless 360 is Salesforce’s response to the agentic threat. If agents are going to access customer data anyway, sell them the sanctioned door.

There are already signs of demand. Wedbush noted that Anthropic is one of Salesforce’s largest customers, with usage reportedly rising fivefold in Q1 due to Headless 360.

The problem is pricing. Management did not give a clear answer. President Miguel Milano said Salesforce would “work together with our customers and partners to find a fair way to monetize” the product. That answer is the whole problem in one sentence.

Usage is rising, but Salesforce has not yet explained how Headless 360 becomes a durable revenue stream. The risk is what Borges called “value abstraction”: Salesforce becomes the data store behind the agent instead of the interface where work happens.

That may still be valuable, but it requires a different pricing model. Salesforce has not fully figured it out yet.

That pricing challenge is harder because Salesforce carries so much legacy surface area. Sales Cloud, Service Cloud, Marketing Cloud, Commerce Cloud, Tableau, MuleSoft, Slack, and Informatica all come with different renewal cycles, pricing models, and competitive threats. Agentforce has to lift the entire portfolio at once. That may work over time, but the bull case needs proof faster than the product cycle can deliver it.

Takeaway: The issue is no longer whether Agentforce is real. It is whether AI makes Salesforce more essential or turns it into the data layer behind someone else’s agent. Until cRPO re-accelerates and Headless 360 has a clear pricing model, the stock might stay in the penalty box.

❄️ Snowflake: The Clean Sheet Advantage

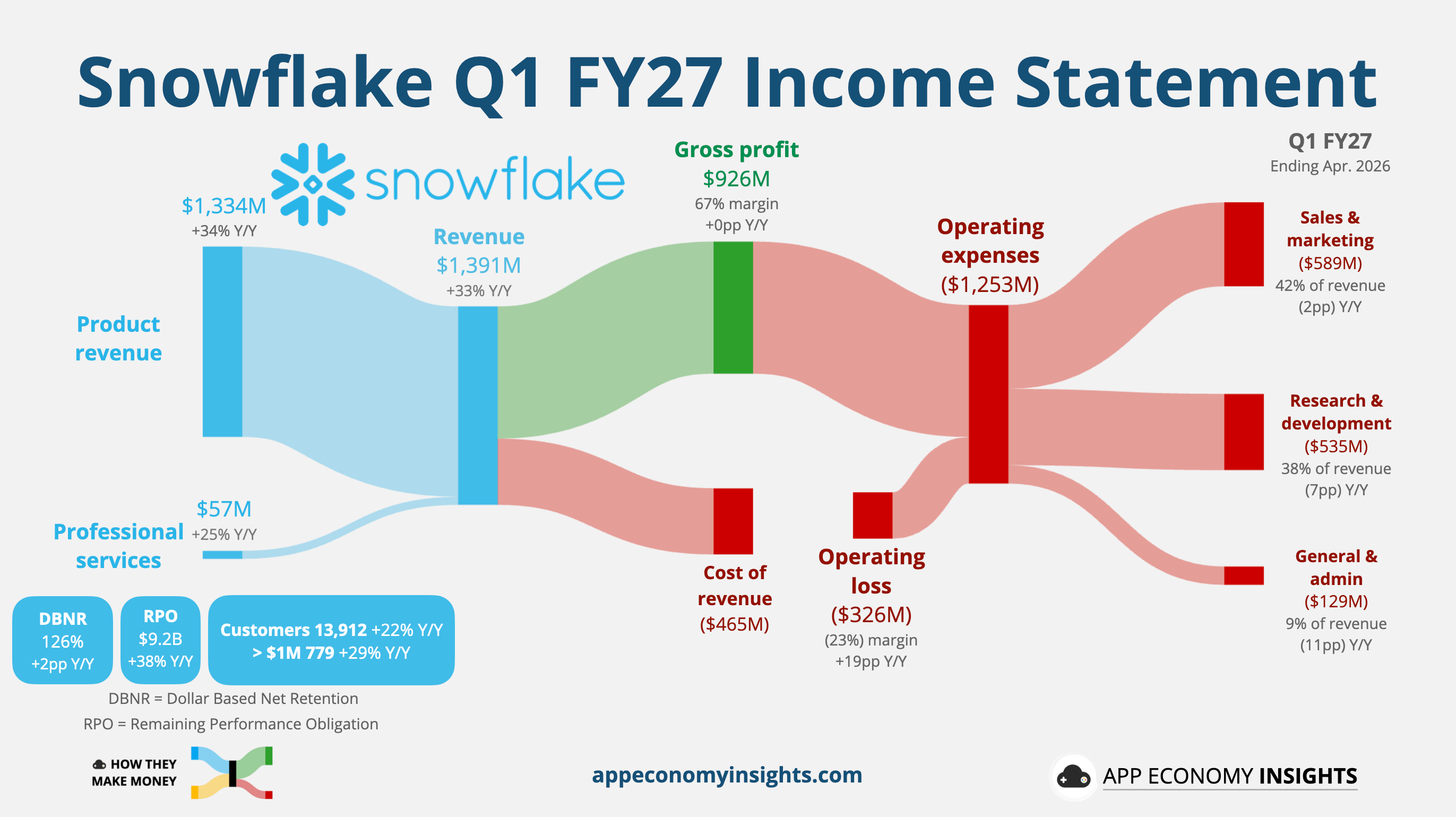

Snowflake walked into earnings as a consensus AI loser in software. It walked out with a 38% after-hours rally that erased its 20% year-to-date drawdown in a single session.

Product revenue grew +34% Y/Y to $1.33 billion, accelerating from +30% Y/Y in the prior quarter and beating management’s own projection by seven percentage points. Management raised full-year product revenue guidance to $5.84 billion (+31% Y/Y), up from $5.66 billion three months ago. Snowflake also doubled down on AWS with a five-year, $6 billion commitment.

The bear case was that agents would route around the data layer. The print suggests agents need the data layer more than humans ever did.

The quarter in numbers:

Revenue +33% Y/Y to $1.39 billion ($70 million beat).

Product revenue +34% Y/Y to $1.33 billion.

Operating loss margin -23% (+19pp Y/Y).

Non-GAAP operating margin: 12% (+3pp Y/Y).

Non-GAAP EPS: $0.39 ($0.07 beat).

Net revenue retention: 126%.

FY27 guidance:

Product revenue: +31% Y/Y $5.84 billion (up from $5.66 billion).

Non-GAAP operating margin: 13.5% (up from 12.5%).

Q2 product revenue guide: $1.415–1.42 billion (+30% Y/Y), ahead of the $1.38 billion consensus.

So, what to make of all this?

🔮 Growth outlook gets a real boost: The Q1 beat is only one part of the story. Management raised full-year guidance by $180 million and lifted the implied growth rate from 27% to 31%.

💵 The $1M+ cohort is the real signal: 46 customers crossed the $1M trailing-revenue threshold this quarter, nearly double the 26 a year ago. NRR at 126% confirms existing customers are spending more, not just new logos arriving. The consumption model is working.

🤖 AI products are now monetizing data that doesn’t even live in Snowflake: Cortex Code (CoCo) reached over 7,100 active accounts. Snowflake Intelligence accounts more than doubled quarter over quarter. Crucially, CEO Sridhar Ramaswamy noted that customers are using these tools to access data sitting inside Microsoft, Salesforce, and SAP apps (not just Snowflake’s own databases). That’s a wider moat than the original pitch.

📈 Operating leverage is finally showing up: Operating loss margin is still deep in the red but hit a new high of -23%. Non-GAAP operating margin expanded +3pp Y/Y to 12%, and full-year guidance went from 12.5% to 13.5% — despite carrying a ~150bp headwind from the Observe acquisition.

📉 RPO has a footnote: While RPO surged 38% Y/Y to $9.21 billion, it actually missed the $9.43 billion consensus. Worth tracking, but not the main story. Snowflake is a consumption business, so committed backlog matters less than actual usage.

The $6 Billion AWS Handshake

The headline number is the $6 billion AWS deal over five years.

The deal gives Snowflake heavier access to AWS Graviton chips and custom AI accelerators, helping lower compute costs as AI workloads scale. CFO Brian Robins said the agreement was structured to support AI growth without pressuring gross margins.

That matters because Snowflake is guiding to a 75% product gross margin while AI usage expands. In other words, the company is trying to turn AI demand into consumption growth without sacrificing the economics investors care about.

AWS gets more AI workloads. Snowflake gets cheaper compute, better margins, and a stronger pitch to enterprise customers already building on AWS.

The Natoma Acquisition

Easy to miss next to the AWS number, Snowflake announced the acquisition of Natoma, an enterprise-grade implementation of the Model Context Protocol (MCP).

Snowflake wants to govern not only what AI agents can read, but what they can do.

MCP is the wiring that lets AI agents securely take actions on behalf of an enterprise. That matters because agents that act consume far more compute than agents that simply retrieve answers.

Snowflake spent a decade becoming the governed home for enterprise data. Natoma extends that governance into the agentic workflow.

Databricks, Microsoft Fabric, and Google BigQuery all want the same role. Snowflake’s bet is that enterprise security and identity, not just model quality, will decide who controls the agentic data layer.

Takeaway: Snowflake’s quarter flipped the AI narrative. Agents are not routing around the data layer. They appear to be increasing the need for governed data, secure workflows, and scalable compute. That is exactly where Snowflake wants to sit. The 35%+ rally reflects how washed-out sentiment had become, but the bigger lesson is structural. For the right software model, AI can turn rising usage into rising revenue.

That’s it for today!

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own CRM and SNOW in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.