🔎 Why Google is Selling $85B of Itself

Cash, debt, or equity: how Big Tech pays for AI

Welcome to the Premium edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Alphabet sold $85 billion of stock in two days

That’s more than what the largest IPO in history will raise.

SpaceX is about to price the largest initial public offering ever at $75 billion, valuing the company at ~$1.8 trillion. But Alphabet, the parent company of Google, quietly topped that last week by selling new shares — upsizing a planned $80 billion raise to $85 billion after demand poured in. Berkshire Hathaway anchored it with a $10 billion investment, buying shares at a 6–8% discount.

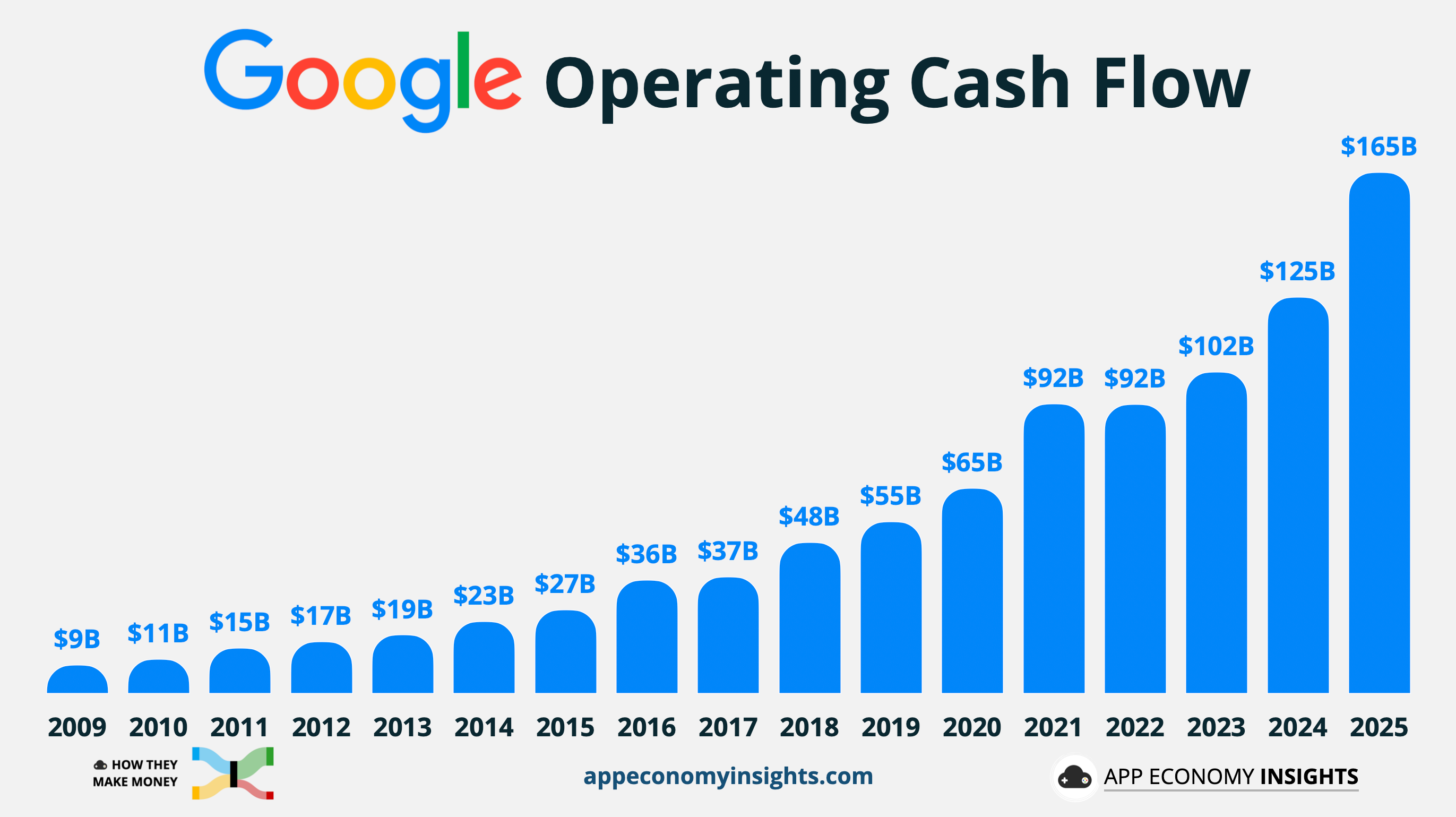

Here’s the paradox. Alphabet sits on well over $120 billion in cash and short-term investments on its balance sheet, just generated $165 billion in operating cash flow last year, and can borrow at rates few companies on earth can match. Firms in that position almost never sell equity. Instead, they use their cash flow to buy back stock. Diluting your own shareholders is the most expensive money there is, a slice of every future dollar of profit, forever.

So why do it? Because the AI buildout has grown so large it requires every available tool. Alphabet expects to spend $190 billion in 2026 alone, and that figure could increase by year-end.

Every company racing to build compute now stands in front of three doors:

Pay with the cash you already generate.

Borrow it (issue debt).

Sell a piece of the company (issue equity).

Each door sends a different signal about how confident you are and how much risk you are willing to take (more on this in a minute).

Today, we are looking at the three ways Big Tech is currently funding the trillion-dollar AI buildout. We’ll review which ones are good or bad for investors and what it says about where we are in this market cycle.

💵 Self-funding

🏦 Debt issuance

📉 Selling more stock

1. 💵 Self-funding

The cleanest way to fund a data center is to pay for it with money the business already makes. No interest, no dilution, no banker fees. For most of this cycle, that’s exactly what Big Tech did.

If you need a reminder, free cash flow (FCF) is the cash generated from the business, less capital expenditures (funds to buy, upgrade, or maintain physical assets). As long as FCF is positive, you are effectively self-funding your business ventures.

Free Cash Flow = [Cash from Operations – Capital Expenditures]

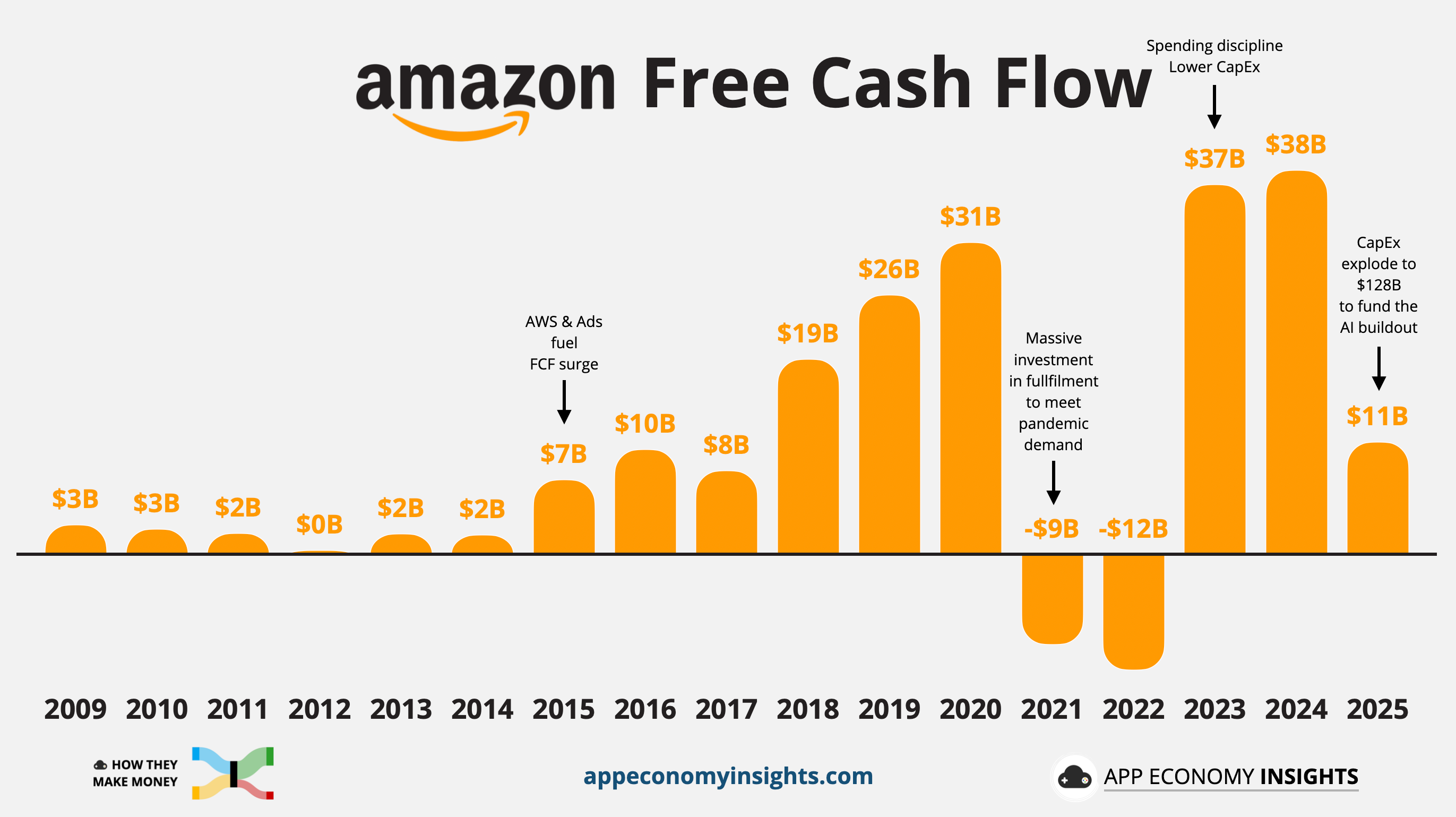

Amazon is the textbook case for how far that model stretches. The company is on track for roughly $200 billion in capital expenditures in 2026, up from a trailing-twelve-month figure of $147 billion (+67% Y/Y).

Meanwhile, trailing-12-month operating cash flow grew to $149 billion (+30% Y/Y) at the end of March. It’s a staggering number that, a few years ago, would have funded the whole thing with room to spare. It no longer does.

Amazon is now spending essentially every dollar it generates. It was already the case in 2021 and 2022, when the company invested in fulfillment to meet pandemic-driven demand. As a result, FCF turned slightly negative in 2021 and 2022. FCF recovered to a record $38 billion in 2024 before the AI buildout cut it to $11 billion in 2025

At the end of Q1 2026, trailing FCF worsened to just ~$1 billion.

“The faster AWS grows, the more short-term CapEx we’ll spend.”

That was CEO Andy Jassy on the Q1 call, and it captures the squeeze. AWS reaccelerated to +28% Y/Y, its fastest in nearly four years, but Amazon has to lay out cash for land, power, chips, and servers 6 to 24 months before it can bill a customer. Growth and free cash flow are pulling in opposite directions.

Self-funding is a position of strength: you don’t need anyone’s permission to build. The catch is that it caps your spend at what the business produces today. The AI bill is now testing that ceiling everywhere. Microsoft, Meta, and Alphabet still fund most of their CapEx from existing operations. The open question is what happens when one great business can no longer feed an even hungrier one.

Takeaway: Free cash flow is the cheapest capital and the proudest signal — it says the core business can pay its own way. But when CapEx consumes more than 100% of operating cash flow, the wallet is empty, and the next dollar has to come from somewhere else.