🎨 Adobe: AI Scare Trade

Live Nation keeps Ticketmaster and Meta launches in-house chips

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights

In case you missed it:

Today at a glance:

🎨 Adobe: AI Scare Trade

🎟️ Live Nation: Keeping Ticketmaster

🤖 Meta: Going Deeper Into Custom AI Chips

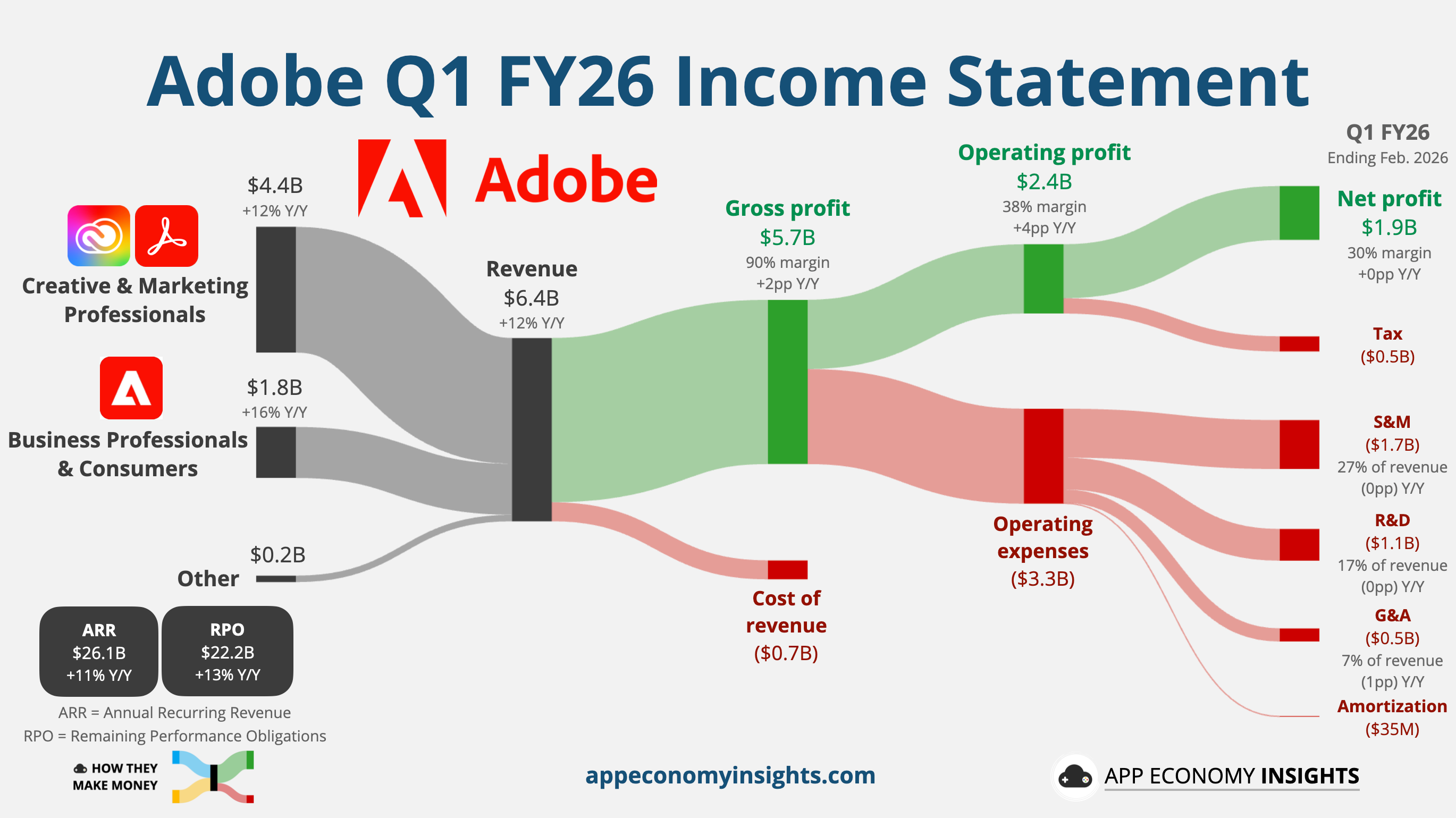

🎨 Adobe: AI Scare Trade

Adobe’s Q1 2026 results came with the end of an era.

The architect of Adobe’s cloud transformation, CEO Shantanu Narayen plans to step down after 18 years. Despite beating estimates across the board, shares fell about 7% as investors weighed leadership uncertainty and persistent fears around AI disruption.

Adobe’s AI strategy is starting to show up in the numbers:

Double beat: Revenue grew 12% Y/Y to $6.4 billion ($120 million beat). Non-GAAP EPS reached $6.06, well above the $5.87 expected.

Strong user growth: Monthly active users reached 850 million (+17% Y/Y). Creative Premium MAU surged 50%, fueled by the freemium funnel for Express and Firefly.

Cash powerhouse: Adobe generated nearly $3 billion in operating cash flow and maintained a sky-high non-GAAP operating margin of 47%.

Next billion-dollar business: ARR from AI-first applications such as Firefly for Enterprise more than tripled Y/Y. Firefly ARR has already crossed $250 million, and Narayen called it Adobe’s next billion-dollar pillar. Still, it remains a tiny portion of total ARR, which grew 11% to $26.1 billion.

The CEO transition follows a similar move at Workday, where the CEO recently stepped aside for a founder-led AI pivot. Narayen will remain as Chair of the Board and CEO until a successor is found. The timing of the exit is curious, given that the board recently approved a new long-term performance share program for Narayen that doesn't vest until early 2029.

This transition comes at a delicate time for the company. AI is a growth engine, but it is also a double-edged sword. Adobe said its traditional stock business, which generates $450 million a year, is declining faster than expected as users shift to generative AI alternatives. This shift captures the core SaaSpocalypse anxiety. The company is successfully selling AI tools, but those tools are also cannibalizing its own high-margin legacy segments.

Adobe is betting its 850 million user base will eventually graduate into paid tiers as they hit AI paywalls for advanced generative features. Q2 guidance was ahead of Wall Street estimates, targeting revenue of $6.43-$6.48 billion, but it still implies a slowdown (+9-10% Y/Y). For a company trying to prove AI can bring reacceleration, single-digit growth is nothing to write home about.

The market remains deeply skeptical, with shares down nearly 30% so far in 2026. At less than 12x forward earnings, Adobe is no longer priced like a premium software franchise. The challenge for the next CEO is straightforward: prove Adobe can turn its AI funnel into durable monetization before rivals and AI-native tools reshape the category around it.

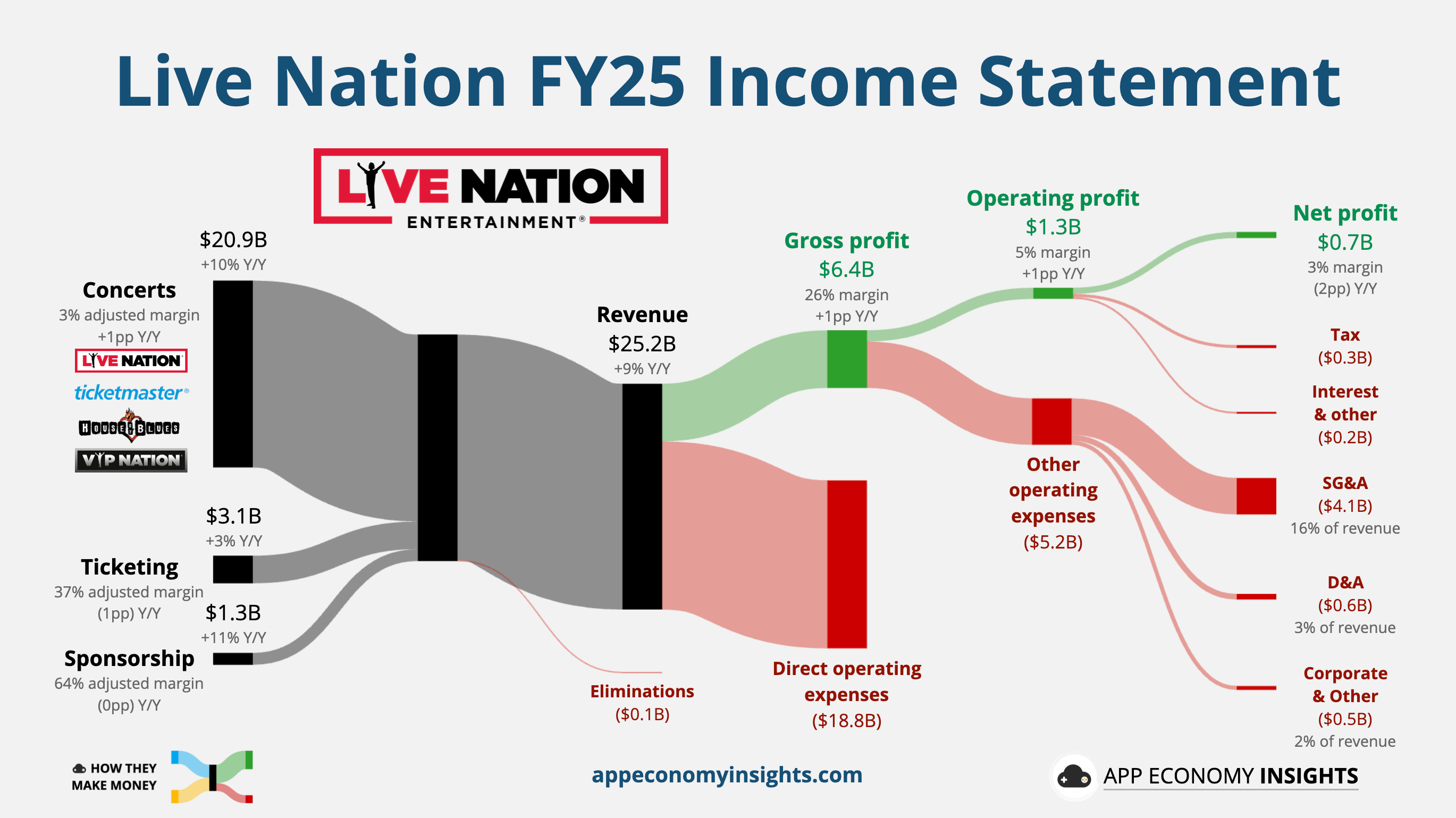

🎟️ Live Nation: Keeping Ticketmaster

The long-running antitrust battle over Live Nation and Ticketmaster took a surprising turn this week.

The US Department of Justice (DOJ) reached a settlement with Live Nation, allowing the company to keep Ticketmaster and avoid the structural breakup regulators had initially pursued. Importantly, the deal does not include a federal financial penalty.

Instead, the agreement focuses on operational concessions designed to increase competition:

Ticketmaster must allow venues to sell up to 50% of tickets through rival marketplaces.

Service fees at Live Nation-controlled venues will be capped at 15%.

The company must terminate exclusive ticketing agreements at 13 amphitheaters and offer both exclusive and non-exclusive ticketing proposals going forward.

The existing DOJ consent decree will be extended for eight years with stronger oversight provisions.

One detail jumps out in how Live Nation makes money. Despite dominating the live events ecosystem, Live Nation’s profits remain surprisingly thin. The company generated $25.2 billion in revenue but only $0.7 billion in net income in FY25, a net margin of just 3%.

That’s because the bulk of the business is concert promotion, where most ticket revenue flows to artists and production costs. Critics argue the company’s market power lies less in massive margins and more in control of the ecosystem (promotion, venues, and ticketing all under one roof).

The biggest headline today is that Ticketmaster stays inside the empire.

Breaking up Live Nation’s ticketing and promotion businesses had been the core structural risk hanging over the stock since the lawsuit was filed in 2024.

However, the legal fight is far from over.

More than two dozen US states rejected the settlement and plan to continue pursuing the case in court, arguing that the agreement fails to address what they view as a monopoly over live events.

Live Nation has set aside $280 million to cover potential damages tied to those state claims.

For now, the outcome removes the most extreme scenario of a forced divestiture of Ticketmaster. But it leaves a lingering legal overhang as the state-led case moves forward.

🤖 Meta: Going Deeper Into Custom AI Chips

Meta unveiled a roadmap for four new in-house AI chips this week: MTIA 300, 400, 450, and 500. The chips will roll out through 2027 and are designed to support everything from content ranking and recommendations to gen AI inference.

The bigger point is inference. Meta is increasingly designing chips not just for training models, but for running AI workloads efficiently at scale. This matters because AI is becoming a much larger cost center for Meta.

It also hints at a narrower focus. Earlier this month, reports said Meta had scrapped some of its most ambitious training-chip efforts, including Iris and Olympus, after design struggles. That makes this roadmap look less like a full challenge to NVIDIA and more like a focused attempt to optimize the workloads Meta knows best.

Meta is not doing this alone. The MTIA family is being co-developed with Broadcom, which gives Meta access to proven silicon expertise while accelerating its roadmap. Meta wants to hit a blistering 6-month release cadence to ensure its hardware doesn’t become obsolete before it even reaches the data center.

Despite this in-house push, Meta is still spending billions with NVIDIA and AMD. In fact, Meta just signed a massive $100 billion deal with AMD for 6 gigawatts of MI450 GPUs. Ultimately, the goal is not to replace third-party chips overnight, but to diversify suppliers, lower costs, and better optimize chips for its own workloads.

Every recommendation, every generated image, every chatbot response has to run somewhere. If Meta can lower inference costs across Facebook, Instagram, WhatsApp, and its ad stack, the savings add up fast.

There is still execution risk. Custom chips are expensive to design, take years to bring into production, and only really pay off at huge scale. Meta is betting that better bandwidth density can lower the cost of inference at scale.

Inference is often constrained less by raw compute than by how quickly data can move between memory and processors. By designing for this specific constraint, Meta claims that the MTIA 500 will deliver 27.6 TB/s of bandwidth, potentially outperforming even NVIDIA’s specialized Rubin chips for Meta’s internal workloads.

The biggest AI spenders increasingly want more control over their own infrastructure economics. After spending over $70 billion in 2025, Meta is guiding to $115–$135 billion in capital expenditures in 2026. It’s the third-largest infrastructure budget, only behind Amazon and Google.

Meta’s AI bill is getting so large that even small efficiency gains start to matter. Custom chips are becoming one of the clearest ways to protect margins as inference scales.

That’s it for today!

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own AMZN, AMD, AVGO, GOOG, LYV, META, and NVDA in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.

Interesting