🤖 NVIDIA: Great Wall of Worry

AI momentum continues despite China uncertainty

Welcome to the Free edition of How They Make Money.

Over 200,000 subscribers turn to us for business and investment insights.

🔜 Coming up:

PRO coverage with Alibaba, CrowdStrike…

Premium monthly report with over 100 companies visualized.

In case you missed it:

The AI race is on, and NVIDIA is supplying the shovels.

It's an old Wall Street adage that bull markets are forced to 'climb a wall of worry,' constantly overcoming risks that seem daunting. For NVIDIA, that obstacle has become its own Great Wall—the immense and ever-shifting uncertainty surrounding its future in China.

The latest earnings published on Wednesday delivered more of the same story, with AI momentum so strong that it overshadowed the latest concerns.

CEO Jensen Huang connected the dots for us:

“Over the next 5 years, we're going to scale [...] into effectively a $3 to $4 trillion AI infrastructure opportunity. The last couple of years, you have seen that CapEx has grown in just the top four CSPs has doubled to about $600 billion. So we're in the beginning of this build-out.”

As the primary beneficiary of this spending, NVIDIA is positioned to capture a significant share of this expanding pie. With demand still far outstripping supply, the growth story is alive and well.

Perhaps the most bullish case for NVIDIA is the rising role of “reasoning” models and the race for everyone to stay at the leading edge. No matter who takes the lead, NVIDIA gets paid all the same.

So what did we learn from the world's largest company this quarter?

Today at a glance:

NVIDIA’s Q2 FY26.

Great wall of worry.

Key quotes from the call.

What to watch moving forward.

1. NVIDIA Q2 FY26

NVIDIA’s fiscal year ends in January, so the July quarter was Q2 FY26.

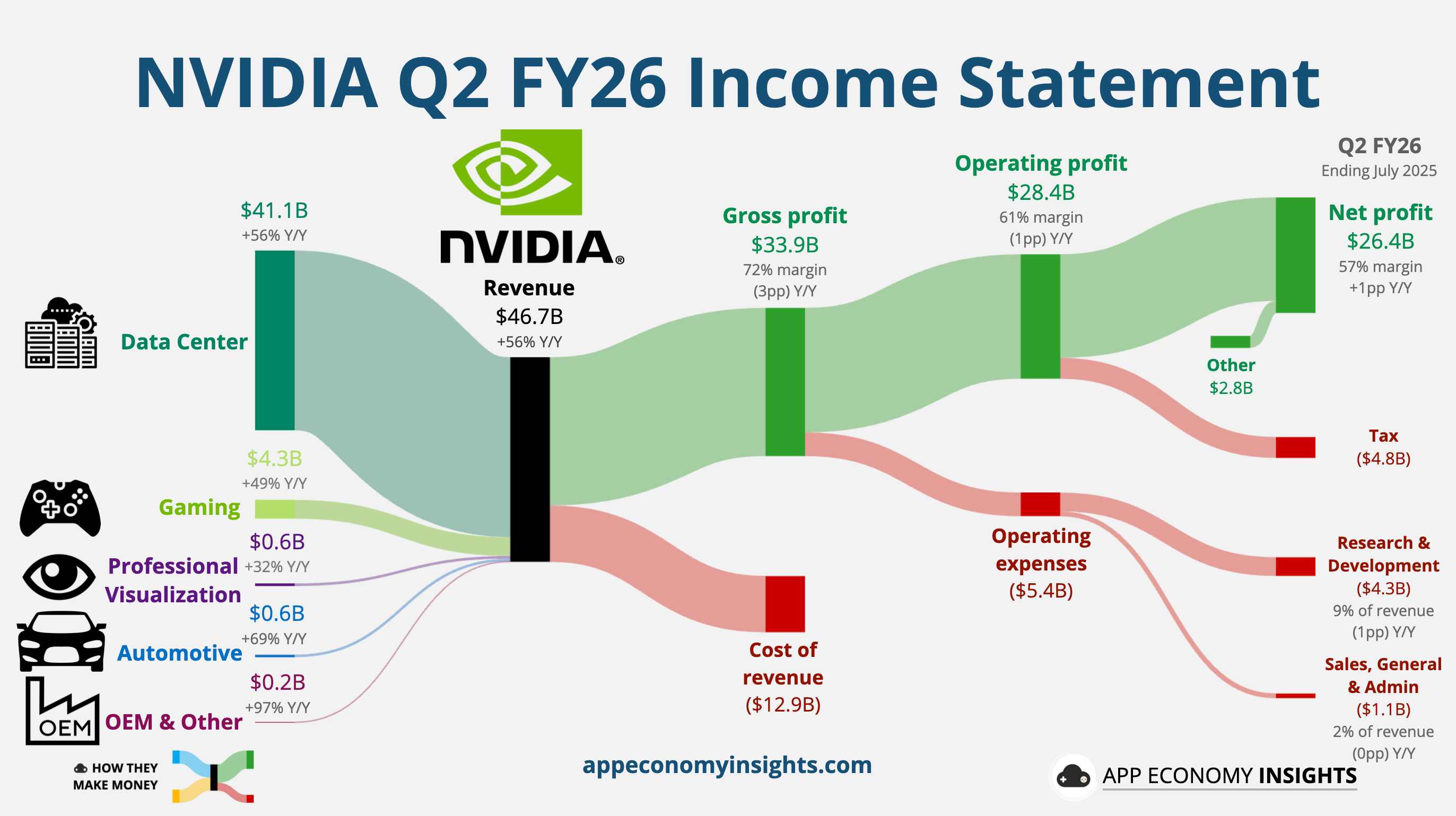

Income statement:

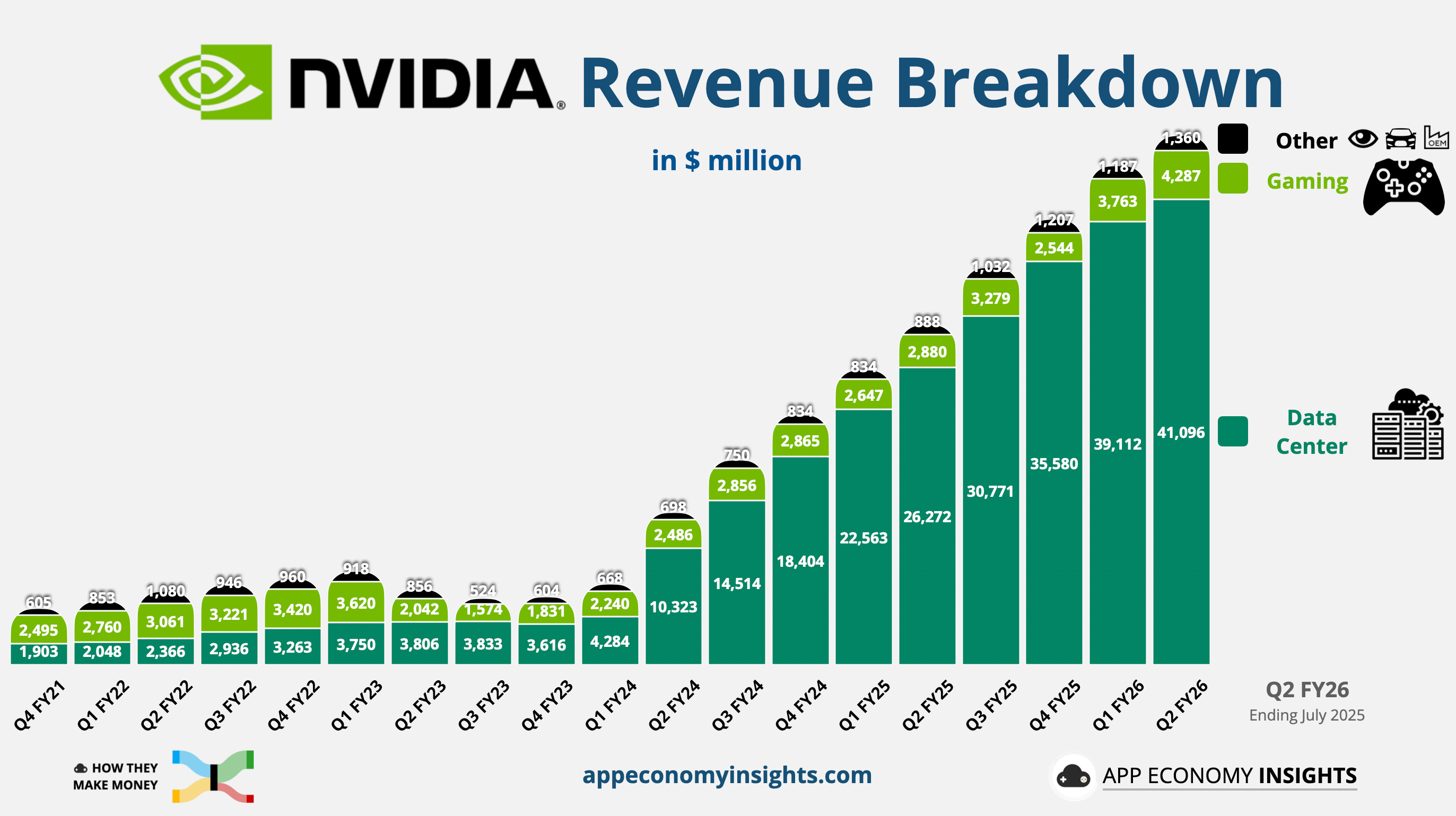

Revenue jumped +6% Q/Q and 56% Y/Y to $46.7 billion ($0.6 billion beat).

⚙️ Data Center +5% Q/Q and +56% Y/Y to $41.1 billion.

🎮 Gaming +14% Q/Q and +49% Y/Y to $4.3 billion.

👁️ Professional Viz +18% Q/Q and +32% Y/Y to $0.6 billion.

🚘 Automotive +3% Q/Q and +69% Y/Y to $0.6 billion.

🏭 OEM & Other +56% Q/Q and +97% Y/Y to $0.2 billion.

Gross margin was 72% (-3pp Y/Y).

Operating margin was 61% (-1pp Y/Y).

Non-GAAP operating margin was 65% (-2pp Y/Y).

Non-GAAP EPS $1.05 ($0.04 beat).

Cash flow:

Operating cash flow was $15.3 billion (33% margin).

Free cash flow was $13.5 billion (29% margin).

Balance sheet:

Cash and cash equivalents: $56.8 billion.

Debt: $8.5 billion.

Q3 FY26 Guidance:

Revenue +16% Q/Q and +54% Y/Y to $54.0 billion ($1.2 billion beat).

Gross margin 73% (+1pp Q/Q).

So, what to make of all this?

The global AI boom easily eclipses the impact of lost sales in China.

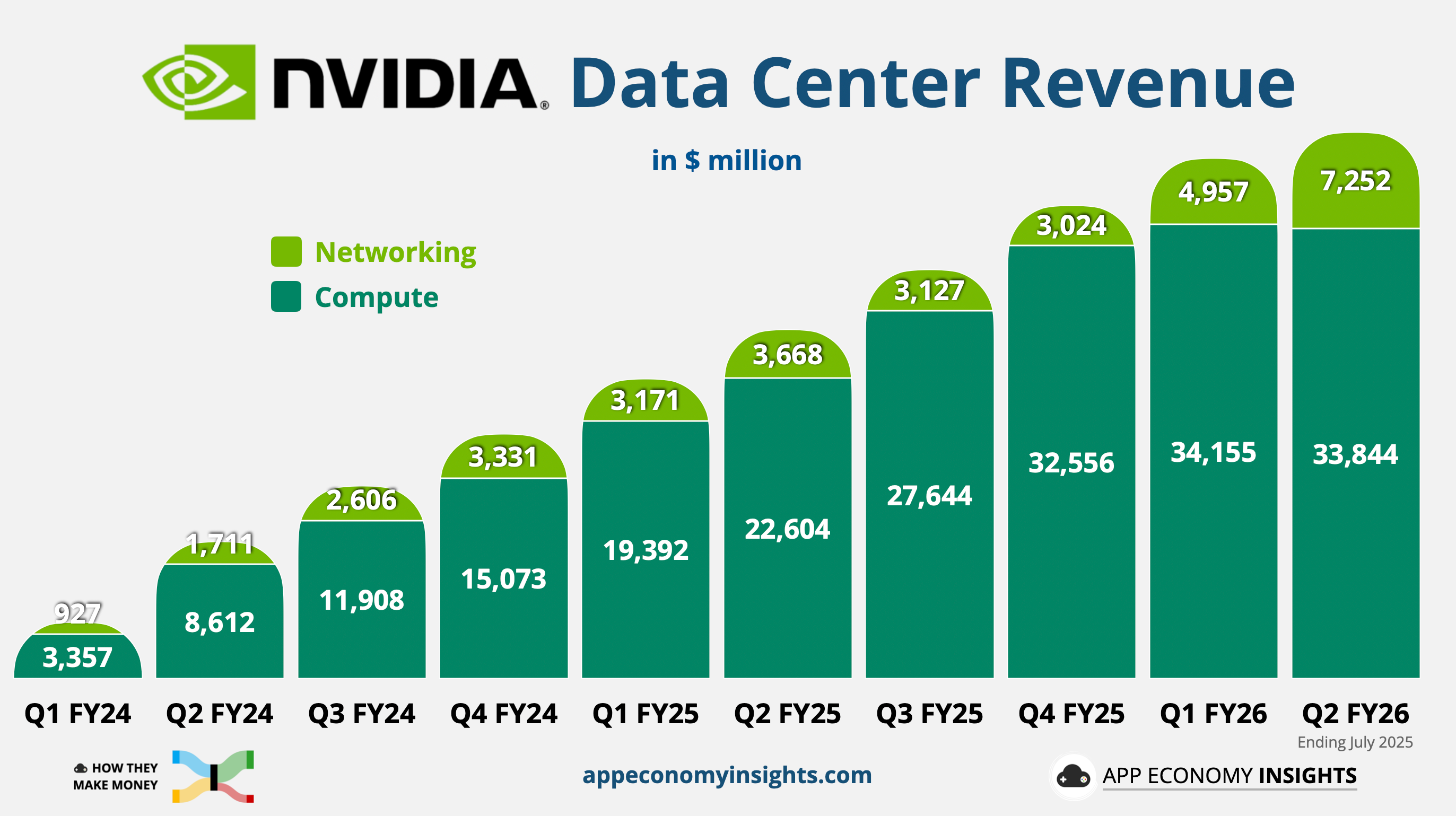

⚙️ Data Center represented 88% of total revenue. Blackwell revenue grew 17% Q/Q and is now recognized across all customer categories, led by hyperscalers. The upgrade cycle is broadening beyond early adopters. The segment saw a softer 5% sequential growth and slightly missed expectations, but we have to look closer:

⚡ Compute revenue ticked down 1% Q/Q to $33.8 billion because of the H20 (the chips designed to ship to China to comply with US export rules) sales dropping from $4.0 billion in Q1 to zero in Q2. Results included a one-time tailwind of $180 million release tied to roughly $650 million of H20 inventory sold to an unrestricted customer outside China. It lifted gross margin by ~40bps and EPS by $0.01.

🔌 Networking revenue jumped 46% Q/Q to $7.3 billion as NVLink fabrics for GB200/GB300, XDR InfiniBand, and fast Ethernet-for-AI deployments scaled across cloud and consumer internet customers.

🎮 Gaming rebounded 14% sequentially, reaching $4.3 billion, boosted by the successful launch and rapid adoption of the Blackwell-powered GeForce RTX 5060 GPUs.

👁️ Professional visualization saw an 18% sequential growth to $601 million, driven by the adoption of Blackwell architecture in notebook workstations, catering to AI-powered workflows, real-time rendering, and complex simulations.

🚘 Automotive reported a 3% sequential growth to $586 million, reflecting the increasing adoption of NVIDIA’s autonomous platforms and digital cockpit solutions.

📉 Margins recover: Gross margins saw a significant recovery from Q1, which was impacted by an inventory write-down. The company's guidance for the third quarter points to continued margin expansion.

🔮 Outlook still solid: Q3 outlook assumes zero H20 to China again. Yet, revenue is expected to surge another 16% sequentially, a remarkable acceleration. Management also announced a $60 billion buyback.

Big picture: The standout lever is networking as AI fabrics scale, while the modest compute dip is H20/China-driven noise, not demand erosion. With Blackwell ramping across cohorts and strong guidance set without China, the thesis remains intact.

2. 🇨🇳 Great Wall of Worry

The US government’s April ban on H20 chip exports to China blocked $2.5 billion in revenue for Q1, and another $8 billion missed opportunity for Q2.

The tension boiled over after a US official, Howard Lutnick, explained the strategy behind allowing sales of less-advanced chips:

"We don’t sell them our best stuff, not our second-best stuff, not even our third-best. […] You want to sell the Chinese enough that their developers get addicted to the American technology stack."

The remark was undiplomatic and "insulting" to some senior officials in Beijing, and it gave Chinese regulators the perfect justification to push local firms toward domestic hardware, putting a business that recently made up 13% of NVIDIA's revenue in a precarious position.

For Wall Street, the key question is how much revenue to expect from China—if any. Analysts are grappling with the double-whammy of Beijing's cold shoulder and a potential new US deal that forces NVIDIA to hand over 15% of its China revenue as a "tax" for export licenses, directly squeezing margins. While NVIDIA is developing a new chip for China, the B30A, its future hinges on unpredictable regulations on both sides of the Pacific.

NVIDIA's own guidance assumes the worst. From the earnings call:

“We have not included H20 in our Q3 outlook [...] If geopolitical issues reside, we should ship $2-to-$5 billion in H20 revenue in Q3. [...] We continue to advocate for the US government to approve Blackwell for China.”

This is the multi-billion-dollar wildcard. The Q3 guide of $54 billion is already a blowout, but any good news would boost Q3 numbers.

While the immediate focus is on sales numbers, the bigger story is China's race to build a completely independent AI stack. Local AI startup DeepSeek announced its latest model is optimized for homegrown AI chips. The country is actively looking for ways to leave NVIDIA on the outside looking in. If they succeed, NVIDIA could be locked out of a market Jensen Huang expects to be worth $50 billion.

NVIDIA's moat is a fortress built on four walls: CUDA software, its ubiquity across clouds, its unmatched systems and networking integration, and its superior performance-per-watt in a power-limited world.

Maintaining this moat in China requires selling chips in the country to begin with.

3. Key quotes from the earnings call

CFO Colette Kress:

On Data Center growth:

“Data center revenue also grew sequentially despite the $4 billion decline in H20 revenue. [...] NVIDIA’s Blackwell platform reached record levels, growing sequentially by 17%. [...] This growth is fueled by capital expenditures from the cloud to enterprises, which are on track to invest $600 billion in data center infrastructure and compute this calendar year alone, nearly doubling in two years.”

The Blackwell ramp and networking scale-out managed to more than offset the China headwind, as the infrastructure race rages on.

On Networking:

“Networking delivered record revenue of $7.3 billion, a 46% sequential and 98% year on year increase with strong demand across Spectrum X Ethernet, InfiniBand, and NVLink. Our Spectrum X enhanced Ethernet solutions [...] delivered double digit sequential and year over year growth with annualized revenue exceeding $10 billion”

This massive growth showcases networking’s crucial role in AI factories. In short, AI fabrics (InfiniBand, NVLink, and Ethernet-for-AI) are becoming a second growth engine.

On Sovereign AI:

“Sovereign AI is on the rise as the nation's ability to develop its own AI using domestic infrastructure data and talent presents a significant opportunity for NVIDIA. [...] We are on track to achieve over $20 billion in sovereign AI revenue this year, more than double that of last year.”

From a talking point to a $20 billion business in a short time. This is proof that countries worldwide are treating AI infrastructure as critical national security, and NVIDIA is the primary arms dealer.

CEO Jensen Huang:

On "Reasoning" as the new growth engine:

The shift from simple chatbots to complex "agentic AI" is a fundamental driver.

“Chatbots used to be one shot, you give it a prompt and it would generate the answer. Now the AI does research. It thinks and does a plan, and it might use tools. It's called long thinking [...] The amount of computation necessary for one shot versus reasoning agentic AI models could be 100x, 1000x, and potentially even more.”

More than adoption by more users, AI models will do exponentially more work per query, which is a critical justification for the world needing trillions of dollars in new infrastructure.

On Full-Stack moat vs. ASICs:

When asked about the competitive threat from custom ASICs, Jensen Huang reframed the argument around the most critical bottleneck in AI today: power.

“We're in every cloud for a good reason. Not only are we the most energy efficient, our perf per watt is the best of any computing platform. And in a world of power-limited data centers, perf per watt drives directly to revenues.”

Huang’s defense is simple. NVIDIA wins here because its full-stack platform—where hardware and CUDA software are co-designed—delivers the best efficiency, making it the most profitable choice for customers. While rivals focus on building a single chip, NVIDIA builds the entire factory. That’s the real moat.

On Rubin:

“We're on an annual cycle [...] because we can do so to accelerate the cost reduction and maximize the revenue generation for our customers. [...] Our next platform, Rubin, is already in fab.”

An annual cadence makes it nearly impossible for competitors to catch up.

4. What to watch moving forward

Still a popular pick in 2025

We recently reviewed Wall Street’s top picks in the latest 13F filings for Q2 2025. High-profile funds like Altimeter, Sands, Appaloosa, Tiger Global, Baillie Gifford, and Whale Rock increased their NVDA allocation, which is not entirely surprising considering the stock hit a new 52-week low during the quarter.

The trend? NVDA remains one of the most widely held stocks, and funds are still adding to their positions on weakness. Paradoxically, now that NVDA makes up nearly 8% of the S&P 500, most top money managers are still underexposed relative to the index, forcing them to play catch-up.

At 41x forward earnings, NVIDIA trades at a premium to Microsoft and Apple. But with EPS surging 61% Y/Y in Q2, you can argue NVIDIA is still… undervalued? With $26 billion in net income this quarter, the profits are very real, even with a challenged China business.

NVIDIA's growth is supply-constrained. While this means revenue growth will remain limited by the company's ability to catch up with demand, it also makes analyzing quarter-to-quarter trends misleading

If you’re a regular reader, you already know the key risks:

Cycles boom and bust: Like any technology bubble in history, there will be a point where the skyrocketing demand will plateau or decline. It’s a matter of when, not if. The ebb and flow of market cycles can lead to extreme volatility.

Geopolitics are regulations: NVIDIA is highly reliant on TSMC, which could lead to a supply chain disruption. New tariffs are always around the corner, and China appears determined to build without NVIDIA’s chips. Oh, and the US government now owns 10% of Intel?

Customer concentration and competition: Hyperscalers still buy, while simultaneously building their own AI chips. NVIDIA’s 67% net profit margin is someone else’s opportunity.

Robots next?

To close the call, Jensen painted a picture of the next wave: AI moving from digital services to the physical world.

“The age of physical AI has arrived, unlocking entirely new industries in robotics, industrial automation. Every industry and every industrial company will need to build two factories, one to build the machines and another to build their robotic AI.”

This is the long-term vision. The demand for compute and networking won't just come from data centers serving language models, but from a world of autonomous machines, robots, and smart factories, all needing to be trained and operated.

Staying at the leading edge

To compete with each other, AI labs must build more powerful and expensive models. But doing so crushes their own margins while sending a tidal wave of cash directly to NVIDIA.

Frontier models are better precisely because they "think longer," with queries requiring an exponential number of tokens. As more tasks shift from humans to AI, the world is not going to look back. There will always be a new leading-edge model tapping more into NVIDIA’s ability to deliver accelerated computing.

That’s the story of a perpetual and ever-expanding need for NVIDIA's platforms.

That’s it for today!

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Disclosure: I own AAPL, AMD, AMZN, GOOG, META, and NVDA in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.