🍿 Netflix: The Battle for Attention

Ads, live programming, and the push to become a daily habit

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Netflix no longer needs to prove that streaming can be profitable. It needs to prove that a mature streaming business can continue to grow. The market has expressed skepticism, with shares down more than 40% in the past year. The Q2 FY26 print offered no relief, with the stock falling roughly 8% after hours.

The company walked away from Warner Bros. Discovery last quarter, avoiding an expensive bidding war and collecting a $2.8 billion breakup fee. But the decision also removed a potential shortcut to the next phase of growth. Netflix must now generate it internally through higher prices, advertising, live programming, and a wider variety of content.

That task is becoming more urgent as competition for attention intensifies. YouTube continues to gain television share, free services like Tubi are growing, and traditional media companies are using sports to pull audiences into their platforms. Netflix’s response is to give viewers more reasons to open the app without weakening the economics that made the business so attractive.

Today at a glance:

🍿 Netflix Q2 FY26

📺 Becoming the bundle

📈 The battle for attention

💳 Stripe wants to buy PayPal

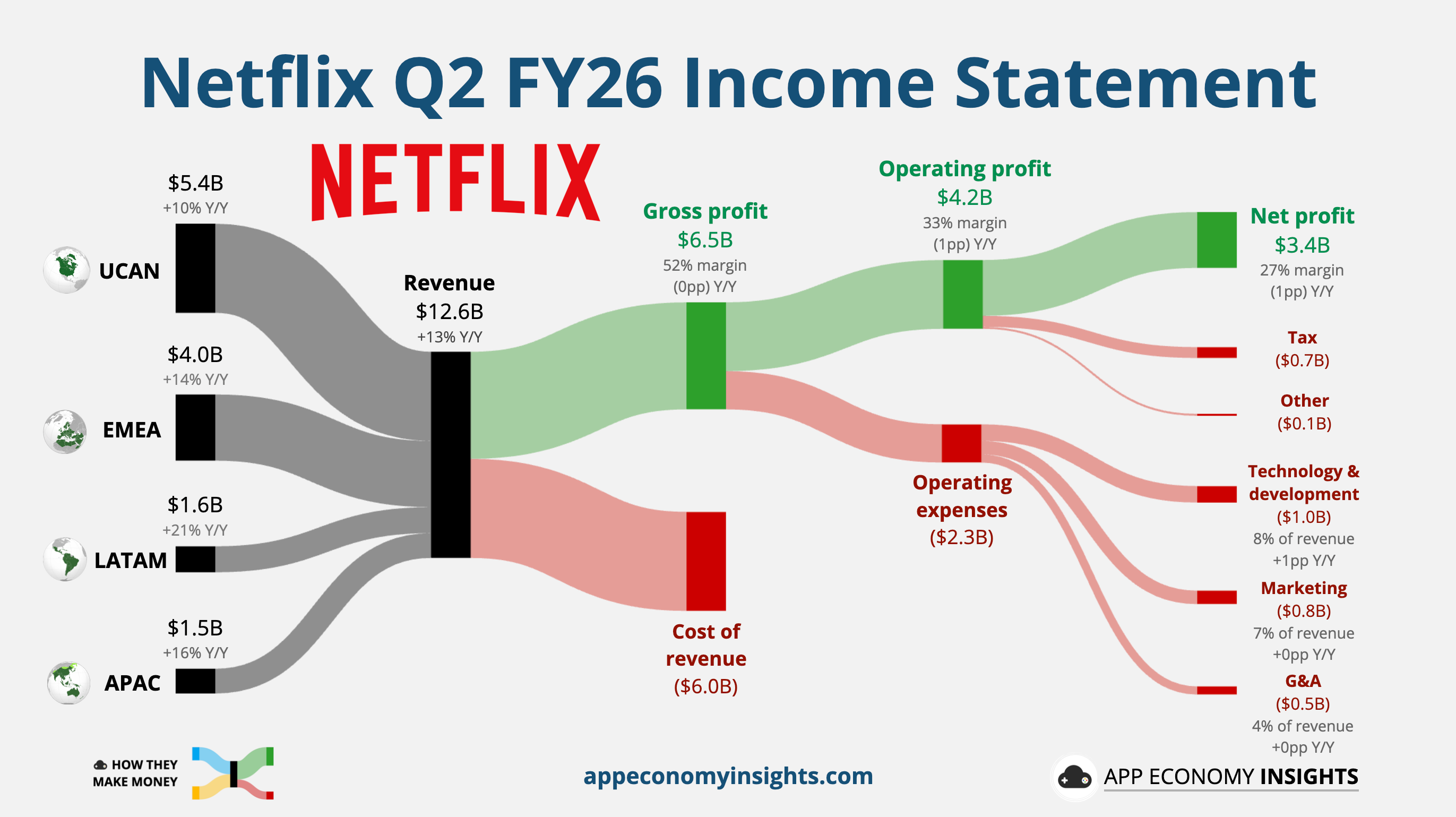

🍿 Netflix Q2 FY26

Income statement:

Revenue +13% Y/Y to $12.6 billion ($20 million miss).

Operating margin 33% (-1pp Y/Y).

EPS +11% Y/Y to $0.80 ($0.01 beat).

Balance sheet:

Cash and short-term investments: $9.1 billion.

Debt: $14.4 billion.

FY26 guidance:

Revenue +13%-14% to ~$51.2 billion with a narrower range.

Operating margin 31.5% (+2pp Y/Y, unchanged from last quarter).

So, what to make of all this?

📊 Solid, but no raise: The numbers came mostly in line with consensus. The operating margin exceeded Netflix’s own forecast, but the full-year outlook was only narrowed to the same midpoint. The slight Y/Y margin compression reflected front-loaded content amortization, with expansion set to resume in the second half. Management expects Q3 operating margin of 33%, up from 28% a year ago. In a world where outlooks are meant to be beaten and raised, it wasn’t quite what Wall Street was hoping for. The expected 12% Q3 revenue growth would be the slowest since 2023.

📢 Ads doubling on schedule: Netflix reiterated its expectation for roughly $3 billion in 2026 ad revenue, with US upfront commitments expected to close within weeks. Programmatic access is expanding to Pause Ads and live inventory this summer, reducing the manual friction that kept smaller advertisers out. How far the business scales will depend heavily on how automated it can become.

📺 Live punches above its weight: Members watched 97 billion hours in H1, up 2% Y/Y and accelerating from 1.5% growth in 2025. Live programming will consume just over 5% of 2026 content spending and drive only about 1% of view hours, yet it accounts for six of Netflix’s 10 largest new-member sign-up days over the past five years. With the NFL and Fury-Joshua, Netflix is buying sign-ups more than hours.

🤖 GenAI at scale: GenAI workflows touched ~300 titles in 2026, concentrated in post-production. Management framed it as shots and sequences that otherwise wouldn’t exist (enhanced crowds, historical battles, worldbuilding), delivered faster and cheaper than traditional methods. Netflix framed the technology as a capability expansion rather than a cost-cutting exercise.

💰 Record buybacks: Netflix repurchased $4.7 billion of stock, its largest quarter ever, with $27.1 billion of capacity remaining after April’s fresh $25 billion authorization. Free cash flow fell to $1.5 billion from $2.3 billion, but the drag was largely cash taxes tied to the Warner Bros. termination fee. The full-year ~$12.5 billion FCF target is unchanged.

📉 Retiring the engagement scoreboard: The What We Watched report moves from biannual to annual starting in 2027, deliberately decoupled from earnings. Management wants the quarterly conversation anchored on revenue and operating profit, not view hours. It’s the same signal as removing subscriber counts. Netflix wants to be judged as a scaled compounder, and it is steadily removing the metrics that invite a different debate. The change is more controversial because management has repeatedly presented engagement as its North Star. Reducing disclosure makes it harder to independently judge what is driving performance. Subscriber churn also remains undisclosed, an unusual omission for a subscription business.

📺 Becoming the bundle

Netflix spent years replacing scheduled television with an ad-free, on-demand library. Now it is selectively rebuilding many of the features it disrupted.

As of its last disclosure in May, the ad tier reached more than 250 million monthly active viewers, up from 190 million in November. Netflix expects advertising revenue to approximately double to around $3 billion this year, but audience growth alone is not enough. The next challenge is converting that reach into better targeting, higher fill rates, and more revenue per viewer.

That helps explain Netflix’s selective push into live sports. The company is not trying to replicate ESPN or Prime Video with full-season packages. Instead, it is focusing on tentpole events that attract large audiences, generate premium advertising inventory, and feel culturally significant.

Its new MLB deal includes Opening Night, the Home Run Derby, and the Field of Dreams game. Netflix will also carry five NFL games this season, including Thanksgiving Eve, Christmas Day, and a potentially decisive Week 18 matchup.

The approach creates appointment viewing without paying to fill hundreds of hours with lower-profile games. It may be a more capital-efficient way to use sports as an acquisition and advertising tool, although Netflix still has to prove audiences will follow isolated events to a platform that is not their year-round sports destination.

The strategy extends beyond sports. Netflix recently added TF1’s live channels and on-demand catalog directly to its service in France. Rather than acquiring a traditional media company, Netflix can integrate third-party programming and serve as the interface through which viewers access it..

The company is also expanding into video podcasts, short-form clips, and licensed videos from publishers. Together, these moves suggest Netflix wants to become more than the place viewers visit for a new season of Stranger Things. It wants to become an app they open every day.

That may increase engagement at a lower cost than premium scripted content. But it also creates strategic tension. Netflix is adding ads, scheduled programming, third-party channels, sports, podcasts, games, and vertical video. If those pieces do not feel cohesive, it risks recreating the bloated television bundle it once replaced.

📈 The battle for attention

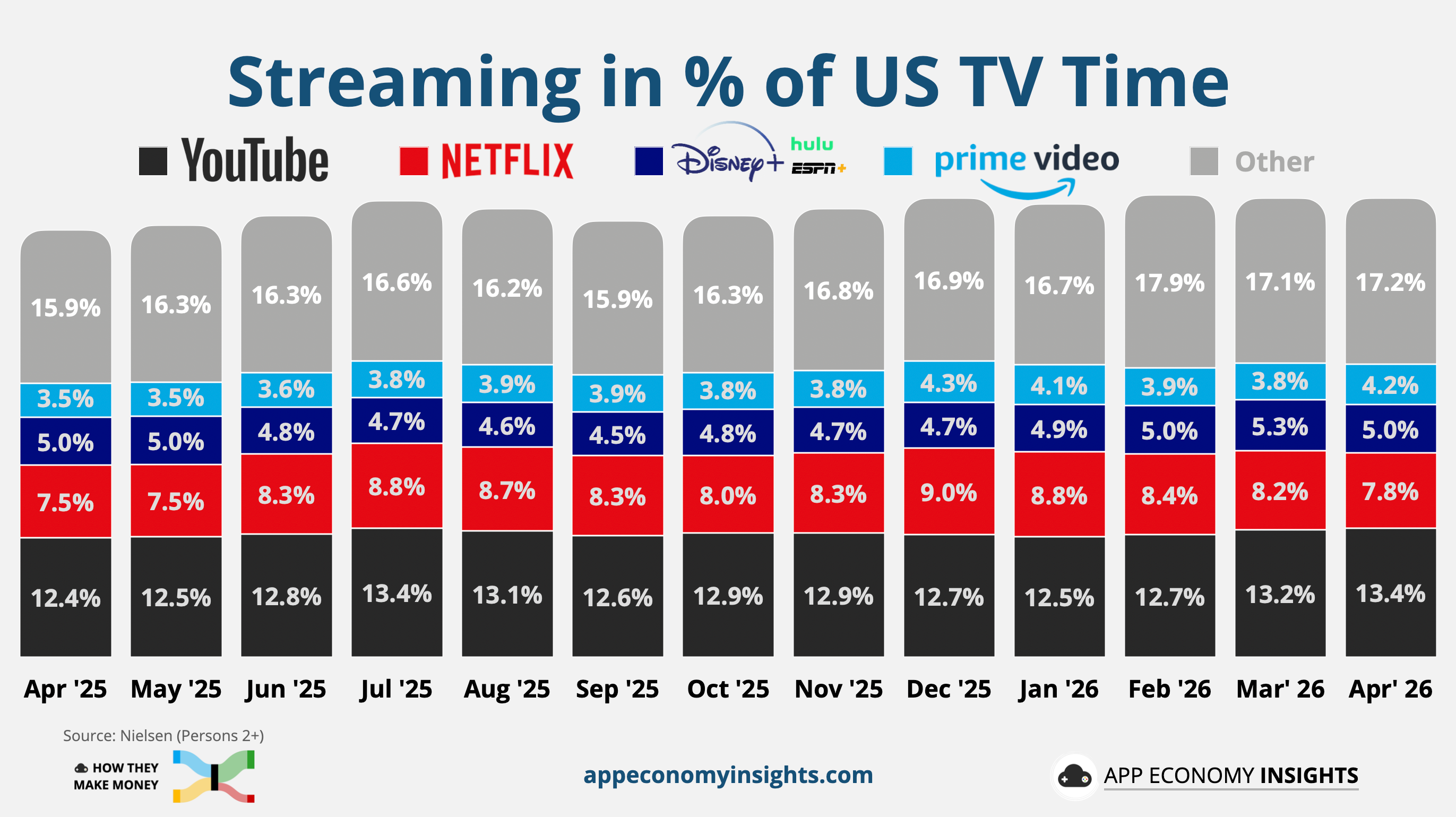

Netflix’s engagement challenge is visible in Nielsen’s latest data. Streaming represented 47.6% of US TV time in April, up from 44.3% a year ago and near record levels, while cable fell from 24.5% to 21.6%.

Netflix captured 7.8% of US TV time in April, up slightly from 7.5% a year ago but below its 9.0% December peak, when Stranger Things and Christmas Day football lifted viewing. Monthly figures are heavily influenced by release schedules, but the broader competitive trend is harder to dismiss.

YouTube increased its share to a record 13.4% in April. Amazon Prime Video reached 4.2%, helped by its new NBA package, while Tubi hit a platform record of 2.3%. The competitors gaining the most attention are not relying exclusively on expensive scripted series. They combine creator content, sports, free programming, or multiple forms of entertainment.

Netflix argues that retention and customer satisfaction matter more than raw hours watched. That is reasonable for a subscription business. But engagement still supports nearly every part of its strategy. More viewing creates more advertising inventory, improves the return on content spending, reduces churn, and makes future price increases easier to absorb.

Bottom line: Netflix’s ad tier, pricing power, and operating leverage can support low double-digit growth. But at a premium valuation, investors need evidence that its broader entertainment strategy is producing more engagement, stronger monetization, and durable returns on spending. Otherwise, Netflix risks becoming more complex without becoming more valuable.

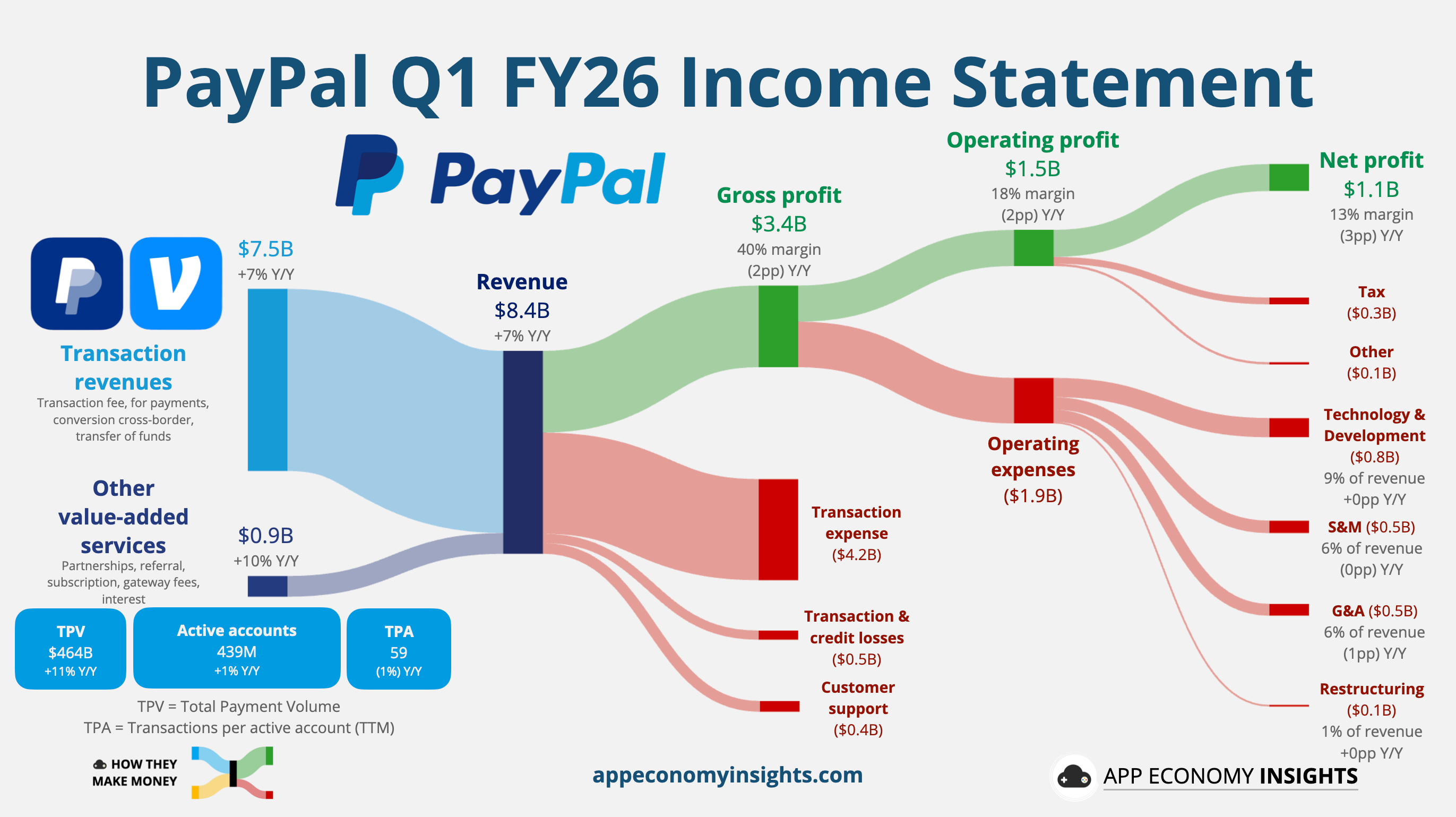

💳 Stripe wants to buy PayPal

PayPal may be about to cash out. Reuters first reported that Stripe and private equity firm Advent International have offered $60.50 per share to acquire the company, valuing it at more than $53 billion. The proposal is reportedly backed by approximately $50 billion of committed financing.

This is still an unsolicited offer rather than an agreed deal. PayPal has not formally responded, and the companies involved have declined to comment. However, PayPal has reportedly been working with Goldman Sachs and Evercore to evaluate strategic options, including a potential sale or breakup. The company is not necessarily looking for a buyer, but it appears willing to consider what one might pay.

🛒 Stripe Gets the Consumer

The strategic logic is straightforward. Stripe built its business by helping merchants accept payments online, becoming one of the most important infrastructure providers in digital commerce. Consumers use Stripe constantly, but most barely know it exists. PayPal brings the missing half of the network: 439 million active accounts, approximately $1.8 trillion in annual payment volume, and Venmo, one of the strongest consumer payment brands in the United States.

A combination would give Stripe a much larger presence on both sides of a transaction. Stripe could continue powering payments for merchants while PayPal, Venmo and Stripe’s Link wallet deepen its relationship with consumers. Braintree would add another large merchant-processing platform, while PayPal’s stablecoin and crypto assets would complement Stripe’s recent acquisitions of Bridge and Privy.

In theory, that creates one of the most comprehensive payment ecosystems in the world. In practice, Stripe would also inherit overlapping products, aging technology, and a collection of businesses PayPal has struggled to integrate. Buying PayPal could accelerate Stripe’s expansion into consumer payments, but combining the two companies without distracting the faster-growing business would be a major undertaking.

💵 Private Equity Sees the Cash Flow

For Advent, the attraction is less about strategic fit and more about cash flow. PayPal generated approximately $5.6 billion of reported free cash flow last year, or $6.4 billion on an adjusted basis. A $53 billion purchase price values the company at roughly 8 times adjusted free cash flow, before considering debt, transaction costs, and the cost of financing.

That is the kind of setup private equity looks for. It’s a durable but unloved business, with strong cash generation, and a cost structure that can still be cut. Away from the public market, PayPal could restructure more aggressively without every investment or layoff being judged against the next quarter. Stripe and Advent could eventually relist the company, sell individual assets, or separate the consumer and merchant businesses.

🤔 Is $60.50 Enough?

The offer looks generous relative to PayPal’s depressed share price, but less so relative to the cash flow and strategic assets the buyers would receive. PayPal traded above $78 only a year ago, and its network of consumers and merchants would be extremely difficult to recreate from scratch.

Michael Burry, who owns PayPal shares, has already called the proposal too low. His valuation may prove optimistic, but the broader point is reasonable: Stripe and Advent would not be offering $53 billion unless they believed PayPal could ultimately be worth substantially more.

Bottom Line: PayPal became vulnerable because investors stopped believing in its turnaround. Stripe and Advent are betting that the assets are worth more than the public company built around them. At $60.50 per share, shareholders receive a clean exit from years of underperformance. But the first offer may establish only that PayPal is in play, not the price that ultimately gets it sold.

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own AMZN, META, and NFLX in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.