🏦 Banking on Volatility

A record trading and dealmaking haul powered Q2

Welcome to the Premium edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

A new earnings season is here with the big banks kicking us off.

Later this week, we’ll have a look at Netflix and the picks and shovels of the AI era, TSMC and ASML.

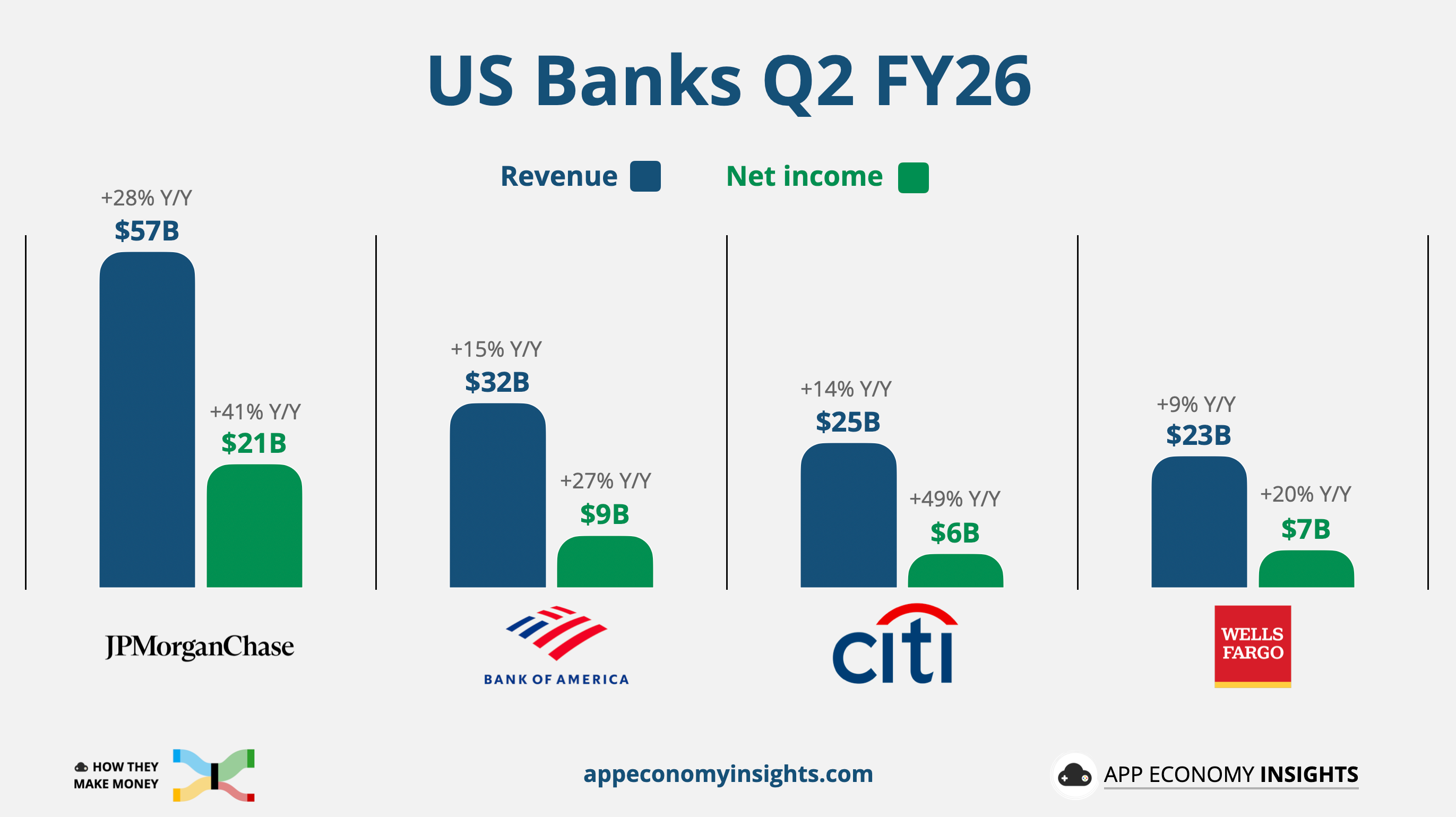

Four of the largest US banks just booked a combined $43 billion in profit, smashing records and beating estimates. They did it despite the Iran war, sticky inflation, and mounting doubts about the staying power of the AI boom.

Even as profits hit new records, the bank chiefs kept pointing to risks shifting beneath the surface: geopolitics, sticky inflation, and elevated asset prices.

High rates and market volatility are a windfall for the banks, while the gap keeps widening between households riding record markets and those squeezed by the cost of living.

Let’s break down the results.

Today at a glance:

JPMorganChase: As Good As It Gets

Bank of America: A Blowout With Caveats

Citigroup: Four Out of Five

Wells Fargo: Fees Do the Heavy Lifting

The Big Picture

As a reminder, banks make money through two main revenue streams:

💵 Net Interest Income (NII): The difference between interest earned on loans (like mortgages) and interest paid to depositors (like savings accounts). It’s the primary source of income for many banks and depends on interest rates.

👔 Noninterest Income: The revenue from services unrelated to interest. It includes fees (like ATM charges), advisory services, and trading revenue. Banks relying more on noninterest income are less affected by interest rate changes.

Here are the significant developments shaping Q2 FY26:

💰 Records fall across the board: The four biggest lenders beat expectations despite the Iran war and sticky inflation. The common engine was the trading floor. Every desk cashed in on a volatile quarter, and the results were strong enough that Jamie Dimon told analysts conditions are “getting close to as good as it gets.”

🎰 Trading and dealmaking do the work: Equities desks set records nearly everywhere, led by JPMorgan (+86% Y/Y). A dealmaking revival capped by the SpaceX IPO pushed investment banking to its best showing since 2021. Volatility that could have been a threat became the quarter’s biggest profit source.

🏦 Margin divergence: Beneath the capital-markets boom, the lending picture split. JPMorgan raised its full-year net interest income guide, but net interest margins compressed at Bank of America, Citi, and Wells Fargo as deposit costs stayed stubbornly high. The easy-money era of NII growth is uneven, and the banks leaning hardest on rates are feeling it most.

💵 Capital floods back to shareholders: Confidence showed up in the payouts. JPMorgan authorized a fresh $50 billion buyback and a 10% dividend hike, Wells Fargo repurchased ~$7 billion in the first half and lifted its dividend 11%, and Citi and BofA kept returning capital aggressively. With balance sheets flush, the big banks are signaling they see more room to run.

🛢️ Energy relief, already reversing: June CPI cooled to +3.5% Y/Y, driven almost entirely by a 9.7% drop in gasoline after the Iran ceasefire reopened the Strait of Hormuz. That relief is unwinding fast. The ceasefire collapsed on July 8, oil is climbing again, and the July inflation print will look very different.

📉 The K-shaped consumer holds: Card spending rose 9% Y/Y at both BofA and Wells Fargo, and provisions came in below expectations across the group, signs the consumer is still spending and paying on time. But management remained cautious about affordability for lower-income households, and the divide between asset-rich households and everyone else remains.

🌋 Risks below the surface: Even while celebrating records, Dimon warned of “risks shifting below the surface like tectonic plates,” naming geopolitical conflict, sticky inflation, large fiscal deficits, and elevated asset prices. Charlie Scharf echoed him, cautioning that favorable conditions “do not go on forever.”

🔑 Takeaway: The big banks are posting record profits amid a trading and dealmaking boom, returning capital freely, and leaning on a consumer that’s still holding. But margins are thinning where the boom isn’t reaching, and management keeps pointing to the same tensions that leave little room for error.

Let’s visualize them one by one and highlight the key points.

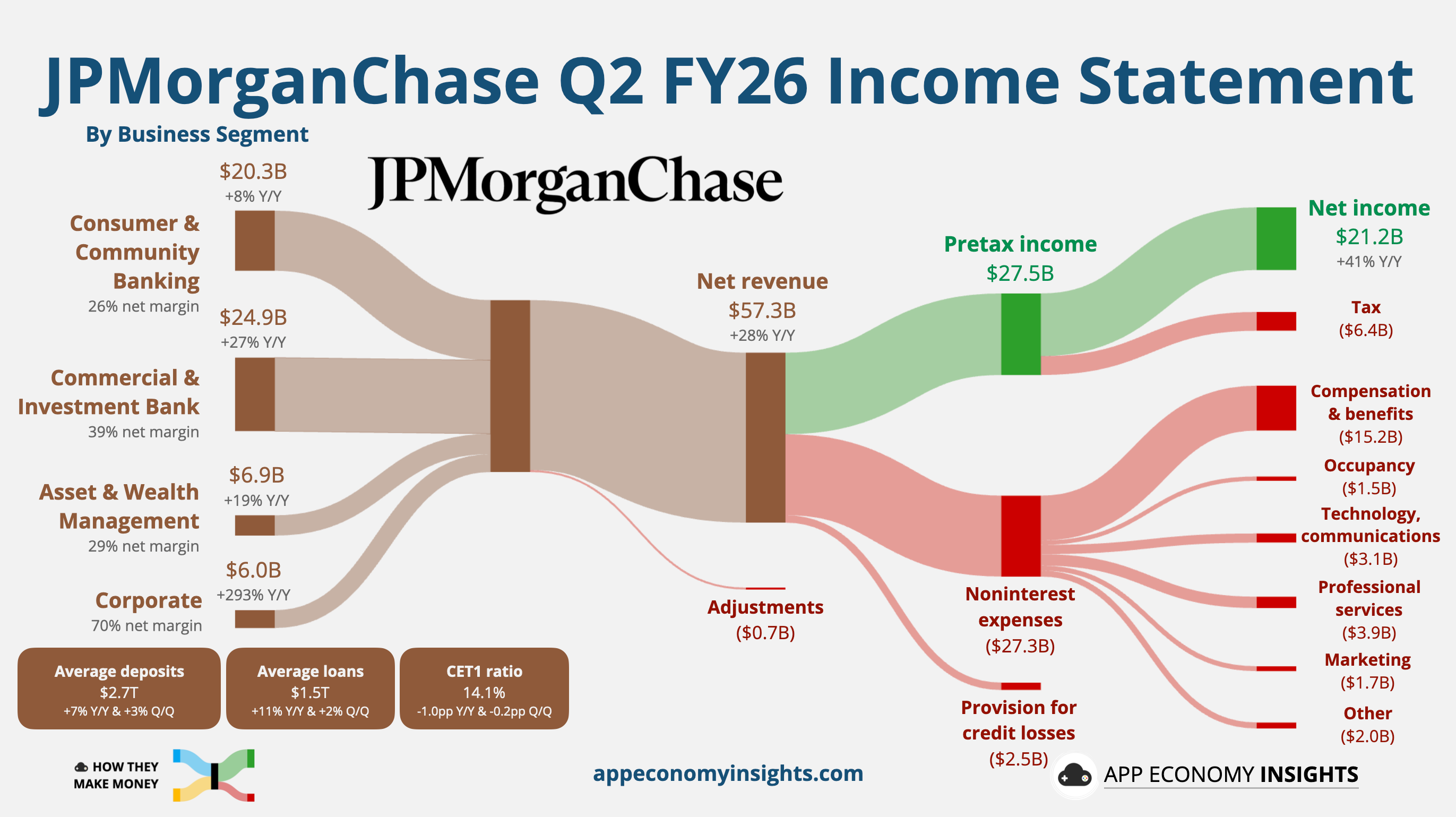

JPMorganChase: As Good As It Gets

Net revenue grew 28% Y/Y to $57.3 billion ($6.7 billion beat):

Net interest income (NII): $25.5 billion (+10% Y/Y).

Noninterest income: $31.8 billion (+47% Y/Y), lifted by a $4.6 billion one-time Visa gain.

Net income: $21.2 billion (+41% Y/Y).

Adjusted EPS: $6.14 ($0.34 beat).

Key developments:

📈 Equities smash the record: JPMorgan’s stock traders pulled in $6.0 billion (+86% Y/Y), beating even the highest analyst estimate and pushing total trading revenue to a fresh record of $12.1 billion (+35% Y/Y). The volatility that started with the Iran war and rippled through global equity markets, including a chaotic stretch in Korean stocks, handed the desks their best quarter ever.

💳 The Visa windfall: A long-held Visa stake paid off to the tune of $4.6 billion, plus another $1.0 billion in equity investment gains. Reported EPS of $7.70 crushed consensus, but ~$1.56 of that was one-time. Even excluding the windfall, the bank still delivered a 23% return on tangible equity.

🚀 Dealmaking roars back: Investment banking fees jumped 30% Y/Y to $3.3 billion, riding the record SpaceX IPO, heavy index rebalancing, and a wave of AI-related financing. M&A advisory rose 20%, though that fell short of the 27% expected by analysts. CFO Jeremy Barnum called the environment “dynamic and interesting across a whole variety of dimensions.”

🏦 NII guidance raised: Management lifted the NII outlook to ~$105.5 billion (from $103 billion), as higher-for-longer rates extend the tailwind. The card net charge-off forecast also improved, to ~3.2% from 3.4%, a sign that consumer credit is holding better than feared.

💸 Expenses are the catch: Full-year expense guidance climbed to ~$107.5 billion (from $105 billion). Management framed the increase as the cost of doing more business, tied to the elevated activity levels that drove the revenue outperformance.

💰 Capital floods back to shareholders: JPMorgan raised its quarterly dividend 10% to $1.65 and authorized a fresh $50 billion buyback, with CET1 at a comfortable 14.1%. With Dimon having pegged excess capital near $40 billion, the firm has ample room to keep returning cash even as Basel III capital rules loom.

🔑 Takeaways: Every business line set records, and the NII guide flipped from headwind to tailwind versus Q1. Underneath a one-time Visa boost, JPM showed it can monetize volatility, dealmaking, and higher rates all at once.

Key quote:

CEO Jamie Dimon: “These results were the product of a particularly favorable environment with an elevated level of market activity, as well as rigorous execution, years of consistent investment, and thoughtful capital deployment.”