🏴☠️ Can Ubisoft Turn it Around?

Sony just killed the disc

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

💿 Sony just killed the disc

Starting January 2028, no new PlayStation game will ship on a disc, third-party publishers included. That timeline caught some fans off guard, but the disc gave up its usefulness years ago. Critical day-one patches are now standard, so the plastic in the box is already just a glorified install key with better packaging. Digital accounts for ~80% of Sony's full-game sales, and many smaller titles skip the box altogether.

Take-Two Interactive got a head start on Sony. Its upcoming game, GTA VI, will ship this November with a download code in a box and no disc at all. It’s an admission that a disc has become more of a liability than an asset. A physical disc means locking the code weeks before launch and hoping it doesn’t leak in the meantime.

Killing the disc kills the resale market that’s quietly taxed every publisher for decades. A used copy undercuts the full-price version by a few dollars within days of launch, and the publisher sees nothing from the resale. Publishers tolerated that leak while the market was growing. But Console was gaming's slowest-growing segment in 2025, up just 3% Y/Y to $45 billion, or 22% of the ~$200 billion global games market now dominated by mobile.

AAA budgets keep climbing, and studio layoffs have become routine at big publishers. Microsoft just proved how bad that math has gotten. Xbox is cutting 3,200 jobs, 20% of its workforce, and divesting four studios. CEO Asha Sharma told staff the business is "not healthy," operating at margins three to ten times below those of comparable platform and publishing peers. A business model that stops leaking resale value to GameStop is exactly the fix a stagnant industry needs.

Today at a glance:

💰 Pricing the pure plays

🏴☠️ Can Ubisoft turn it around?

💰 Pricing the pure plays

While consoles have trailed mobile gaming for years, GTA VI is shaping up to be the biggest single entertainment release in history, game or otherwise. Some analysts see it selling over 40 million units at launch, with the lowest-priced edition running at $80.

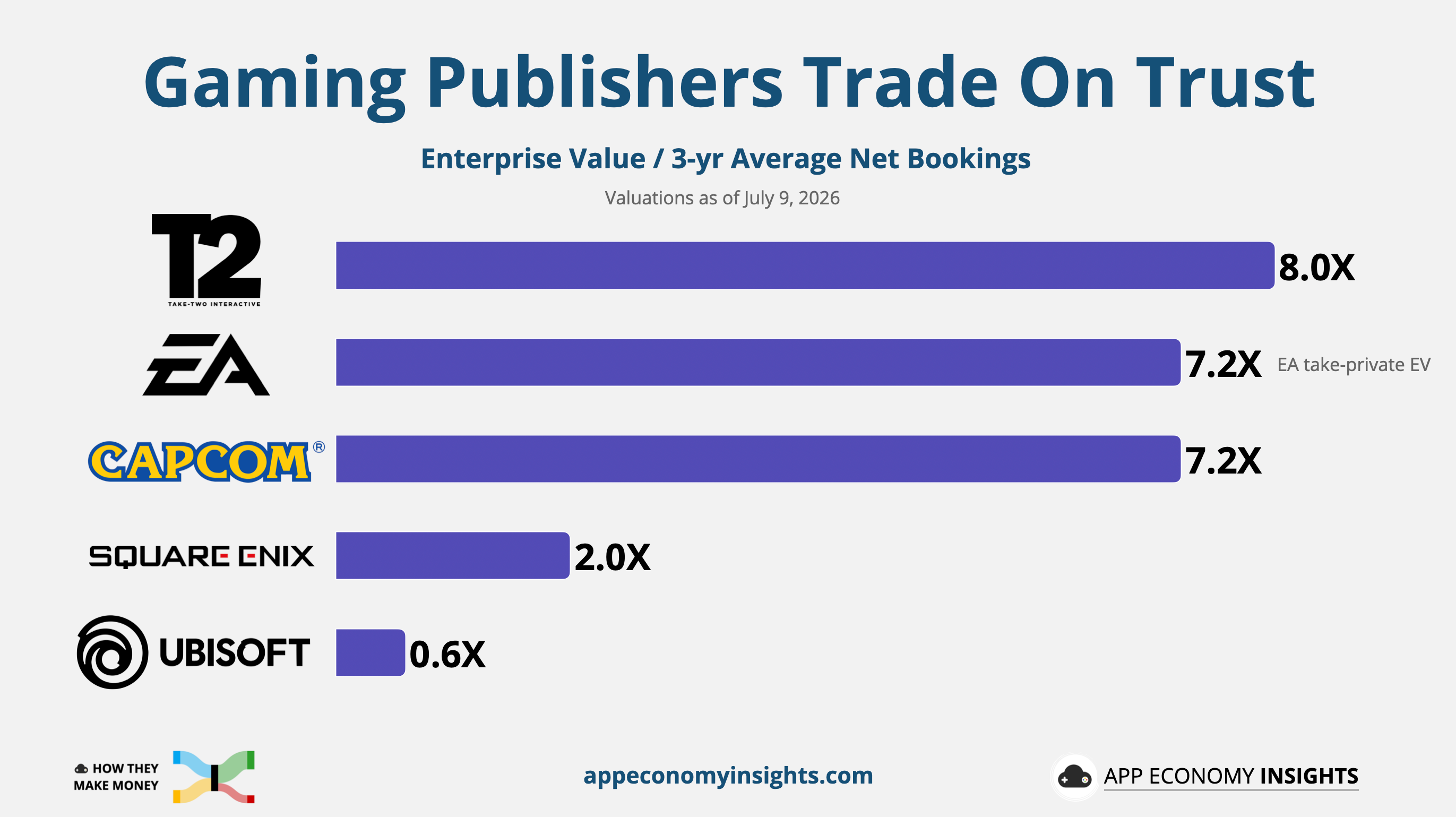

The market is already pricing that in. Take-Two now trades at 8.0x its average net bookings over the past three years, the highest multiple in this peer group.

Here's how the net bookings multiples of the leading console publishers stack up:

🇺🇸 Take-Two (8.0x): With an enterprise value near $47 billion, Take-Two is the largest publicly traded standalone gaming publisher. FY27 guidance has net bookings jumping to ~$8.1 billion from $6.7 billion in FY26, which would pull the forward multiple closer to 6x. The market is already pricing a big GTA VI launch.

🇺🇸 EA (7.2x): The Saudi PIF-led consortium took the company private at a $55 billion enterprise value. Live-service sports franchises give EA the most predictable revenue base in the group, which is exactly what a private buyer pays up for.

🇯🇵 Capcom (7.2x): The Japanese publisher is valued at nearly $7 billion and trades at a premium multiple, supported by a standout margin profile (~39% operating margin in FY26). A successful remake strategy turned Resident Evil from nostalgia into a repeatable growth engine, while Monster Hunter and Street Fighter continue to prove that Capcom can refresh mature franchises with strong commercial results. Capcom’s efficiency and consistent execution are what earn a multiple this rich.

🇯🇵 Square Enix (2.0x): Square Enix trades at the low end of the group, with a ~$4 billion valuation. Its RPG franchises, Final Fantasy and Dragon Quest, carry the portfolio. Operating margin sits around 13%, roughly half the peer average, dragged down by uneven execution, bloated budgets, and several high-profile misses. An activist investor is now pushing management to close that gap.

🇫🇷 Ubisoft (0.6x): The French publisher has fallen from a €12 billion enterprise value in 2018 to just over €1 billion today, a collapse driven by escalating budgets on major titles, repeated project cancellations, and franchise fatigue across Assassin's Creed and Far Cry.

Bottom Line: Every publisher in this cohort benefits from Sony killing the disc. But the multiple investors are willing to pay comes down to trust. Great IP only matters if it ships on time and turns into cash.

🏴☠️ Can Ubisoft turn it around?

Assassin’s Creed Black Flag Resynced, a full remake of the studio’s 2013 pirate adventure, just launched on July 9. The original game has been played by over 34 million unique players. Ubisoft wants to follow in Capcom’s footsteps by modernizing its biggest hits. Commercial success of remakes is more predictable, and upfront production costs are usually lower, making it a potent combo. Ubisoft’s CEO, Yves Guillemot, officially confirmed that the company is developing multiple remakes of older Assassin’s Creed games.

The remake is arriving while the company is priced as if bankruptcy is on the horizon. Ubisoft has an enterprise value of ~€1.2 billion, with average annual net bookings of nearly ~€2 billion. Even multiplying this valuation by 3 would put it merely in line with struggling publisher Square Enix.

That price implies a company in slow-motion liquidation rather than an underperforming publisher. As of July 2026, nearly 14% of Ubisoft stock on Euronext Paris is short (people betting the stock will go down).

So what’s happening here? Let’s look at the underlying business.

New Structure, New Capital

Ubisoft spent January reorganizing into five Creative Houses, decentralizing decisions that used to run through the center. Vantage Studios ended up holding the crown jewels: Assassin’s Creed, Far Cry, and Rainbow Six. The other four Houses split the rest of the portfolio across multiplayer shooters (Ghost Recon, The Division), live services (The Crew), and casual and family titles (Rayman).

Tencent closed a €1.2 billion investment in Vantage Studios in November 2025, taking a 26% economic interest while Ubisoft retains exclusive control and keeps consolidating the studio’s results. The deal valued Vantage Studios at a pre-money enterprise value of €3.8 billion. That structure suggests that both sides see more value in Vantage than the market is currently assigning to Ubisoft as a whole (€1.2 billion). But the Guillemot family's control and Tencent's right of first refusal make an EA-style buyout unlikely.

Tencent’s cash injection did real work on the balance sheet. Ubisoft closed FY26 (ending in March) with an adjusted net debt of €0.2 billion and cash reserves of €1.3 billion, a very different position from the one that had investors bracing for a covenant breach a year ago.

The relief could be temporary, though. Bondholders can demand ~€0.5 billion back in November. Another ~€0.7 billion follows in late 2027. That is nearly the entire cash pile due before the FY28/FY29 slate can fully repair free cash flow. Add a year of guided burn, and the math stops working. Ubisoft's near-term future hinges on refinancing.

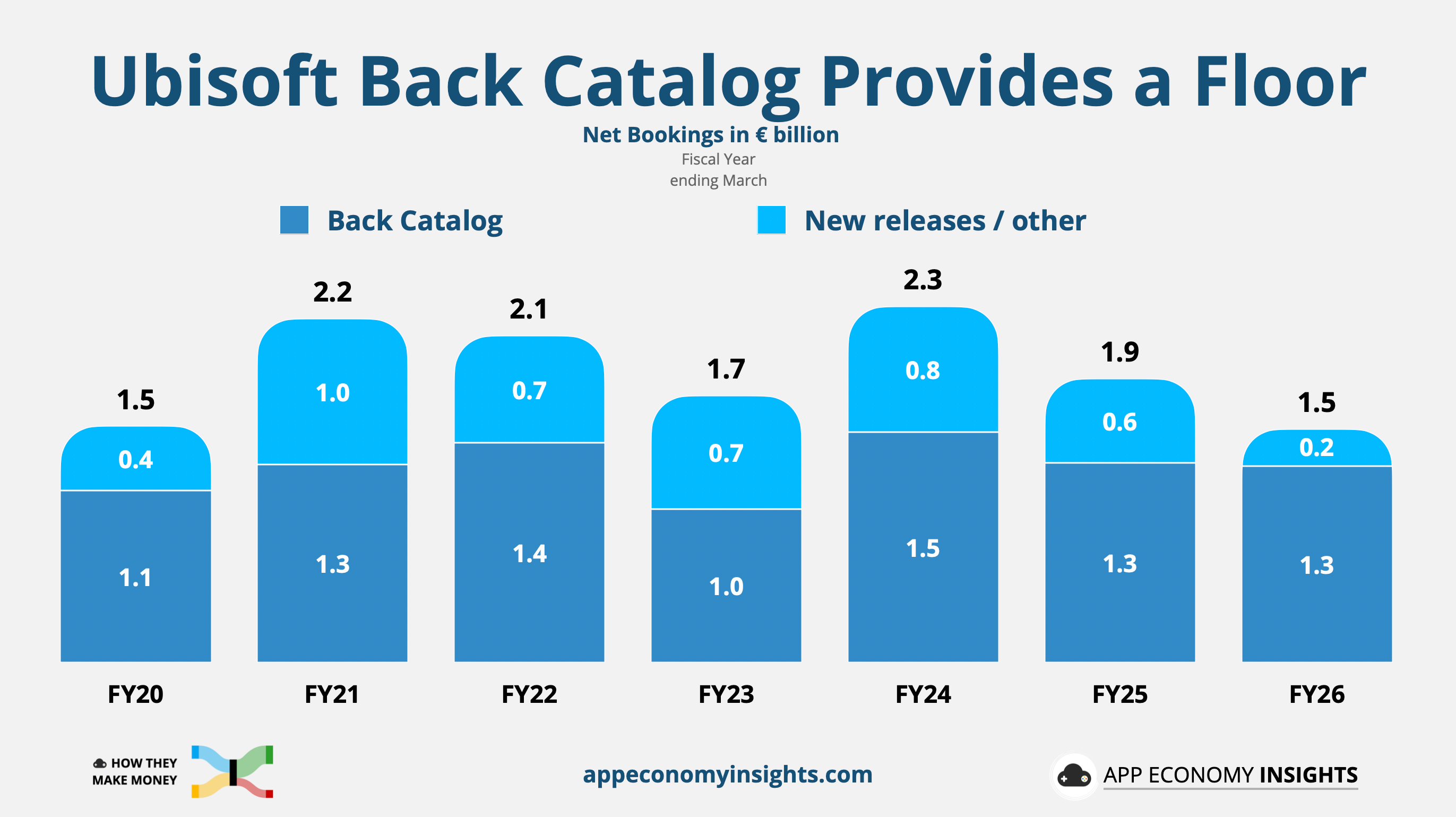

The Back Catalog is already carrying the business

In FY26 (ending in March), Ubisoft’s back catalog generated €1.3 billion in net bookings, compared with just €0.2 billion from new releases and other revenue. That’s 84% of the entire business running on games released in previous years. It illustrates the durability of a digital catalog library that gives the company a revenue floor, even without new tentpole releases. The disc-free future acts as a tailwind for this revenue line, with no second-hand market eating away at the long tail of legacy franchises.

A pipeline with execution risks

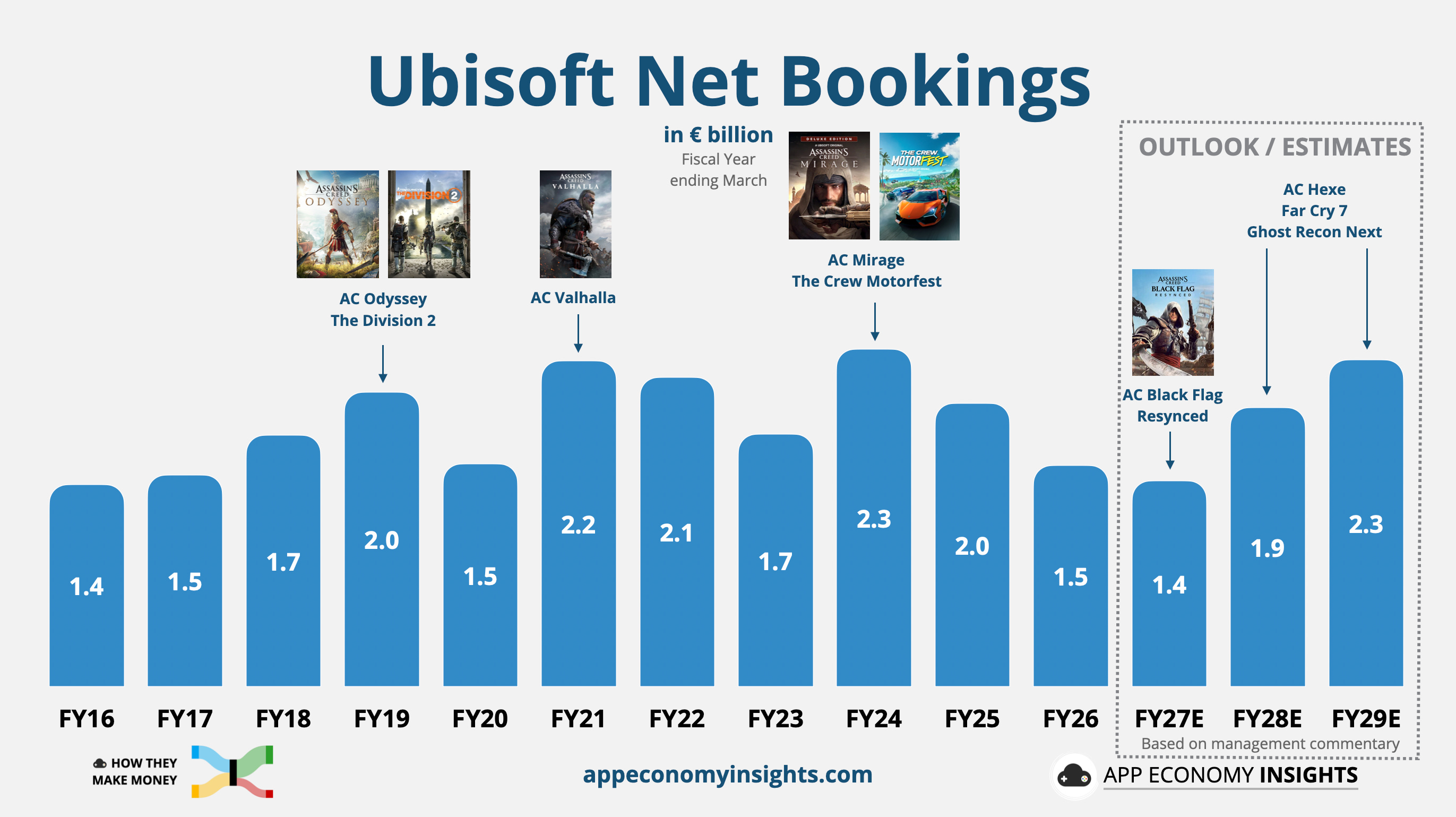

FY24: Net bookings peaked at €2.3 billion, driven by Assassin’s Creed Mirage and The Crew Motorfest, with strong back-catalog performance.

FY26: Net bookings fell to €1.5 billion, with no notable new releases.

FY27: Guidance for the fiscal year that started in April points to a high-single-digit decline, implying roughly €1.4 billion in net bookings. Black Flag Resynced is the main new release, and Ubisoft’s guidance appears to leave room for upside. The game does not need to be a massive blockbuster to improve the narrative. That is the advantage of low expectations.

Ubisoft plans for a rebound in FY28 and FY29, when management expects to ship Assassin’s Creed Hexe, Far Cry 7, and a new Ghost Recon, lifting bookings closer to the ~€2 billion of previous years. A success for Black Flag Resynced could remind the market that the IP still works. It would certainly be a good idea ahead of a Netflix tie-up with an Assassin’s Creed show expected in the coming months. The main risk ahead is that the upcoming games could be postponed if the quality is not there, leaving the company in a cash flow hole.

The cash burn is real

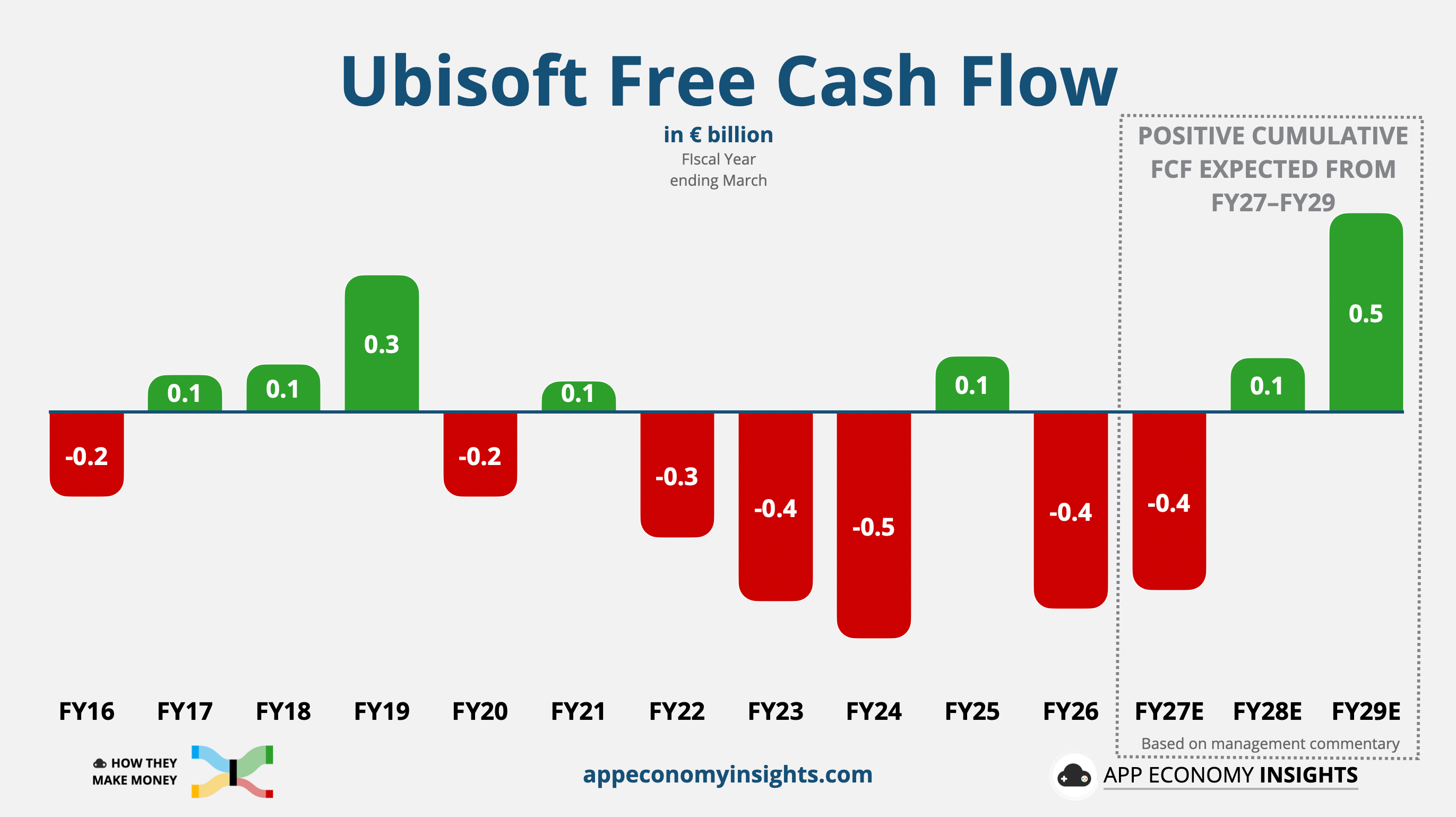

Free cash flow has been negative in four of the last five fiscal years, including -€0.5 billion in FY24 and -€0.4 billion in FY26. Management already stated that free cash flow consumption in FY27 will be no more than -€0.5 billion, but that’s a low bar.

On the bright side, Ubisoft expects cumulative free cash flow to turn positive from FY27 through FY29. That would be good news for liquidity and solvency. But that inflection point still depends on a set of games to actually launch over that period.

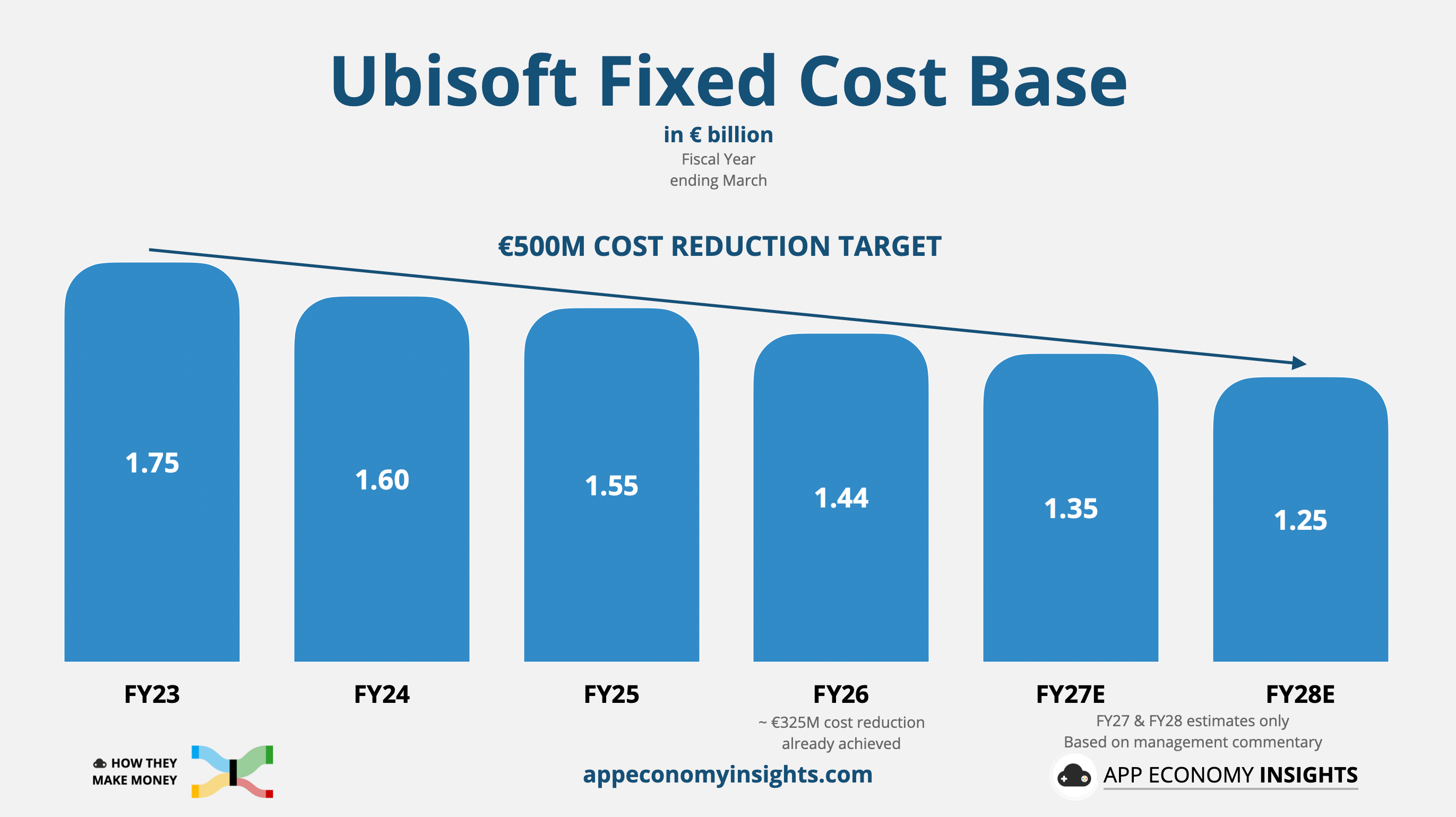

To achieve such a rebound, Ubisoft has been cutting fixed costs aggressively, reducing them from €1.75 billion in FY23 to €1.44 billion in FY26. The target is €1.25 billion by the end of FY28. Whatever happens to bookings, Ubisoft is guiding to a structurally smaller cost base than the one that burned through FY23 and FY24. To do so, they have reduced their workforce from ~20,000 to roughly ~16,000.

The cost reset lowers the hurdle, but it does not solve the problem on its own. Ubisoft still needs enough successful releases to spread that smaller cost base over the same bookings pool.

Why it matters:

The market factors a solvency risk: It also assumes the company may face significant dilution if it needs to raise capital to meet near-term obligations. The catalog is de-risked, but there is no margin of safety for the next few high-profile titles. Ubisoft still has to navigate near-term debt maturities while proving that FY27 is the trough and FY28/FY29 can restore positive cash flow.

There is an asymmetric upside if FCF rebounds: Sub-1x EV/bookings against a back catalog this large only makes sense if the market expects the catalog itself to erode. But the back-catalog net bookings trend suggests the portfolio has been very resilient and that only one high-profile game per year is needed to keep the company in the black moving forward, which seems like a very low bar for ~16,000 employees.

Tencent put a real price on the crown jewels: The minority stake in Vantage Studios signals that Tencent sees value in the main IPs and studios. That value was €3.8 billion just a few months ago.

A challenging history: Ubisoft has been plagued with toxic workplace allegations, game controversies, repeated delays, and the founding Guillemot family keeps tight control, with family members placed in key leadership positions.

Bottom Line: Ubisoft doesn’t need a miracle. FY27 guidance looks conservative, the catalog still produces more than €1 billion a year, and fixed costs are finally moving lower. But the company still needs to ship the next major slate by March 2029 and prove the new cost base can turn bookings into cash. At 0.6x average net bookings, the market is not paying for that yet. After years of delays, cancellations, and uneven launches, execution remains the hard part. If cash burn persists, the balance sheet becomes the only story that matters.

That's it for today.

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own AAPL, GOOG, META, and TCEHY in App Economy Portfolio. I also personally own UBSFY. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.