🦚 Comcast: The Great Unbundling

Plus Meta's cloud business and Nike’s margin mirage

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

☁️ Meta is pulling an Amazon move

Meta has been shunned by the market this year for overspending on AI. But something good might come out of it.

Bloomberg reported Wednesday that Meta is building a cloud business to rent out its excess AI compute, muscling onto turf held by AWS, Azure, and Google Cloud.

Zuck poured hundreds of billions into data centers for his superintelligence dream, but he might have bought more than he needs. The stock surged nearly 10% on the news, as the new business could offset some of that rapidly growing CapEx line.

It wasn’t good news for everyone. CoreWeave fell 13% and Nebius dropped 15%. Meta spent the past year as one of their biggest customers. Now it could turn into a massive new rival.

It also sharpens the question of where we are in the cycle: did Meta overspend, or is Zuck embracing a new strategy?

Starting a cloud business also confirms that Meta expects to have capacity worth selling. The generous read is that Meta is betting demand keeps coming, the same bet Amazon made when it launched AWS nearly two decades ago.

Zuck called it “definitely on the table” back in May, noting outsiders ask to buy Meta’s compute almost every week. The company, spending up to ~$145 billion this year on its own moonshot, now has a Plan B: if superintelligence takes its time, collect rent.

Today at a glance:

🦚 Comcast: The Great Unbundling

👟 Nike: Not a Recovery Yet

🦚 Comcast: The Great Unbundling

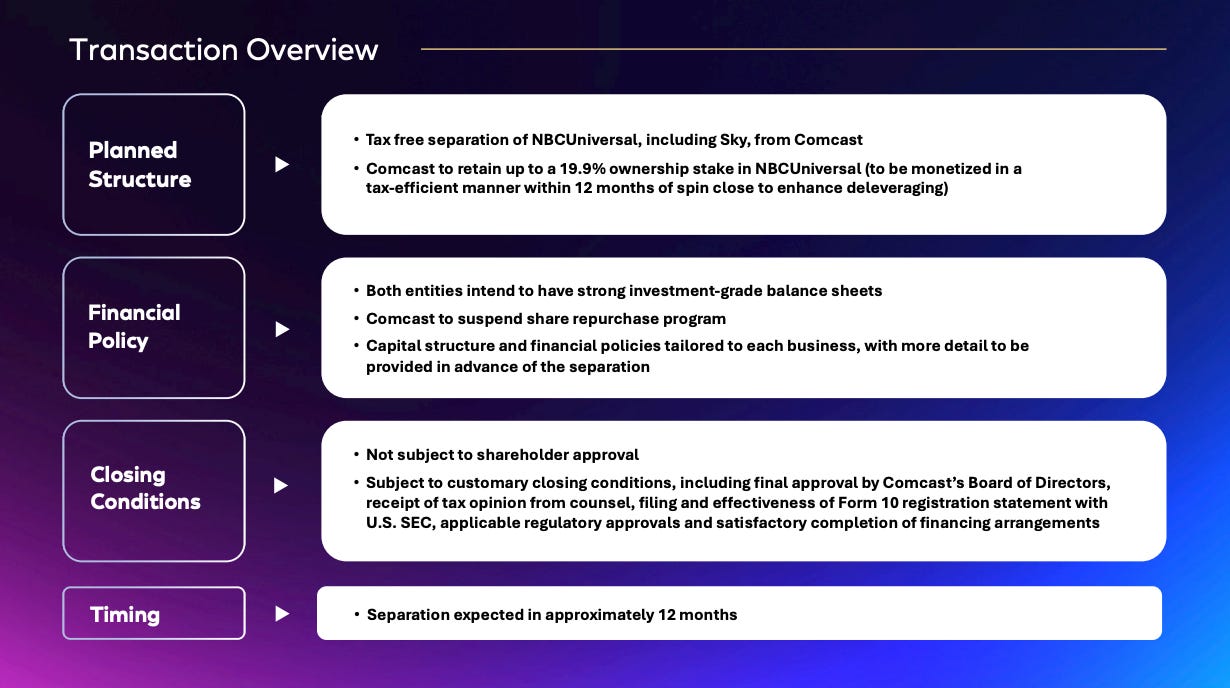

Comcast is unwinding the ~$30 billion bet it spent a decade defending.

The company is splitting in two, separating NBCUniversal and Sky into a standalone media business, while the parent keeps broadband, wireless, and Comcast Business.

The stock jumped as much as 17% intraday, its biggest move since 2008, before settling up ~5%. Not bad for a name that was down ~22% on the year going in.

This is the second breakup step in less than a year. In January, Comcast spun off its cable networks (CNBC, USA, MS NOW, Golf Channel) into Versant, which fell 13% on its Nasdaq debut and has traded sideways since. The channels were the appetizer. Now the studios, parks, NBC, Peacock, and Sky are leaving too.

Who keeps what

Comcast retains the cash machine: the largest converged network across 65M+ homes, the largest WiFi network, and a fast-growing wireless business in a $200B+ market. Michael Angelakis, the former CFO who helped architect the 2011 NBCUniversal purchase, returns as CEO to run the company now shedding it (you can’t make this up.)

NBCUniversal walks away with the IP: Universal Studios, the theme parks (including Epic Universe), NBC, Telemundo, Bravo, Peacock, and Sky. Co-CEO Mike Cavanagh takes over. Brian Roberts, whose family controls both through a dual-class structure, stays “actively involved” in each.

The structure is a tax-free separation in roughly 12 months, with Comcast holding up to a 19.9% stake in NBCUniversal to sell down and cut debt. The buyback is suspended until then.

Why now

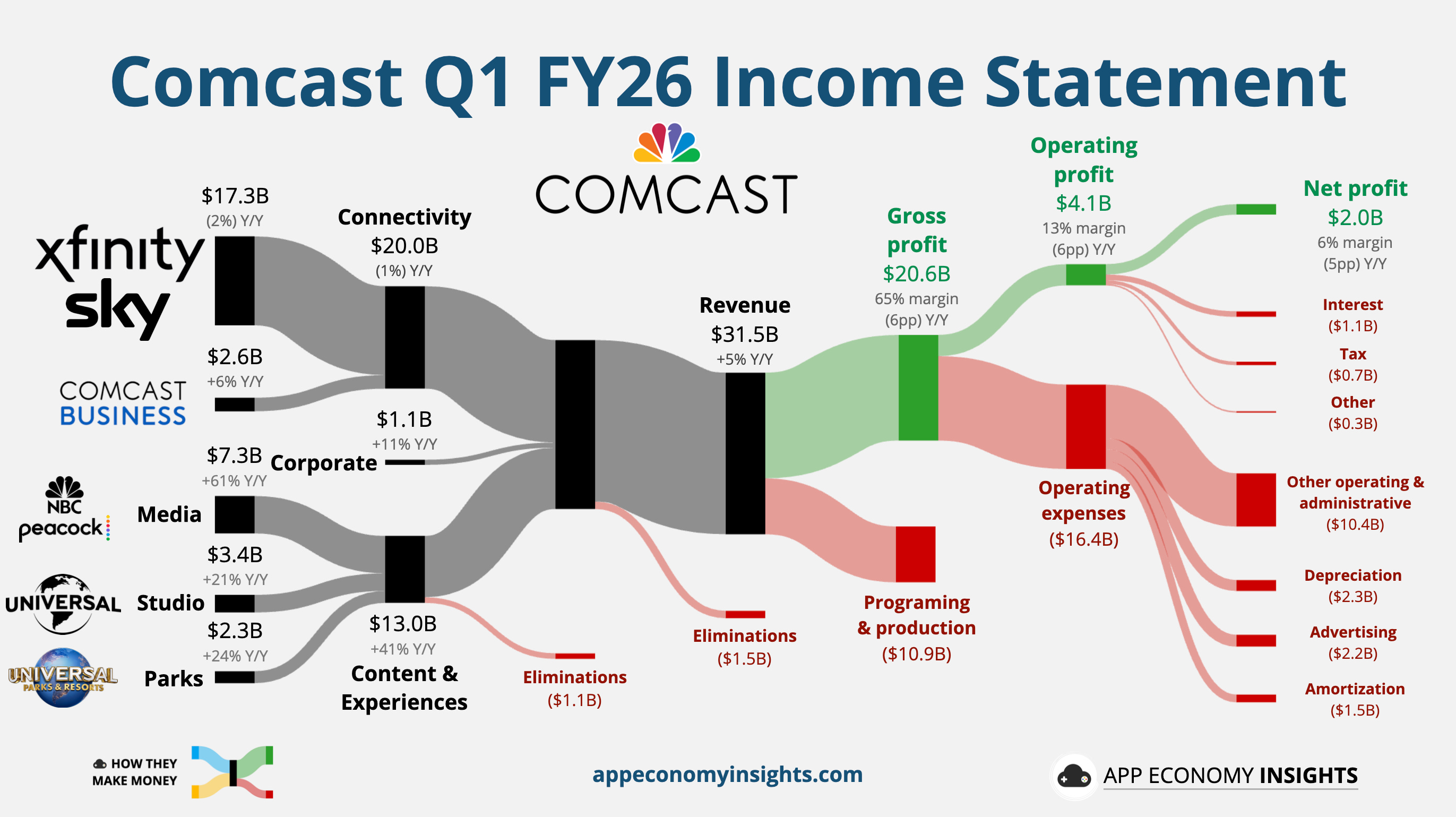

Q1 made the logic obvious:

Connectivity delclined 1% Y/Y to $20.0 billion, a slow, dependable annuity now under siege from fixed-wireless home internet and Starlink.

Content & Experiences grew +41% Y/Y to $13.0 billion, but only because NBC aired both Super Bowl LX and the Winter Olympics in February. Media revenue spiked +61% Y/Y on events that don't recur next quarter.

One business is a flat-growth utility throwing off free cash flow. The other is a lumpy, hit-driven content engine. Bundling them blurred the story for two very different investor bases, which is exactly the rationale Comcast now cites. After years of insisting the businesses belonged together, Cavanagh told analysts, “(we) simply changed our mind.”

The real story is M&A

Management swears it isn’t about future M&A. Roberts called the split “absolutely not” a prelude to deals. Wall Street seems unconvinced. Some analysts argued the separation matters less than what it enables: two focused companies, each with its own equity currency and board, free to pursue transactions that were unthinkable inside the conglomerate. It’s a way to unlock value and a clear ramp to dealmaking.

Wells Fargo pegs the sum-of-the-parts valuation at ~$25 per share, barely above today's price, and says the upside requires a transaction. A standalone NBCUniversal could use its own stock to buy content and reach the scale to fight Netflix and Disney. Or it might become a target itself.

Bottom Line: Comcast just conceded the conglomerate logic of the last decade is dead. The split should sharpen both businesses, but the market is already pricing the sequel. A leaner NBCUniversal, Sky in tow, becomes either the sector's next buyer or its next target the moment the ink dries.

👟 Nike: Not a Recovery Yet

Nike’s fourth quarter initially looked like a breakout. Reported EPS jumped more than 5x to $0.72. But the quarter included a $986 million tariff recovery tied to the International Emergency Economic Powers Act, which added roughly 900 basis points to gross margin. Adjusted for that one-time boost, EPS was closer to $0.20, a modest beat against the $0.13 consensus rather than the blowout the headline suggested.

The business underneath kept shrinking. Revenue fell 1% to $11.0 billion in the May quarter ($120 million beat) and dropped 4% in constant currency, nearly two years into Nike’s turnaround.

The margin mirage

Reported gross margin hit 49% (+9pp Y/Y), one of the highest in Nike's history, but ~9pp of that was the tariff refund. Underlying gross margin was ~40%, essentially flat and still near the lows of the reset.

Wholesale rose 4% to $6.6 billion.

NIKE Direct fell 7% to $4.1 billion, with Nike Brand Digital down 12%.

The trade kept margins compressed and shrank Nike's own channels, but it did help push North America back to growth.

What’s actually working

North America grew 3% to $4.8 billion, with wholesale up 10% as Nike rebuilt the retail relationships it spent years walking away from. Nike Running notched its fifth straight quarter of double-digit growth, adding roughly $1 billion to the category and five points of market share across North America and Western Europe. That was the clearest proof that Hill’s “Sport Offense” (the reorg that moved 8,000 employees into sport-specific teams) could create growth. The progress was real but uneven. A Boston Marathon ad got pulled after backlash, and some World Cup stock missed its retail delivery window.

International was still the drag:

Greater China: Sales fell 12% Y/Y to $1.3 billion (down 17% in constant currency), with segment profit down 20%. Results beat lowered expectations, but local brands like Anta and Li-Ning continued to take share. The "comprehensive reset" Hill is running is expected to weigh on results through FY27.

EMEA: Revenue slipped 1% Y/Y to $3.0 billion, but down 6% in constant currency, so the underlying business is losing even more momentum.

APLA: Roughly flat at $1.6 billion, up 1% Y/Y reported and down 1% in constant currency.

Converse: time to call it?

Revenue plunged 32% Y/Y to just $244 million, and full-year sales were the lowest since 2011. Neil Saunders of GlobalData suggested that if Nike couldn't or wouldn't fix the brand, it should weigh an exit before Converse became a drain on management's attention. Hard to argue.

Soft outlook with a parting warning

Nike expected Q1 FY27 revenue to be down low-to-mid single digits and earnings roughly flat through Q2 FY27 (excluding the tariff benefit), though gross margin should finally start expanding as early as Q1.

Outgoing CFO Matt Friend was blunt: "We are not expecting the environment to improve meaningfully over the next six months." He warned that Nike's customers were under pressure worldwide. Friend will hand the reins to David Denton, Pfizer's CFO, on August 17. A fresh set of eyes, arriving at an awkward moment.

Bottom Line: Nike's profit surge was a one-time tariff windfall. The stock has fallen more than 30% this year, on track for a fifth straight annual decline. That said, North America and Running are the first hard evidence that the reset can produce real growth after months of inventory cleanup. At ~28x forward earnings, this is still a "show me" story, and the real test comes at November's investor day.

That's it for today.

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own AAPL, GOOG, META, NVDA, and TSLA in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.