🧠 Cerebras: Demand Is Not the Problem

A record semiconductor IPO meets data-center reality

Welcome to the Premium edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Cerebras pulled off the biggest semiconductor IPO

The May 2026 IPO priced at $185, surged to $386 on opening day, and closed at $311, a 68% pop.

That was the high-water mark. The stock spent the next six weeks giving back most of its gains, and its first earnings report triggered a record two-day plunge that briefly pushed it below the IPO price.

If that round-trip feels familiar, it’s the pattern we walked through in How To Invest in IPOs. The day-one pop is often short-lived, and the first earnings call is where the hype meets reality.

The quarter itself was impressive. Revenue nearly doubled, Cerebras beat expectations, and management raised full-year guidance above consensus.

The problem was not demand. It was the cost of keeping up with it.

Management argues the market misunderstood the softer margin outlook, which is partly due to Cerebras renting back its own chips from a customer while it waits for new data centers to come online.

Let’s review what we learned.

Today at a glance:

🧠 How Cerebras makes money

📊 Q1 FY26 by the numbers

🎙️ Key insights from the call

🔭 What to watch next

FROM OUR PARTNERS

The $7.1 Trillion Flowing Into AI is Not What You Think

When McKinsey & Company projects $7.1 trillion in AI investment by 2030, it’s not meant just for names like OpenAI, Anthropic, and Google.

Investors want to know the new movers in this industry. That’s why they’re looking at companies like BluSky AI.

These companies are building the infrastructure layer of the AI future. And their tech is only getting more important with time as demand for AI compute power outruns supply.

While typical data centers take several years to build, BluSky AI deploys modular, AI-ready data centers in months. BluSky AI utilizes less power, little to no water, and minimizes the impact on local communities.

Startups, enterprises, and governments will depend on tech like this. BluSky AI has a robust portfolio of unique sites with negotiated power ready for deployment. Become an early-stage investor in BlueSky AI today.

This is a paid advertisement for BluSky AI Regulation A offering. Please read the offering circular at https://invest.bluskyaidatacenters.com/

🧠 How Cerebras makes money

We’ve not covered Cerebras before in this newsletter, so let’s go back to basics.

A typical AI processor is roughly the size of a postage stamp. Cerebras builds one the size of a dinner plate: an entire silicon wafer turned into a single chip. Its Wafer-Scale Engine packs ~4 trillion transistors, against ~200 billion on NVIDIA's flagship Blackwell. Cerebras sells it inside a single machine, the CS-3, rather than as a bare chip.

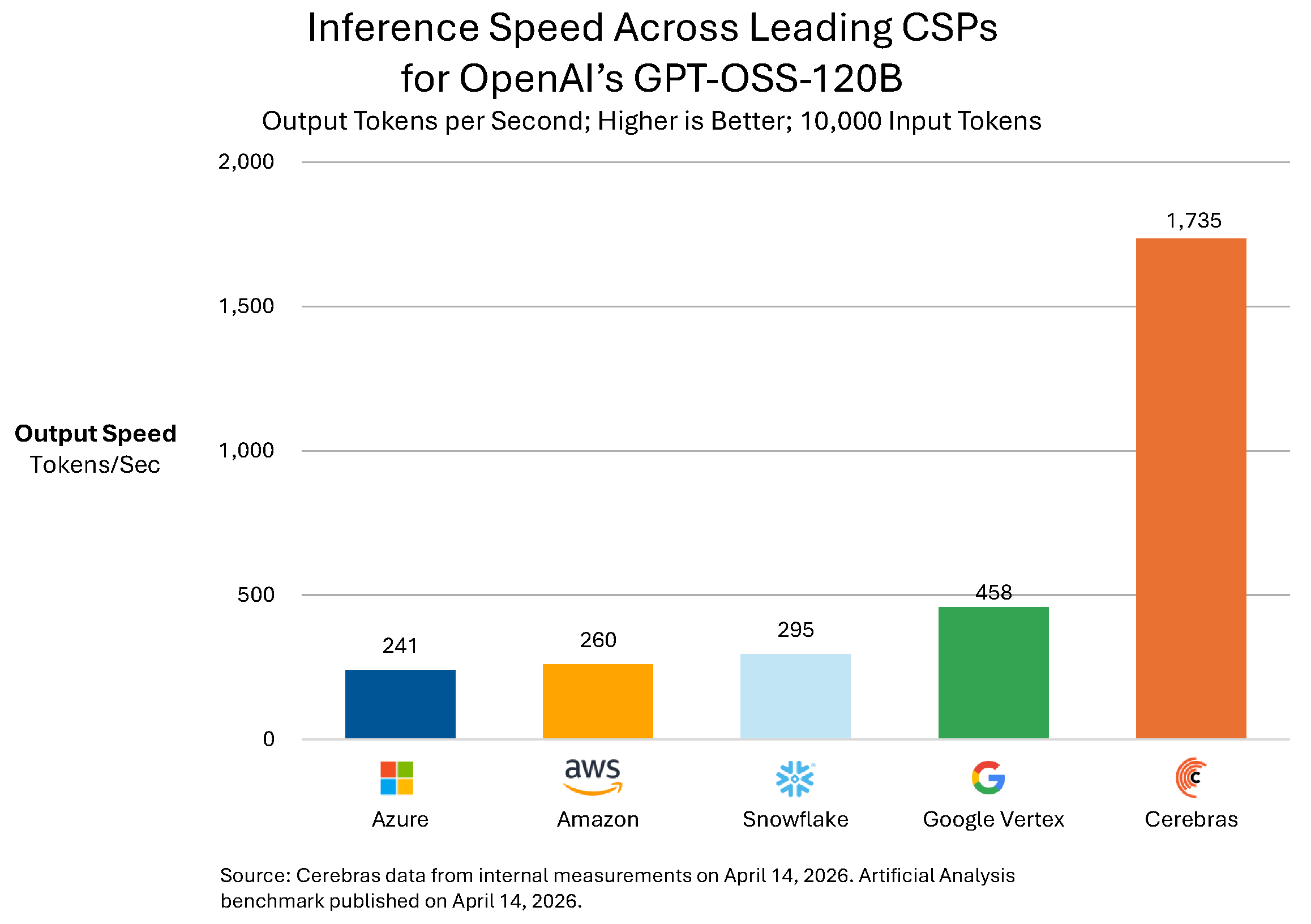

The point of all that silicon is speed. Keeping a model on one giant chip avoids the slow shuffle of data between thousands of smaller ones, which lets Cerebras generate tokens roughly an order of magnitude faster than a GPU cluster. On frontier models, it clears 1,000 tokens per second. The pitch is simple: fast AI is worth a premium because it gets more done.

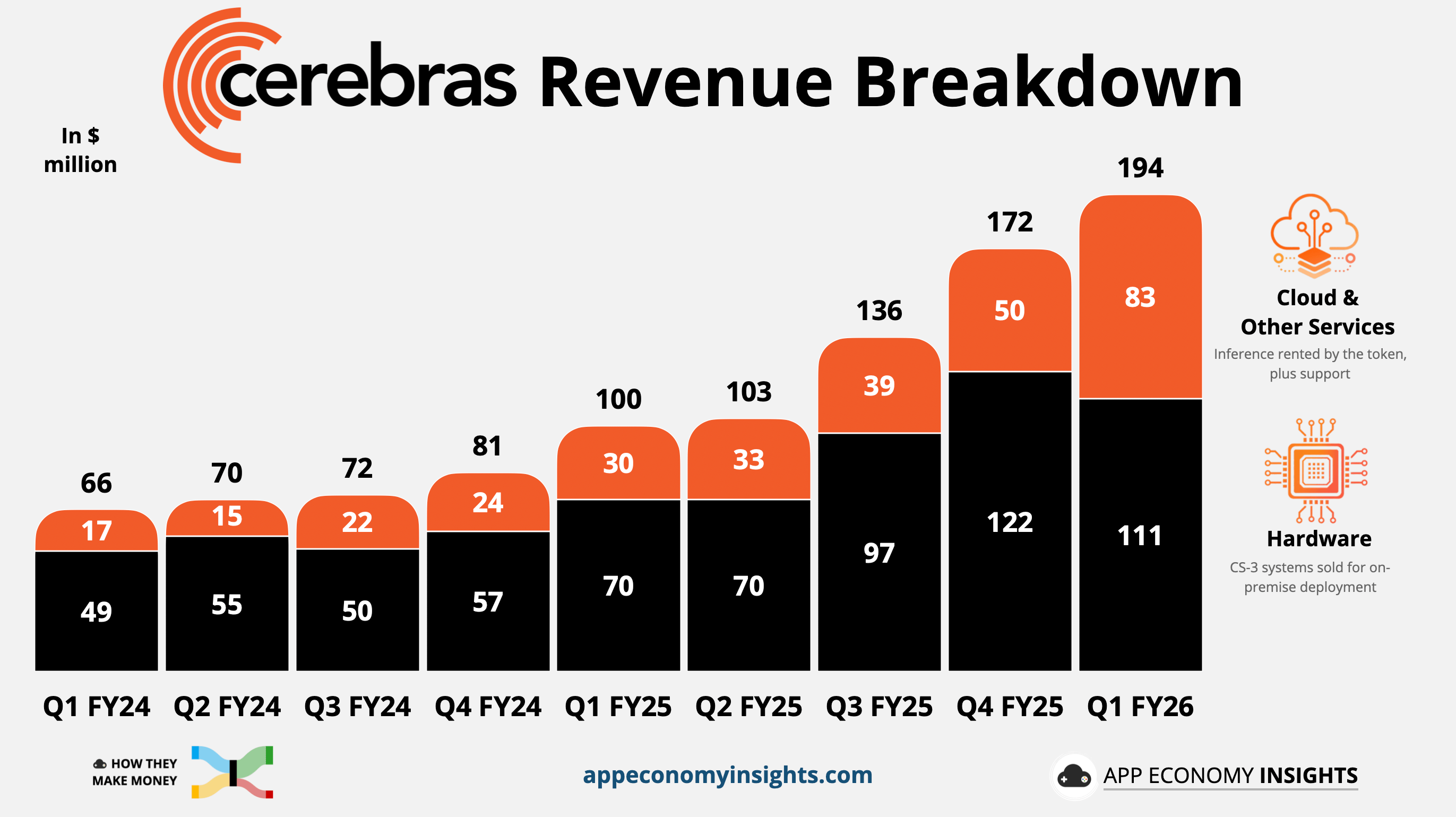

Cerebras turns that into two revenue streams.

Hardware: Ceberas sells CS-3 systems and clusters to customers who run them in their own data centers. This segment was $111 million in Q1 FY26 (+59% Y/Y), and it’s the legacy side of the business.

Cloud & other services: Customers can rent that same inference horsepower by the token from Cerebras-operated data centers. This segment hit $83 million (+178% Y/Y), growing three times faster than hardware and the strategic center of gravity going forward.

The moat is where it gets interesting. Cerebras sidesteps the exact chokepoints throttling everyone else. It uses no high-bandwidth memory (HBM), no CoWoS advanced packaging, and no bleeding-edge 3nm process, leaning instead on plentiful SRAM and mature 5nm. While the industry fights over the same scarce TSMC and HBM allocation, Cerebras isn’t standing in that line, and it’s the only AI accelerator maker building its systems entirely in the US.

The catch is who’s been paying. Cerebras was, until recently, almost entirely dependent on G42, an Abu Dhabi AI group. Its risk disclosures now name four significant customers: OpenAI, G42, MBZUAI University, and AWS. The bull case rests on the first and last names on that list, turning a UAE-heavy customer base into broader Western enterprise demand.

One quirk of the OpenAI deal shapes the numbers throughout, so it’s worth understanding up front:

The deal: A multi-year agreement for more than $20 billion of Cerebras compute.

The twist: To win it, Cerebras also handed OpenAI warrants (the right to buy its stock at a discount).

The accounting: Those warrants count as a discount, so part of what OpenAI pays never shows up as revenue.

The upshot: The reported figure understates the true size of the OpenAI business, and that gap widens as the deal ramps.