🐉 Alibaba: The AI Trade-Off

Spending big to accelerate growth

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

You have to spend money to make money

This week, Alibaba and Sea Limited reminded investors what that looks like.

Both missed profit expectations. Both stocks rallied anyway.

That’s the paradox of an investment cycle. The income statement gets worse before the underlying business gets better. Alibaba is pouring money into AI infrastructure. Sea is spending to widen its e-commerce moat.

To be sure, the bar was very low. After all, these two stocks have been down in the past five years, while the S&P 500 has nearly doubled.

But investors may forgive ugly earnings today if the spending creates better earnings tomorrow. The question is whether these companies are building moats or just burning cash.

Today at a glance:

🐉 Alibaba: The AI Trade-Off

🌊 Sea Limited: Moat Over Margins

🐉 Alibaba: The AI Trade-Off

Alibaba just delivered one of the strangest earnings reactions of the season.

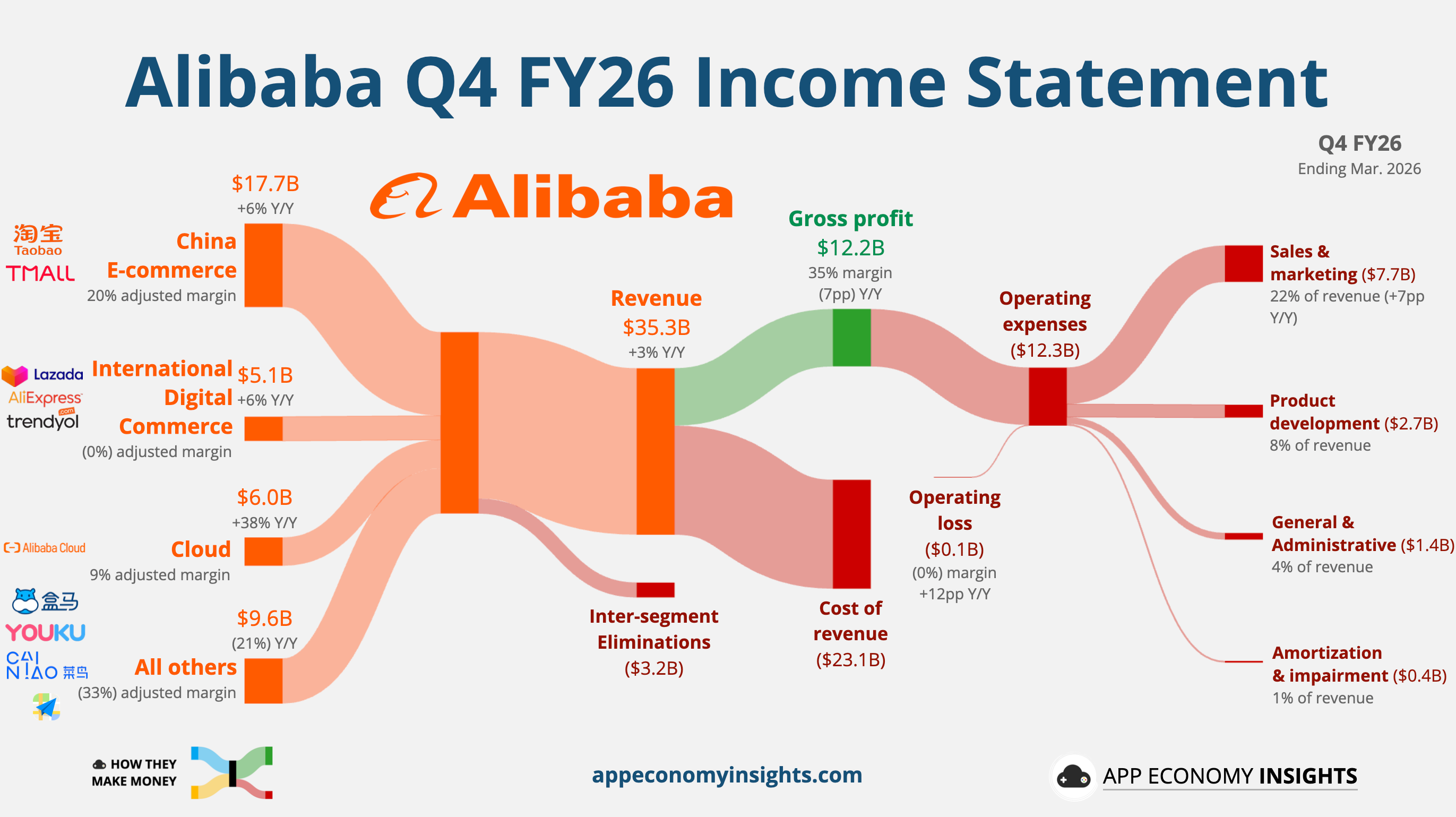

Revenue grew only 3% Y/Y to $35.3 billion ($1.1 billion miss), while adjusted EBITA fell 84% to $0.7 billion. The company turned to an operating loss for the first time in five years.

And yet, the stock jumped 8%. Why? Because investors looked past the income statement and focused on the AI trajectory.

CEO Eddie Wu said Alibaba’s AI work has moved from “incubation to commercialization at scale.” The company now expects to spend even more than its previous $52 billion three-year AI investment plan, with management prioritizing growth and market share over near-term margins.

In short, Alibaba traded profit for AI growth.

Income statement

Revenue breakdown:

🛒 China E-commerce: $17.7 billion, up 6%.

☁️ Cloud Intelligence: $6.0 billion, up 38%.

🌍 International commerce: $5.1 billion, up 6%.

🧩 All others: $9.6 billion, down 21%, distorted by disposals.

Excluding disposed businesses such as Sun Art and Intime, group revenue actually grew 11% Y/Y.

The main problem was profitability. Group operating margin turned slightly negative. Adjusted EBITA margin dropped to 2% from 14%. Sales and marketing expenses rose to 22% of revenue as Alibaba funded subsidies for quick commerce and user acquisition for the Qwen AI model family. Free cash flow swung to a $6.8 billion outflow as AI infrastructure spending ramped up.

Alibaba is no longer managing the business for clean quarterly margins. It is managing for a strategic position.

FY27 commentary

Management expects Cloud Intelligence’s external growth to keep accelerating beyond +40%. Annual recurring revenue from AI models and applications is expected to surpass 30 billion yuan (~$4.4 billion) by year-end. CapEx will rise from already elevated levels, as management warned of much higher-than-expected AI spending.

☁️ Cloud accelerates

Cloud Intelligence was the bright spot thanks to AI.

Revenue grew 38% Y/Y to $6 billion, while external cloud revenue accelerated to 40% growth. AI-related product revenue grew triple digits for the 11th consecutive quarter and now accounts for 30% of external cloud revenue. Alibaba expects that mix to exceed 50% within about a year.

That matters because Cloud is the business that can change Alibaba’s multiple. The core marketplace is mature, quick commerce is expensive, and international commerce remains competitive. But if Cloud keeps accelerating with AI demand, Alibaba starts to look less like a slow-growth e-commerce giant and more like China’s AI infrastructure champion.

Wu’s key point is that AI tokens are becoming a production input, not just another line in the IT budget. If companies use AI to run workflows, serve customers, build software, and automate operations, demand scales with business activity.

That is the bull case for Alibaba Cloud.

🛒 E-commerce is still paying the bill

China E-commerce reported revenue growth of 6% Y/Y, but the underlying marketplace looked healthier than the headline suggests.

Customer management revenue grew only 1% on paper, but that was distorted by an accounting change in how Alibaba records merchant subsidies. On a like-for-like basis, management says it grew 8%, though still increasingly supported by subsidies.

The pressure came from quick commerce. Taobao Instant Commerce is Alibaba’s push into food, grocery, and local delivery. It gives Alibaba another way to increase frequency and defend the customer relationship against Meituan, JD.com, PDD, and Douyin.

But it is expensive. China E-commerce adjusted EBITA fell sharply as Alibaba subsidized users and merchants. Management says the unit economics are improving and expects quick commerce to turn profitable on a per-order basis by FY27.

So the e-commerce story is a trade-off: Alibaba is using today’s profits to defend tomorrow’s traffic.

🤖 Qwen is the consumer AI swing

The most interesting long-term move is Qwen.

Alibaba is integrating Qwen into its broader ecosystem, including e-commerce experiences such as shopping assistance. That gives Alibaba something most AI companies would love to have: distribution.

A standalone chatbot has to acquire users from scratch. Alibaba can put Qwen in front of hundreds of millions of shoppers, merchants, and cloud customers.

That does not guarantee adoption. Consumer AI habits are still forming, and ByteDance, Tencent, Baidu, and other Chinese platforms are all fighting for the same user behavior.

But the strategic logic is clear: Alibaba wants AI to connect the full stack:

Models through Qwen.

Infrastructure through Alibaba Cloud.

Applications through shopping, merchant tools, and enterprise agents.

Distribution through Taobao and Tmall.

That is why investors were willing to look past the profit collapse. Alibaba is trying to prove it can be more than China’s e-commerce incumbent. It wants to be one of China’s core AI platforms.

Bottom Line: Alibaba traded a quarter of profit for a quarter of AI growth. The 84% EBITA decline was ugly, but the 40% external cloud growth was the signal investors cared about. Eddie Wu is telling the market that margins are secondary to building China’s AI stack. That can work if Cloud growth keeps accelerating and quick commerce losses narrow. But the spending has to translate into durable AI revenue, not just a bigger CapEx bill.

🌊 Sea Limited: Moat Over Margins

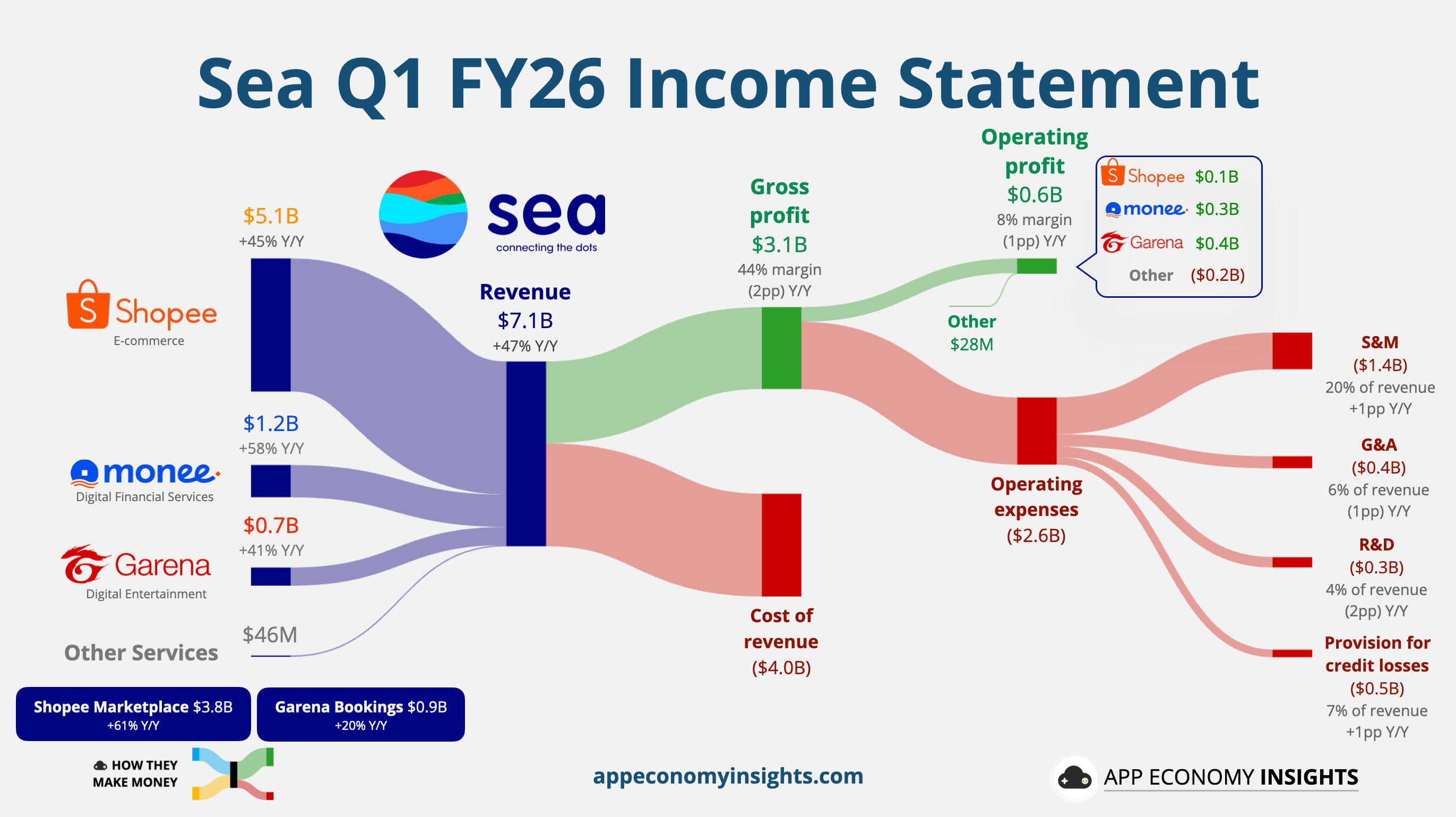

Sea Limited just delivered an impressive Q1, with the top line topping even the Q4 record, despite a quarter typically weaker seasonally.

Revenue grew +47% Y/Y to $7.1 billion, its fastest pace in years, while operating income rose just 30% to $0.6 billion. That gap tells the story: Sea is leaning back into investment mode.

CEO Forrest Li called 2026 a year to “deepen our competitive moats.” Translation: Sea is spending to widen its lead in e-commerce, fintech, and gaming.

The market liked it. The stock jumped as much as 12% after the print, helped by low expectations following a 50% slide from its September high. Investors had grown worried about margin pressure and rising competition across Southeast Asian e-commerce. This quarter showed the trade-off clearly. Growth is accelerating, but profits are being reinvested.

Income statement

Revenue breakdown:

🛒 Shopee: $5.1 billion (+45% Y/Y).

💳 Monee: $1.2 billion (+58% Y/Y).

🎮 Garena: $697 million (+41% Y/Y).

Margins moved the other way:

Gross margin fell to 44%, down 2 points.

Operating margin fell to 8%, down 1 point.

Shopee adjusted EBITDA fell 16% despite record GMV.

FY26 guidance

Management reiterated Shopee GMV growth of ~25% Y/Y, with Shopee’s full-year adjusted EBITDA expected to at least match 2025 in absolute dollar terms.

🛒 Shopee is buying scale

Shopee remains Sea’s engine and burden.

GMV reached a record $37.3 billion, up 30% Y/Y, while gross orders rose 29% to 4.0 billion. Core marketplace revenue, including transaction fees and advertising, surged 61% to $3.8 billion.

That’s the good news: Shopee’s take rate is improving.

The bad news: cost of revenue rose 55% as Sea poured money into logistics and instant delivery. Shopee’s adjusted EBITDA fell to $223 million from $264 million a year ago.

This is the Amazon playbook we are all familiar with. Sacrifice near-term margin to build infrastructure that competitors struggle to match. TikTok Shop and Temu can compete on price. But a regional fulfillment network is harder to replicate.

Management still targets a long-term 2%-3% e-commerce EBITDA margin. For now, Sea appears willing to let margins compress if it means strengthening Shopee’s logistics moat.

💳 Monee is becoming a real bank

Monee, formerly SeaMoney, is no longer a side hustle.

The loan book jumped 71% to $9.9 billion, the main driver of revenue growth for this segment. Non-performing loans past 90 days remained flat at 1.1%, a reassuring sign for now.

That matters because Monee has better unit economics than e-commerce, but also more downside if credit quality cracks. Sea is increasingly a marketplace, a gaming company, and a lender, all in one.

The opportunity is powerful. Shopee gives Sea transaction data that most banks never see. That can improve underwriting and deepen customer relationships. But the credit cycle has not been fully tested at this scale.

🎮 Garena is still funding the empire

Garena delivered its best quarter since 2021. Bookings grew 20% Y/Y to $931 million, and adjusted EBITDA rose 25% to $574 million. Bookings represent the money spent by users during the quarter, which is recognized into revenue over time. It’s the representation of the business momentum.

The surprise is that Garena is not growing by adding many new users. Quarterly active users were roughly flat at 667 million. Instead, paying users grew 12%, and average bookings per user increased.

In plain English: the funnel is mature, but monetization is improving.

Free Fire remains the workhorse, supported by strong live events and partnerships. Garena was once written off as a fading one-hit business. Now it is back to doing what it did during Sea’s first growth wave: generating the cash that funds everything else.

Sea is becoming a three-engine compounder:

Shopee is building the logistics moat.

Monee is monetizing the user base through credit.

Garena is funding the reinvestment cycle.

The bull case is that these three engines reinforce each other. Shopee acquires the users, Monee deepens monetization, and Garena provides high-margin cash flow.

The bear case is just as clear: TikTok Shop, Lazada, and Temu are not going away. Credit risk and logistics costs could pressure margins for longer than investors expect.

Bottom Line: Sea is buying growth again, but this time from a stronger position. Q1 delivered record revenue, record GMV, record adjusted EBITDA, and a cleaner three-engine story than Sea has had since 2021. The next test is whether Shopee’s logistics spend turns into operating leverage and whether Monee’s fast-growing loan book holds up at scale. For now, Sea is choosing moat over margin. That can be a winning strategy, but only if the moat hardens before the bill gets too large.

📊 Stay tuned for our PRO coverage tomorrow, including Tencent, Cisco, Nubank, Figma, and more

That’s it for today!

Stay healthy and invest on!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Start an account for free and save 15% on paid plans with this link.

Disclosure: I own BABA, NU, SE, and TCEHY in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.