🎮 The AI Tax on Gaming

What happens when AI raises your costs but not your multiple?

Welcome to the Premium edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Are gaming giants missing an AI story?

The market is punishing tech companies that can’t tell a grand AI story. Few examples are clearer than Sony and Nintendo, the world’s two top console makers, which reported earnings last Friday.

Sony’s stock is down 23% YTD. Nintendo is down ~50% over the past 12 months. Both are facing a memory crunch driven by AI demand for data centers. Both are raising console prices to defend margins.

Meanwhile, Alphabet, Amazon, Meta, and Microsoft can announce $100+ billion CapEx plans and watch investors come back after a brief selloff. Spending on AI infrastructure is treated as an expanding moat. Higher memory costs for consoles are just margin pressure with no upside.

That’s the strange setup for gaming in 2026.

Sony tried on the AI vocabulary this quarter, with physical AI and creator tools. Nintendo stayed quiet and focused on shipping games.

Both companies are executing well in their own ways.

But both are being valued like they’re missing the only story that matters.

Today at a glance:

🎮 Sony: Beyond PlayStation

🍄 Nintendo: The Price Test

FROM OUR PARTNERS

The Company Behind Meta's Top Productivity App Is Scaling Fast

Immersed has already reserved the NASDAQ ticker $IMRS. But the real opportunity for investors is now, before the company goes public.

They’ve developed the Meta Quest store’s most popular productivity app. More than 1.5M people, including Fortune 500 teams, use it up to 60 hours a week.

Rapid success has driven a 4,000% valuation surge for Immersed. But their next chapter could deliver an even bigger breakthrough…

Immersed’s soon-to-be-released Visor headset has 2M more pixels than Apple’s Vision Pro for 70% less money and 70% less weight. More than 75,000 people are already on the waitlist to receive it. No wonder they’re projecting 10x revenue growth from $7M to $71M in the first year alone.

With just 2 days left, this pre-IPO opportunity is closing soon. Lock in the $0.72 share price before the May 14th deadline.

This is a paid advertisement for Immersed Regulation A+ offering. Please read the offering circular at https://invest.immersed.com/

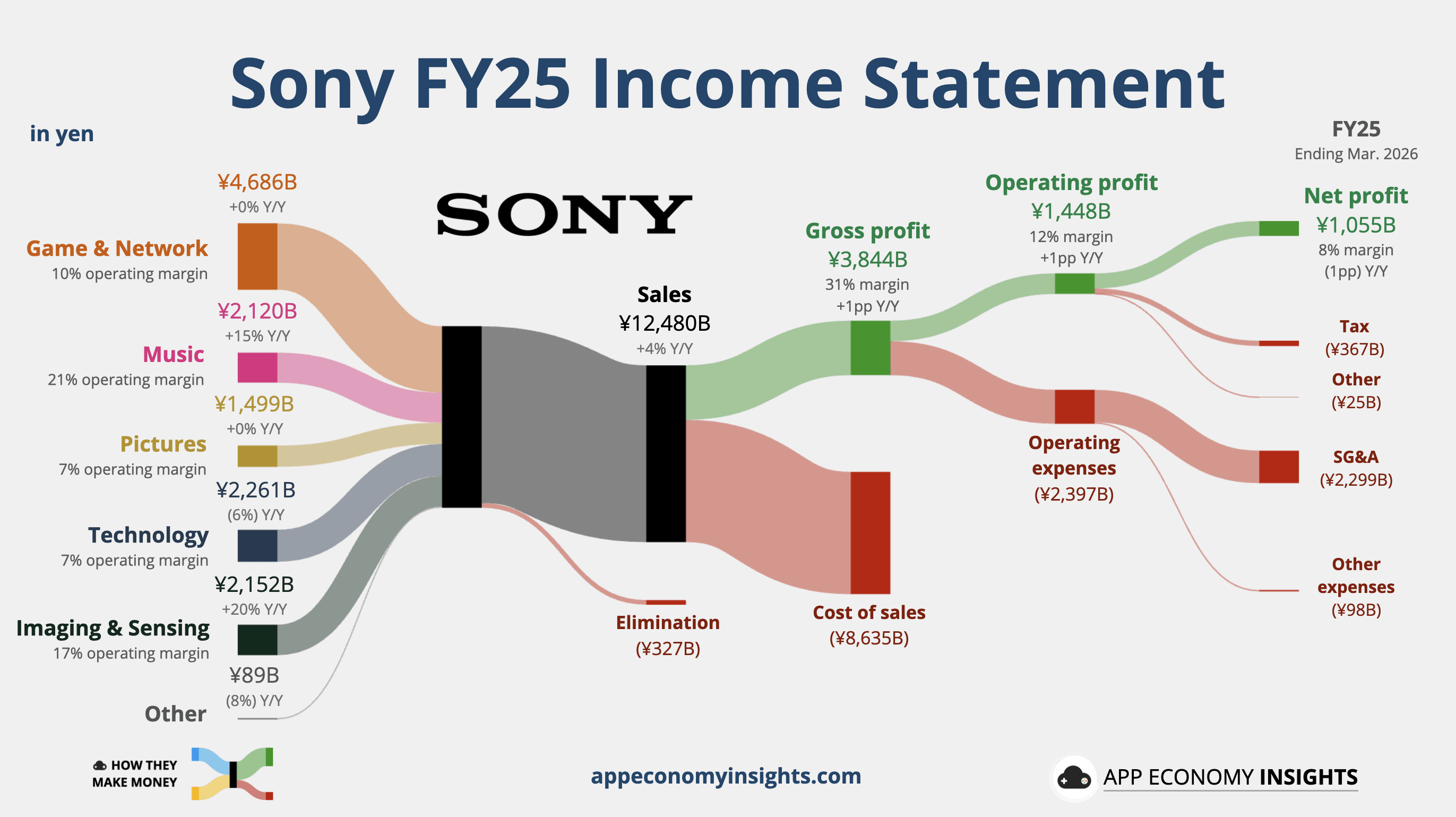

🎮 Sony: Beyond PlayStation

Sony just had its most profitable year ever. But the market focused on what comes next.

FY25 revenue (ending in March 2026) grew 4% Y/Y to ¥12.48 trillion (~$80 billion), while operating income rose 13% Y/Y to ¥1.45 trillion. Yet the March quarter was messy: net profit fell 63% Y/Y to ¥83 billion, far below consensus, dragged down by impairments at Bungie and Pixomondo plus a loss tied to the wound-down Honda EV venture.

The headline miss was ugly, but the underlying story is more interesting.

Sony is becoming a cleaner company: less hardware-heavy, more IP-driven, and more disciplined with capital. The new roadmap is built around gaming services, music catalogs, image sensors, and fab-light manufacturing.

👾 Gaming: Fewer consoles, better economics

The PS5 sold 1.5 million units in Q4, down from 2.8 million a year ago and the lowest quarter on record for the console. Lifetime shipments reached 93.7 million.

As a result, the revenue for the largest segment of the company was flat Y/Y. That sounds alarming, but the PlayStation business is healthier than the hardware numbers suggest.

Game & Network Services (G&NS) segment operating income fell 42% Y/Y to ¥54 billion in Q4, mainly because Sony booked an ¥88.6 billion Bungie impairment. The write-down reflects weaker future cash-flow expectations after softer engagement in Destiny 2 and delays around Marathon. Sony paid $3.6 billion for Bungie in 2022, making this a costly reminder that live-service games are harder to scale than they look. Strip out one-time charges, and full-year G&NS operating income would have grown 45% Y/Y instead of the reported 12%.

The gaming shift is clear:

Hardware is slowing.

Engagement is holding up.

Software and services are carrying more weight.

PSN monthly active users reached 125 million, up only 1% Y/Y, but still near record levels. Playtime grew along with the user base.

That is the key takeaway. Sony may sell fewer consoles late in the cycle, but the installed base remains deeply engaged. At this stage of the cycle, software it the profit center, while hardware is more of a distribution channel.

The FY26 guide confirms it: G&NS revenue is expected to decline 6% Y/Y, while operating income is expected to grow 30% Y/Y as the Bungie impairment rolls off. Hardware profitability is expected to be roughly flat. The growth comes from software, services, and lower costs.