📈 US Banks Ride the Storm

Trading and dealmaking rebound as CEOs grow more upbeat

Welcome to the Premium edition of How They Make Money.

Over 200,000 subscribers turn to us for business and investment insights.

In case you missed it:

📈 Wall Street rides the storm

After a rocky start to the year, America’s biggest banks bounced back in Q2 with strong trading gains and a welcome revival in dealmaking.

Volatility from tariff headlines boosted activity across markets, while a steadier macro outlook gave CEOs room to sound more upbeat. Credit provisions ticked higher, but consumer strength and rebounding pipelines suggest momentum may be turning.

Let’s break down the results.

Today at a glance:

The Big Picture

JPMorganChase: Soft Landing

BofA: Trading Keeps Delivering

Wells Fargo: Cap Lifted

Morgan Stanley: Still the Equity King

Goldman Sachs: Another Record Trade

Citigroup: Blowout Quarter

The Big Picture

Here’s an updated look at the largest US banks by market cap.

As a reminder, banks make money through two main revenue streams:

💵 Net Interest Income (NII): The difference between interest earned on loans (like mortgages) and interest paid to depositors (like savings accounts). It’s the primary source of income for many banks and depends on interest rates.

👔 Noninterest Income: The revenue from services unrelated to interest. It includes fees (like ATM charges), advisory services, and trading revenue. Banks relying more on noninterest income are less affected by interest rate changes.

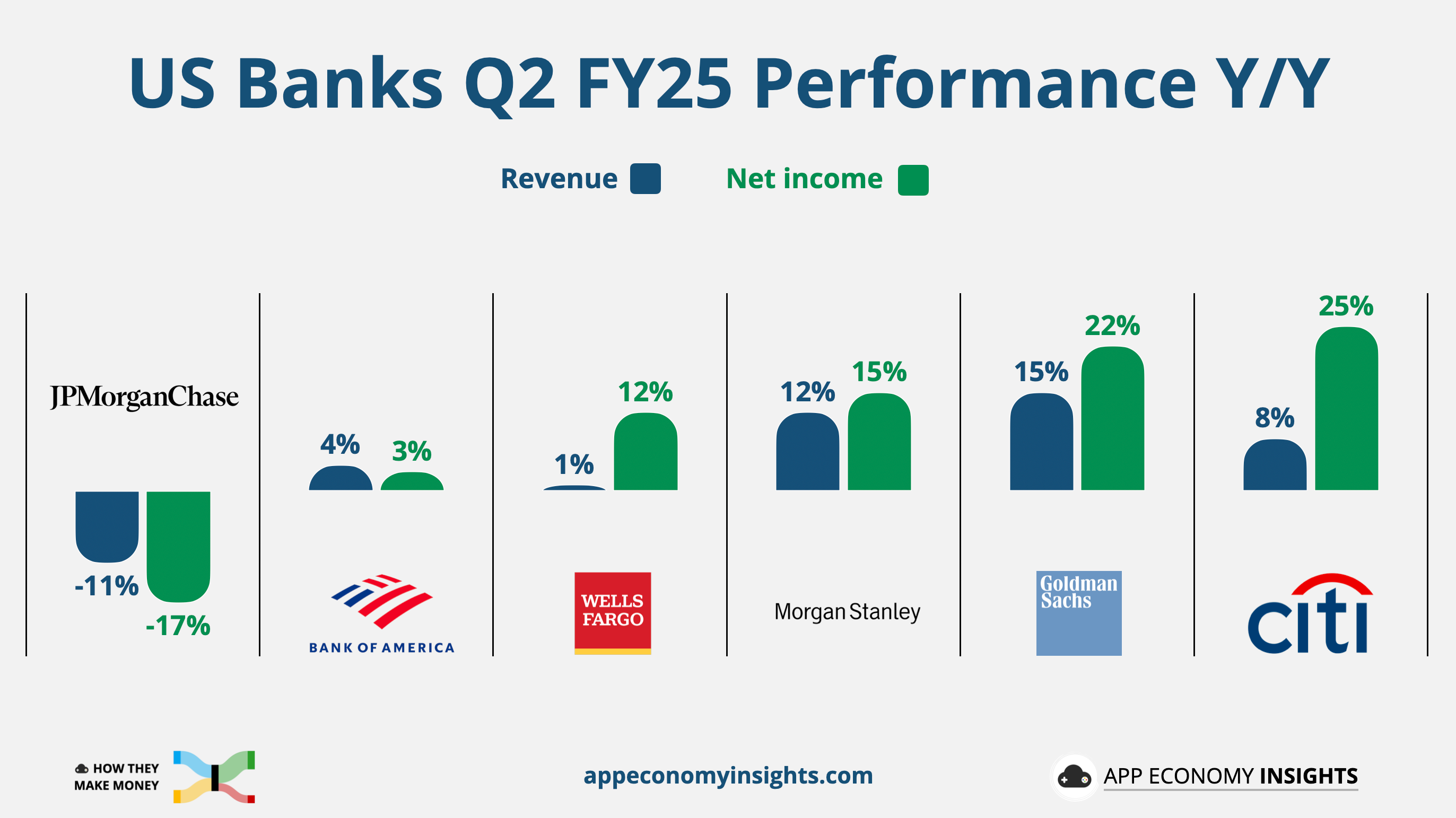

Here is the Q2 FY25 performance Y/Y at a glance.

Here are the significant developments in Q2 FY25:

📈 Trading bonanza: Goldman posted the best equity trading quarter in Wall Street history, while Morgan Stanley and Bank of America also hit near-record levels. Volatility from tariffs and rate speculation drove hedge fund activity and client repositioning, fuel for trading desks.

📊 Dealmaking gets off the mat: Investment banking revenue jumped across the board, with Citi and Goldman leading the rebound in M&A. Large deals are back on the table, and IPO pipelines are thawing. It’s early, but the drought may be ending.

🏦 Regulatory winds shift: With Wells Fargo’s asset cap lifted and capital requirements potentially easing, banks are regaining their swagger. Record buybacks, dividend hikes, and expansion into fee-based businesses are back in focus.

💳 Consumers hold steady, but provisions rise: Consumer spending is solid and delinquencies are stable, yet most banks padded reserves. Higher credit card balances and macro caution are pushing provisions upward, especially at Citi and Wells Fargo.

💰 Mixed NII outlooks: JPMorgan and Bank of America remain bullish on net interest income. But Wells Fargo pulled back, and others are cautious. Deposit costs and sluggish loan growth are squeezing margins even as rates stay high.

🧠 Tone shifts from anxious to upbeat: Last quarter brought recession fears. This quarter? Confidence. CEOs now talk about momentum, green shoots, and normalization. But they’re still watching for political curveballs.

🔑 Takeaway: Wall Street is back in rhythm. Trading and banking surged, consumers proved resilient, and regulatory pressure eased. But with provisions creeping up and tariff uncertainty, banks are moving forward, eyes wide open.

Let’s visualize them one by one and highlight the key points.

JPMorganChase: Soft Landing

Net revenue grew -11% Y/Y to $44.9 billion ($1.7 billion beat):

Net interest income (NII): $23.2 billion (+2% Y/Y).

Noninterest income: $21.7 billion (-21% Y/Y).

Net income: $15.0 billion (-17% Y/Y).

EPS: $4.96 ($0.48 beat).

Key developments:

📈 Guidance raised again: JPMorgan lifted its 2025 net interest income (NII) outlook to ~$95.5 billion ($1 billion raise), reflecting loan growth and pricing power, even as Q2 NII of $23.3 billion came in slightly below consensus.

📊 Markets shine: Markets revenue surged 15% Y/Y to $8.9 billion, with equities at a record $3.3 billion and fixed income up 14% to $5.7 billion. Investment banking fees rose 7%, defying expectations for a decline, as tariff fears eased and dealmaking picked up.

🛍️ Resilient consumers: Consumer & Community Banking net income jumped 23% Y/Y to $5.2 billion, with credit card spending up 7%. Card delinquencies edged down, and net charge-offs fell to 1.69%, easing prior concerns.

⚖️ Loan growth continues: Total loans reached $1.4 trillion (+7% Y/Y), with deposits at $2.6 trillion (+7% Y/Y). Provision for credit losses declined to $2.8 billion, including $2.4 billion in net charge-offs and a $439 million reserve build.

📉 Tough comp pollutes the analysis: The 11% Revenue decline was primarily due to last year’s one-time gains from the First Republic Bank acquisition. Net income fell 17% Y/Y, but EPS of $4.96 beat estimates by $0.48.

🧱 Strategic moves: JPMorgan formed a new Strategic Financing Solutions group, combining banking, markets, and sales to offer tailored capital solutions across public and private markets.

🔮 Economic backdrop: JPMorgan economists dropped their recession call, citing tariff delays and stronger-than-expected consumer health.

🔑 Takeaways: Despite declining headline numbers due to tough comps, JPMorgan delivered a confident quarter, with robust credit metrics, growing loan books, and strong trading activity. The upgraded outlook underscores its scale advantage.

Key quote: CEO Jamie Dimon: “We’ve basically been in this soft landing now for some time. It’s been resilient. Hopefully that will continue.”