🏦 SoFi: Full-Stack Fintech

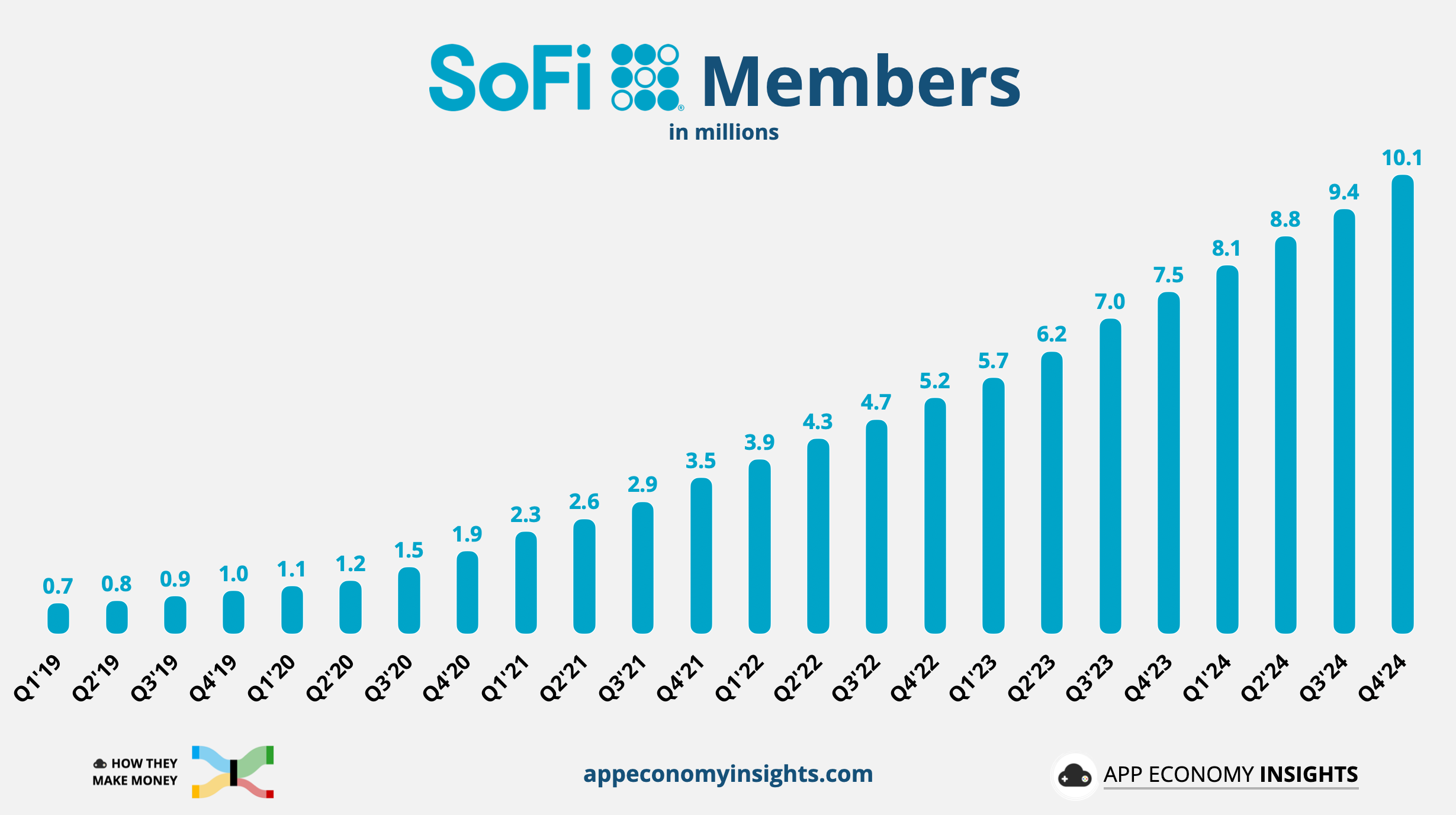

The neobank surpassed 10 million members

Welcome to the Premium edition of How They Make Money.

Over 180,000 subscribers turn to us for business and investment insights.

In case you missed it:

SoFi (SOFI) recently crossed 10 million members, up 10X in the past 5 years, solidifying its transformation into a full-stack fintech platform.

Following its volatile 2021 SPAC debut, SoFi's stock has more than doubled since September, fueled by consistent profitability, record deposit growth, and product expansion.

Despite Q4 results exceeding expectations, SoFi's stock dropped 10% after the earnings report on Monday. This was likely due to lower-than-expected 2025 profit guidance, as the company prioritizes long-term growth.

SoFi's 'financial super app' vision is materializing, but is the recent stock pullback a reality check or a temporary setback?

Today at a glance:

From student loans to full-stack fintech.

Why did the stock recently double?

How SoFi makes money.

Insights from the latest earnings call.

Is the rally sustainable?

1. From student loans to full-stack fintech

Disrupting Student Loans (2011-2017):

Founded in 2011, SoFi (short for Social Finance) initially disrupted the student loan market with alumni-funded refinancing, offering better rates than traditional banks. It quickly expanded into personal and mortgage loans, positioning itself as a digital-first, community-focused alternative.

Expanding Beyond Lending (2017-2020):

Starting in 2017, under CEO Anthony Noto (ex-Goldman Sachs partner, former Twitter COO), SoFi expanded beyond lending, launching SoFi Invest (commission-free trading) and SoFi Money (cash management). The 2020 acquisition of Galileo further expanded SoFi into B2B fintech infrastructure, powering other digital banks.

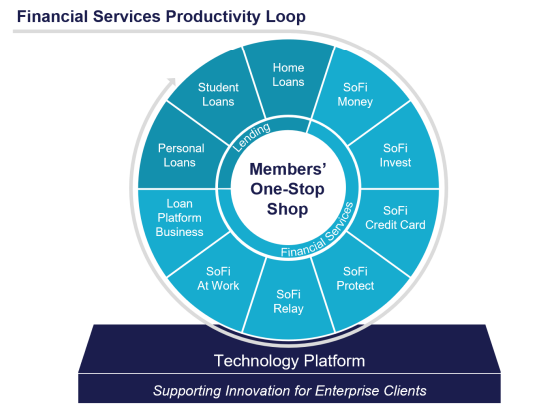

The Bank Charter and Super App Vision (2021-Present):

A game-changing moment came in 2022 when SoFi secured a national bank charter by acquiring Golden Pacific Bancorp. This allowed SoFi to hold deposits, reduce reliance on third-party banks, and improve lending margins—a structural advantage over most fintech peers.

At the same time, SoFi pursued its 'super app' strategy, integrating:

✅ Lending (student, personal, home loans).

✅ Banking (SoFi Money, SoFi Credit Card).

✅ Investing (trading, alternative assets).

✅ Tech Infrastructure (Galileo, Technisys).

The introduction of SoFi Plus, a premium membership tier, further enhanced user engagement and cross-selling. While lending remains a core revenue driver, the rapidly growing Financial Services and Tech Platform segments are on track to become the main revenue source. This dual-pronged strategy—direct-to-consumer finance and fintech infrastructure—has transformed SoFi from a niche lender into a financial powerhouse.