📊 PRO: This Week in Visuals

TSM ASML JNJ AXP BLK SCHW UAL

Welcome to the Saturday PRO edition of How They Make Money.

Over 200,000 subscribers turn to us for business and investment insights.

In case you missed it:

Premium subscribers get:

📊 Monthly reports: 200+ companies visualized.

📩 Tuesday articles: Exclusive deep dives and insights.

📚 Access to our archive: Hundreds of business breakdowns.

PRO subscribers get everything PLUS:

📩 Saturday PRO reports: Timely insights on the latest earnings.

Today at a glance:

⚙️ TSMC: Still Full Throttle on AI

🔬 ASML: Outlook Cools

💊 J&J: Guidance Climbs

🧬 Novartis: CFO Surprise Retirement

💳 American Express: Record Spending

🥤 PepsiCo: Searching for Sparkle

📈 Blackrock: $12.5 Trillion in AUM

🏦 Charles Schwab: Client Momentum

🛩️ United Airlines: Flying Through Turbulence

1. ⚙️ TSMC: Still Full Throttle on AI

Taiwan Semi’s Q2 revenue jumped 44% Y/Y to $30.1 billion, while net profit soared 61% to $12.8 billion, beating estimates thanks to expanding margins. High-Performance Computing (HPC), including AI accelerators, accounted for 60% of total revenue, up from 52% a year ago. Advanced nodes (3nm, 5nm, 7nm) made up 74% of wafer revenue, with 3nm alone rising to 24%, driven by demand from Apple, NVIDIA, and AMD.

Management raised FY25 revenue growth guidance from ~25% to ~30%, citing robust AI momentum and CoWoS capacity expansion (advanced packaging). Q3 revenue is expected at $32.4 billion, but unusually, Q4 is forecasted to decline sequentially, raising questions about tariff-related order pull-ins despite management's reassurances. TSMC is pressing ahead with its $38–42 billion Capex plan, accelerating US expansion in Arizona amid geopolitical uncertainty. No customer behavior changes have been observed, but caution remains around policy risk and currency headwinds.

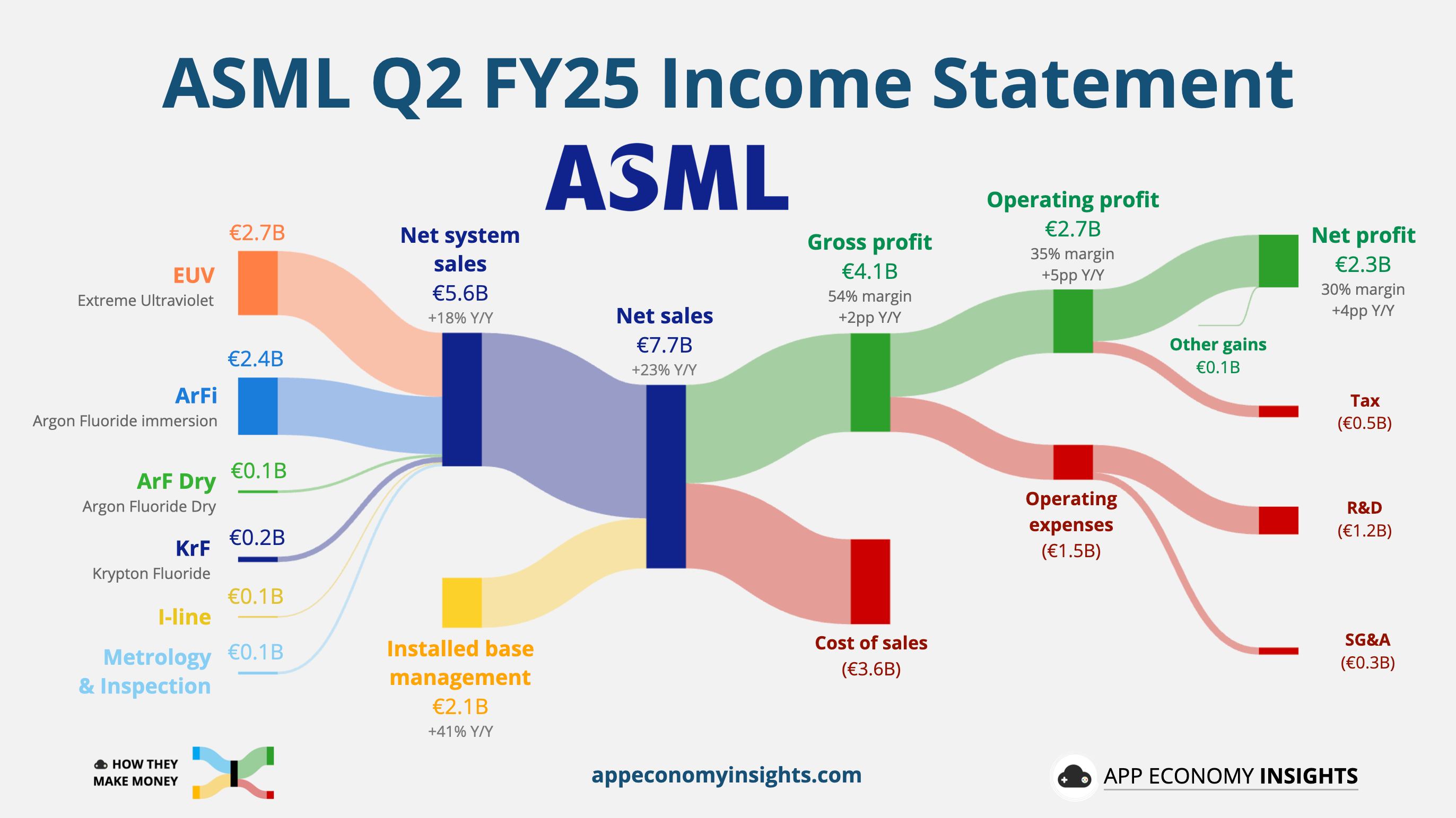

2. 🔬 ASML: Growth Doubts Loom

ASML, the largest European tech company, grew net sales 23% Y/Y to €7.7 billion (€200 million beat) and EPS was €5.90 (€0.75 beat). Bookings rebounded to €5.5 billion (€1.3 billion beat), including €2.3 billion in EUV orders. Gross margin held steady at 54%, helped by a High-NA system delivery (the most advanced machines) and upgrade mix.

Management reaffirmed full-year 2025 guidance for ~15% revenue growth and ~52% gross margin, but struck a more cautious tone on 2026. CEO Christophe Fouquet cited “increasing macro and geopolitical uncertainty,” warning that growth next year is no longer a given. Tariff concerns loom large, especially for US-bound shipments, imported materials, and potential retaliatory measures.

While AI-related demand remains strong—driving a projected 30% Y/Y jump in EUV sales—ASML’s visibility into customer spending has dimmed. China still represented 27% of system revenue, behind Taiwan at 35%. With rising external risks and a narrowed growth forecast, investor focus is shifting from EUV momentum to policy fallout. Most analysts remained bullish long-term after the call.