📊 PRO: This Week in Visuals

WMT ADI INTU NTES TGT TTWO WDAY ZM AS NIO

Welcome to the Saturday PRO edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Premium members get:

📊 Monthly reports: 200+ companies visualized.

📩 Tuesday articles: Exclusive deep dives and insights.

📚 Access to our archive: Hundreds of business breakdowns.

PRO members get everything PLUS:

📩 Saturday PRO reports: Timely insights on the latest earnings.

Today at a glance:

🛒 Walmart: Fuel Pressures the Flywheel

⚙️ Analog Devices: Cyclical Becomes Secular

✅ Intuit: Tax Season Stumble

🎮 NetEase: Live-Service Games Deliver

🎯 Target: Turnaround Finds Traction

🎮 Take-Two: GTA VI Date Locked

👔 Workday: Flex Credits Take Root

🖥️ Zoom: AI Companion Nearly Triples

⛷️ Amer Sports: Salomon Growth Inflection

⚡️ NIO: Margin Expansion Continues

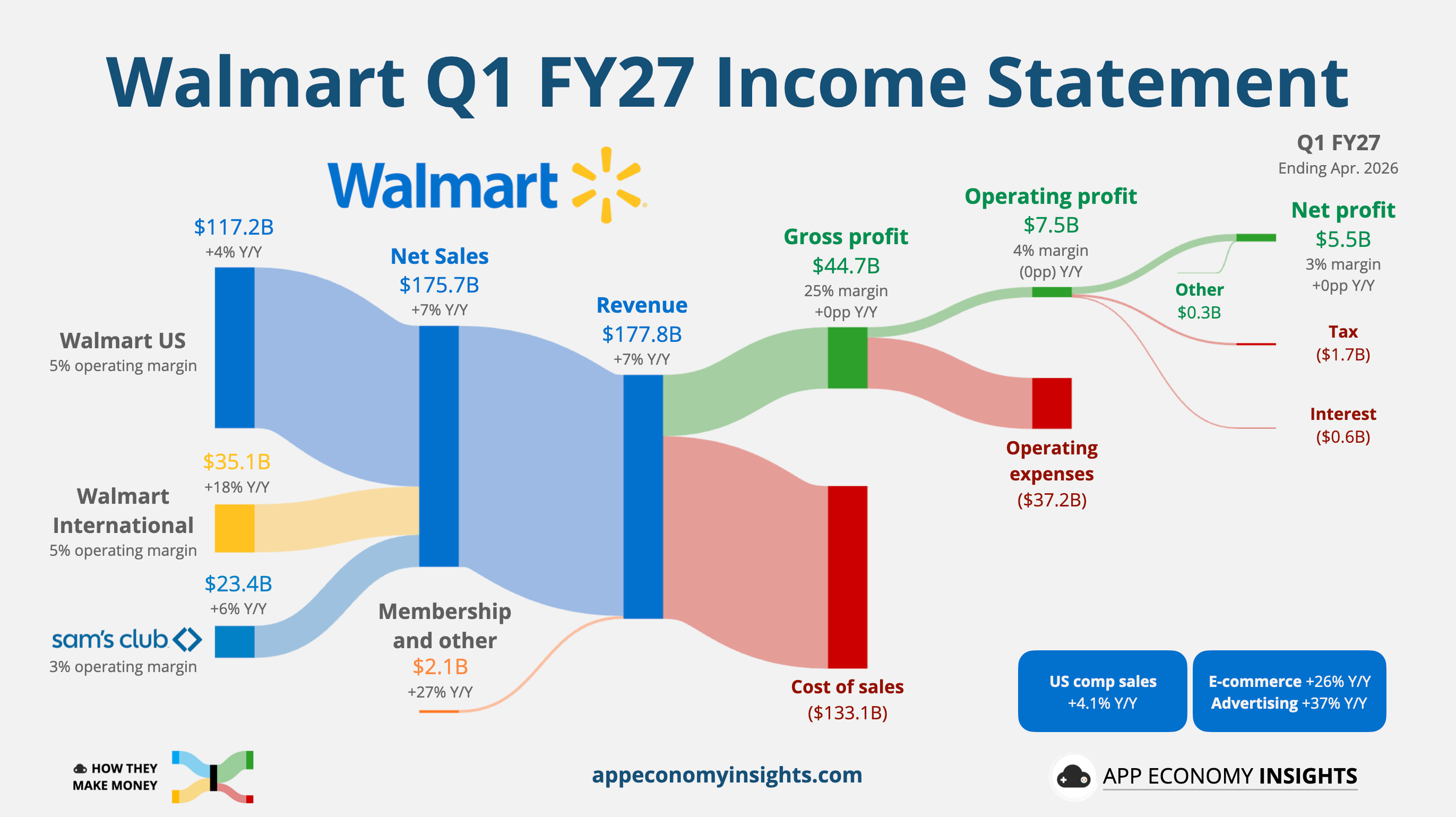

1. 🛒 Walmart: Fuel Pressures the Flywheel

Walmart reported its Q1 FY27 (April quarter), and revenue grew 7% Y/Y to $177.8 billion ($2.9 billion beat). Adjusted EPS was $0.66, in line with expectations. The operating margin contracted slightly due to higher fuel costs.

Walmart US comps rose 4.1%, slightly ahead of consensus, driven by a 3% increase in transactions and a 1.1% higher average ticket. Sam’s Club comps rose 3.9%, also ahead of expectations.

International sales jumped 18% to $35.1 billion, reflecting broad-based strength across key markets such as Walmex, China, and Flipkart in India, as well as continued e-commerce momentum. The segment is increasingly adopting the Walmart US playbook: more marketplace volume, more digital engagement, and more high-margin services layered on top of retail.

The steady shift toward digital continued:

Profit diversification: High-margin streams keep scaling. Global advertising grew 37%, Walmart US advertising grew 36%, while global membership fee revenue rose 17%. The broader “membership and other income” line grew faster, but it includes miscellaneous items beyond subscriptions. Commerce solutions, including ads, membership, and marketplace, now represent roughly one-third of operating income.

AI integration: Sparky, Walmart’s AI shopping assistant, saw weekly active users more than double sequentially. Customers using the tool have an average order value about 35% higher than non-users.

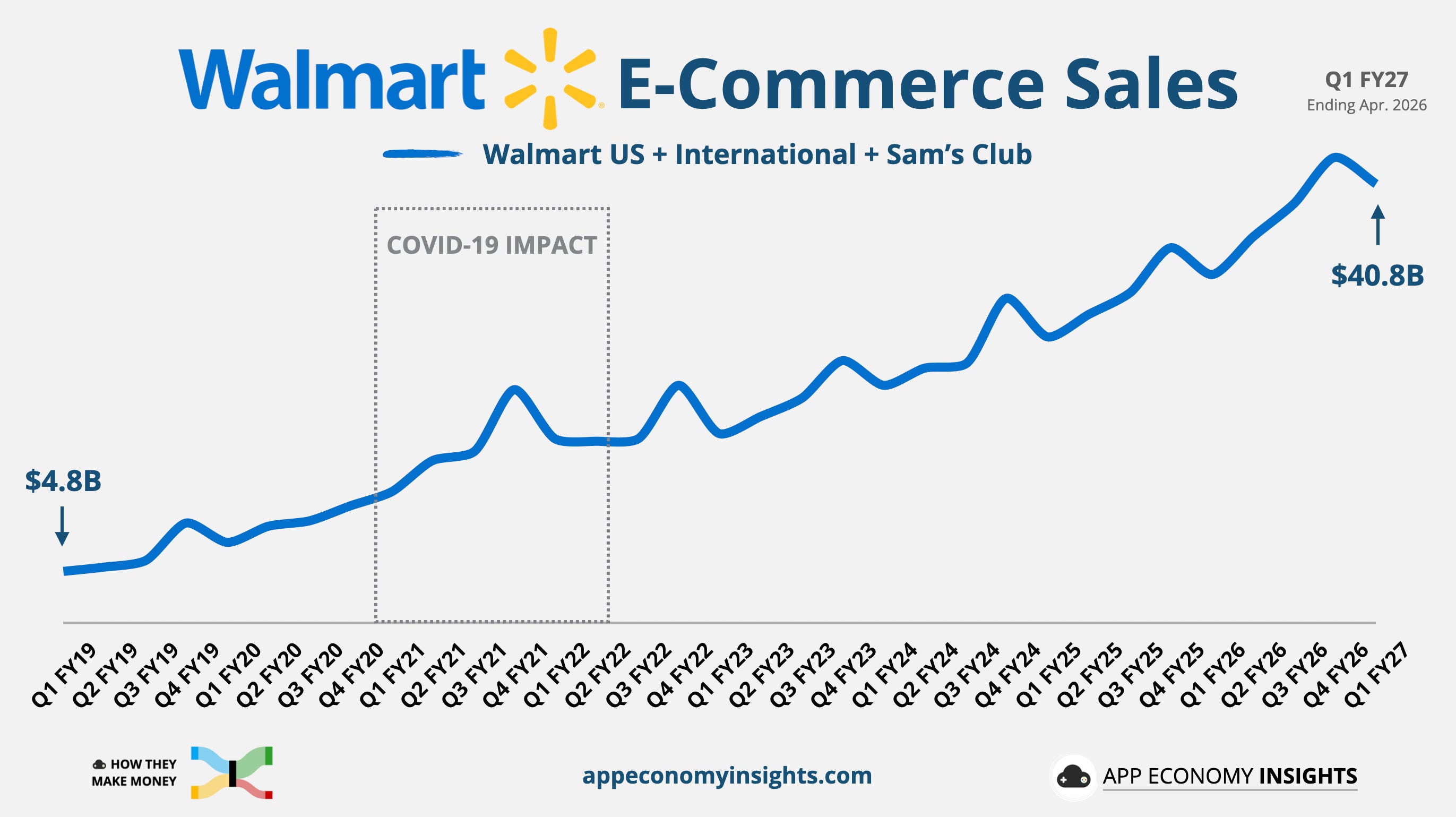

E-commerce momentum: Global e-commerce sales grew 26%, now representing nearly a quarter of total revenue. In the US, delivery grew 45%, marketplace sales rose nearly 50%, and Walmart can now reach 60% of the US population within 30 minutes.

The main pressure point was fuel. Walmart absorbed roughly $175 million in higher fuel costs during the quarter to keep prices competitive. Management noted that lower-income consumers are becoming more budget-conscious, with gas station customers buying less than 10 gallons per visit for the first time since 2022. If fuel prices stay elevated, Walmart may eventually need to raise prices.

Despite the sales beat, shares fell after guidance came in light:

Q2 adjusted EPS: ~$0.73 vs. $0.75 consensus.

FY27 adjusted EPS: ~$2.80 vs. $2.92 consensus.

Management still expects sales to trend toward the high end of its 3.5% to 4.5% annual growth range, with operating income growth improving through the year.

Walmart remains a share-gainer in a pressured consumer environment. Its value proposition is attracting shoppers, while e-commerce, ads, membership, and marketplace are improving the profit mix. But higher fuel costs are testing how much margin the company can protect while keeping prices low.