📊 PRO: This Week in Visuals

PEP DAL GIS

Welcome to the Saturday PRO edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Premium members get:

📊 Monthly reports: 200+ companies visualized.

📩 Tuesday articles: Exclusive deep dives and insights.

📚 Access to our archive: Hundreds of business breakdowns.

PRO members get everything PLUS:

📩 Saturday PRO reports: Timely insights on the latest earnings.

Today at a glance:

🥤 PepsiCo: Gas Prices Bite

🛩️ Delta: Premium Absorbs Fuel Shock

🍪 General Mills: Reinvestment Phase Ends

1. 🥤 PepsiCo: Gas Prices Bite

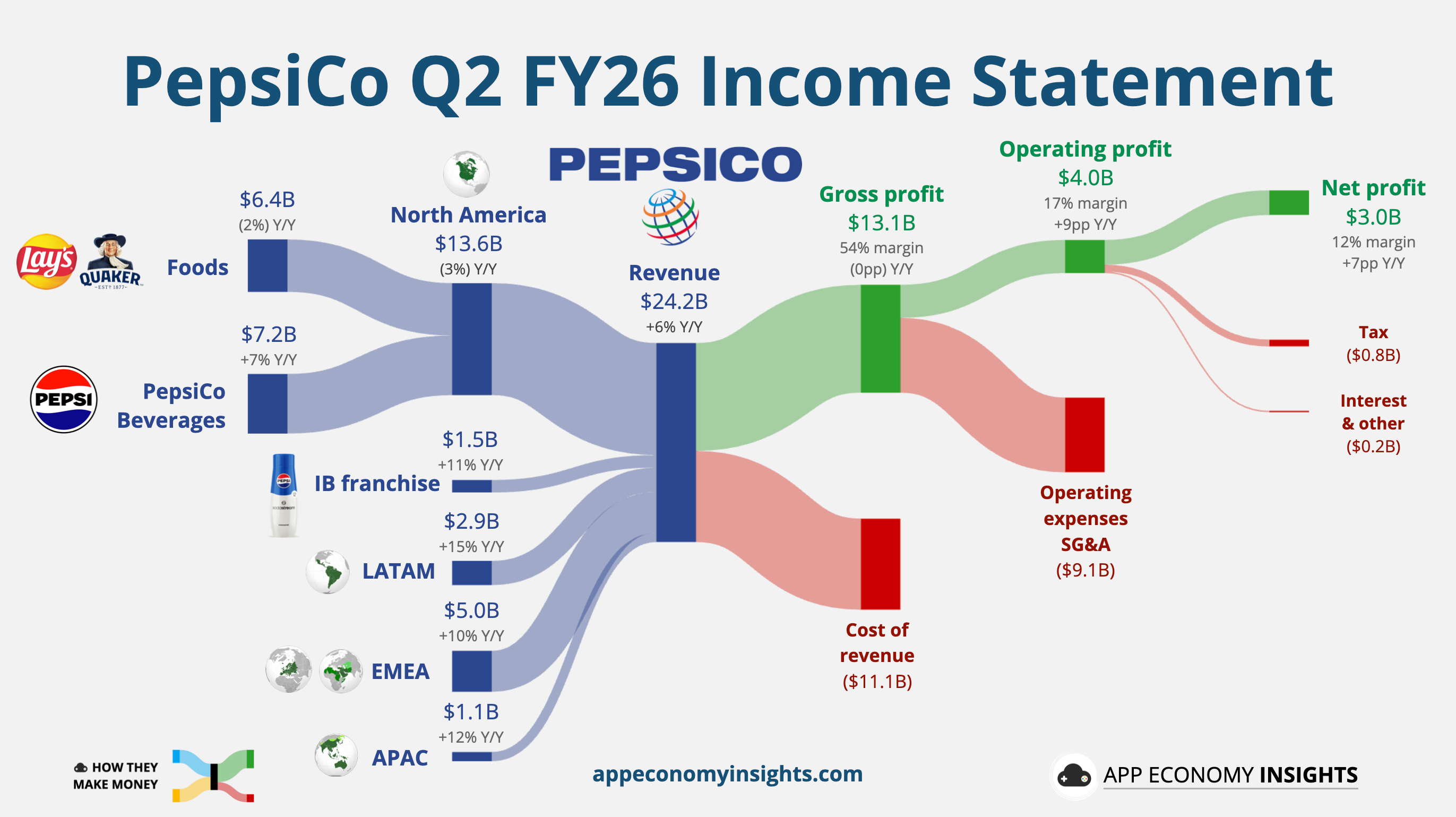

PepsiCo’s Q2 revenue rose 6% Y/Y to $24.2 billion ($230 million beat), with non-GAAP EPS of $2.20 ($0.01 miss). Organic revenue growth of 2.4% included effective net pricing plus modest volume gains, with FX adding 2.2 points and M&A 1.8 points. Shares fell by more than 3% anyway.

The North American segment disappointed after Q1’s tentative snack rebound:

Frito-Lay volume went flat, and revenue declined 2%, reversing the momentum from Q1’s 2% volume gain.

North American Beverages volume slid 4%, with operating margin down 90 bps.

International remained the engine, projected to top $40 billion in revenue this year, with Asia Pacific Foods delivering double-digit volume growth.

CEO Ramon Laguarta said, “The consumer is worse than what we had anticipated, and it’s driven mainly by gas prices.” US gas prices surged above $4/gallon during Q2 due to the Iran conflict, and Laguarta said the pullback was concentrated in convenience stores and other impulse-purchase channels. PepsiCo is now tweaking its 15% price cuts by segment and has noted delays in regaining the shelf space retailers had promised.

The healthier “permissible portfolio” (protein-fortified snacks, portion-controlled multipacks) hit $3 billion in value and is growing double digits, which Laguarta flagged as a bright spot. Activist Elliott’s pressure to accelerate the turnaround continues in the background.

PepsiCo reaffirmed full-year FY26 guidance, with organic revenue growth of 2–4% and core constant-currency EPS growth of 4–6%, though management flagged that results are likely to land at the low end of the EPS range. Tariff refunds will contribute roughly a full point of EPS growth to offset commodity inflation. The next question is whether the impulse channel recovers as gas prices ease, or whether Frito-Lay needs another pricing reset.