📊 PRO: This Week in Visuals

ORCL ADBE DOCU VAIL CHWY

Welcome to the Saturday PRO edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

Premium members get:

📊 Monthly reports: 200+ companies visualized.

📩 Tuesday articles: Exclusive deep dives and insights.

📚 Access to our archive: Hundreds of business breakdowns.

PRO members get everything PLUS:

📩 Saturday PRO reports: Timely insights on the latest earnings.

Today at a glance:

☁️ Oracle: Backlog vs. Balance Sheet

🎨 Adobe: Freemium Bet

✍️ DocuSign: IAM Crosses 13% of ARR

🎿 Vail Resorts: Worst Season On Record

🐶 Chewy: Stretched But Steady

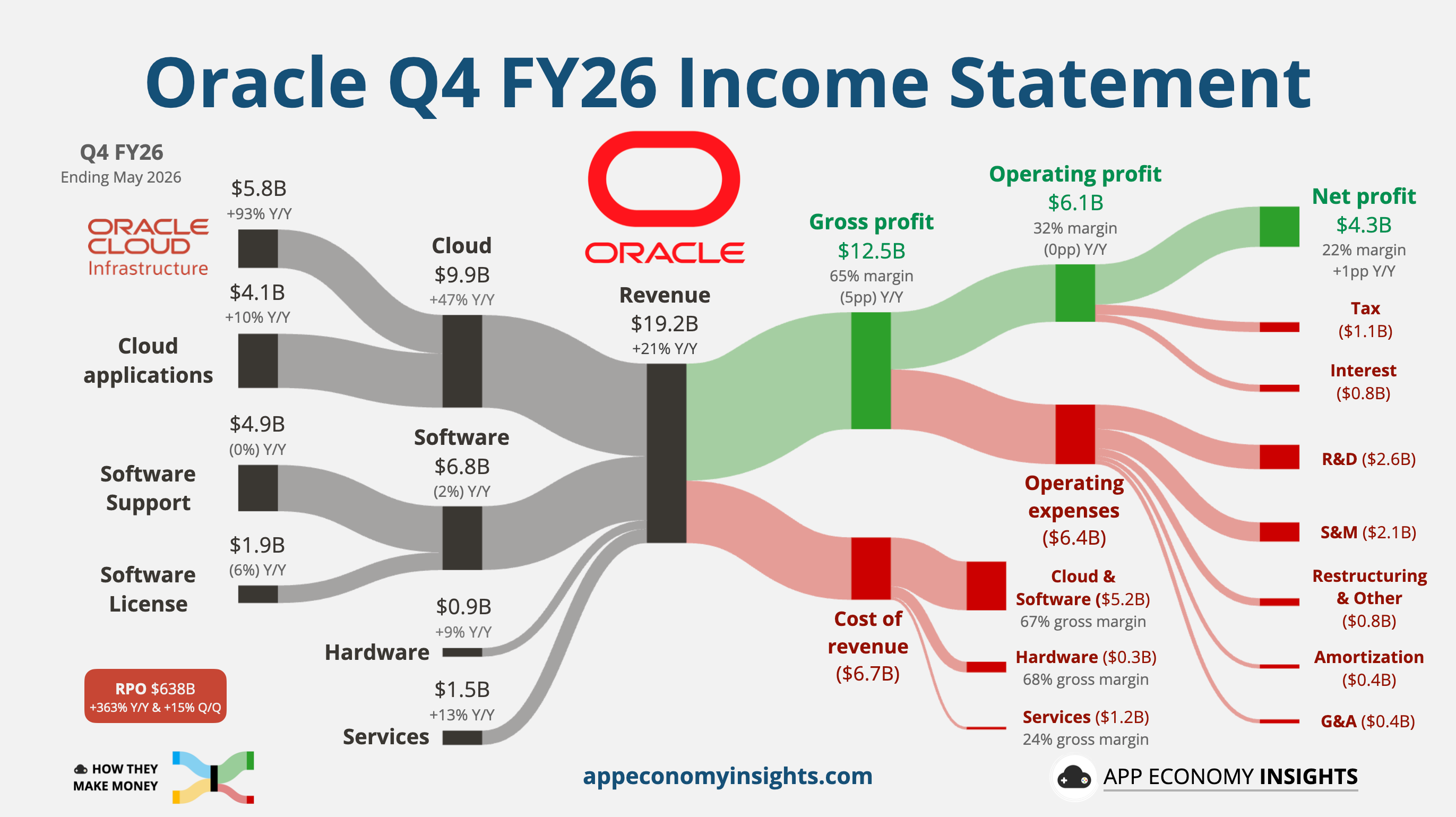

1. ☁️ Oracle: Backlog vs. Balance Sheet

Oracle beat on revenue, beat on earnings, and grew its backlog by $85 billion during the quarter to $638 billion. The stock fell 12% anyway, its worst day since December.

The quarter wasn’t the problem. The incoming bill was. New CFO Hilary Maxson guided FY27 gross margins to “step down” and laid out ~$70 billion in net cash outlay, partly funded by a fresh ~$40 billion raise. Investors naturally scrutinize the cost of converting that backlog.

Q4 FY26 in numbers

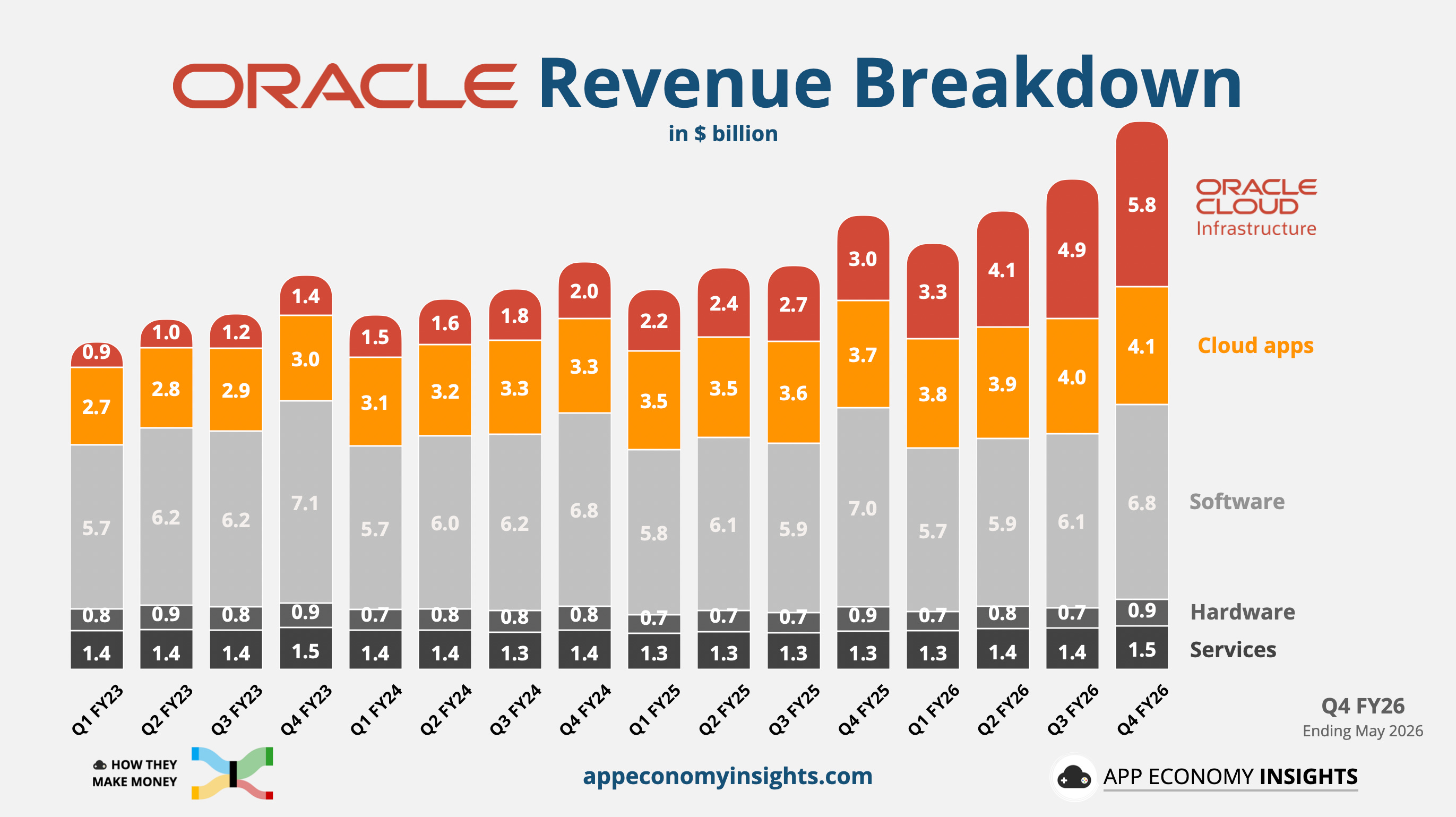

Revenue grew 21% Y/Y to $19.2 billion ($0.1 billion beat). Oracle Cloud Infrastructure (OCI) remains the main driver:

☁️ Cloud +47% Y/Y to $9.9 billion (OCI +93% to $5.8 billion).

🌐 Software -2% Y/Y to $6.8 billion.

🖥️ Hardware +9% Y/Y to $0.9 billion.

💼 Services +13% Y/Y to $1.5 billion.

Margin trends: The operating margin remained flat at 32%, while gross margin compressed by 5pp to 65% as lower-margin IaaS scaled.

Cash flow: For the full year FY26, operating cash flow was $32 billion (+54% Y/Y), but that’s not enough to fund the CapEx ramp. Free cash flow stayed deeply negative (-$24 billion) as CapEx hit $56 billion, above the $50 billion plan.

Balance sheet: Oracle raised $43 billion in debt and $5 billion in equity in FY26 and expects another ~$40 billion in debt and equity financing in FY27. Oracle now has a net debt of $124 billion, including operating lease liabilities.

FY27 guidance: Management reaffirmed FY27 revenue guidance of ~$90 billion, implying ~34% growth. Capital spending is expected to reach roughly $70 billion of Oracle’s own cash outlay. Oracle expects to raise about $40 billion through debt and equity, with any new debt likely pushed to calendar 2027.

So what to make of all this?

📈 The beat the market ignored: RPO jumped 363% Y/Y and 15% Q/Q to $638 billion, well above the ~$590 billion analysts expected. But the market has stopped paying for backlog alone and started pricing the cost of delivering it.

⚖️ Less funding pressure, still massive funding needs: Roughly $75 billion of Oracle’s large AI contracts is prepaid or customer-supplied hardware. That helps. But FY27 capital outlays are still enormous, and Oracle still needs external financing. The funding story improved at the margin. The absolute numbers got bigger.

📉 Margins are the new fault line: Oracle is building capacity before it fully bills. That creates a timing gap: CapEx now, revenue later. Management says infrastructure margins recover quickly once utilization ramps, but investors want proof.

🧱 The old Oracle is now shrinking: Software revenue fell 2% Y/Y. Oracle still needs that legacy cash engine to help fund the AI infrastructure buildout, and a contracting base makes the math harder.

Takeaway: Oracle delivered 1.2 gigawatts of incremental data center capacity in FY26 and expects Q1 FY27 delivery to approach 1 gigawatt. The bull case is becoming more concrete, but so are the capital intensity, margin pressure, and financing needs. Oracle is now a bet on execution.