☁️ Micron: Demand Goes Vertical

While Meta and Tencent push deeper into the AI stack

Welcome to the Free edition of How They Make Money.

Over 300,000 subscribers turn to us for business and investment insights.

In case you missed it:

AI is reshaping capital allocation

Capital is shifting aggressively toward chips, data centers, and model infrastructure. At the same time, management teams are openly questioning how much human labor their future operations actually require.

ServiceNow CEO Bill McDermott recently warned that AI agents could push unemployment for new college graduates into the mid-30% range within two years. While that prediction sounds extreme, the broader shift is already manifesting in corporate behavior.

This week offered three very different examples of that shift.

Today at a glance:

🤖 Meta: More Chips Fewer Humans

📱 Tencent: Agents Meet Distribution

☁️ Micron: Demand Goes Vertical

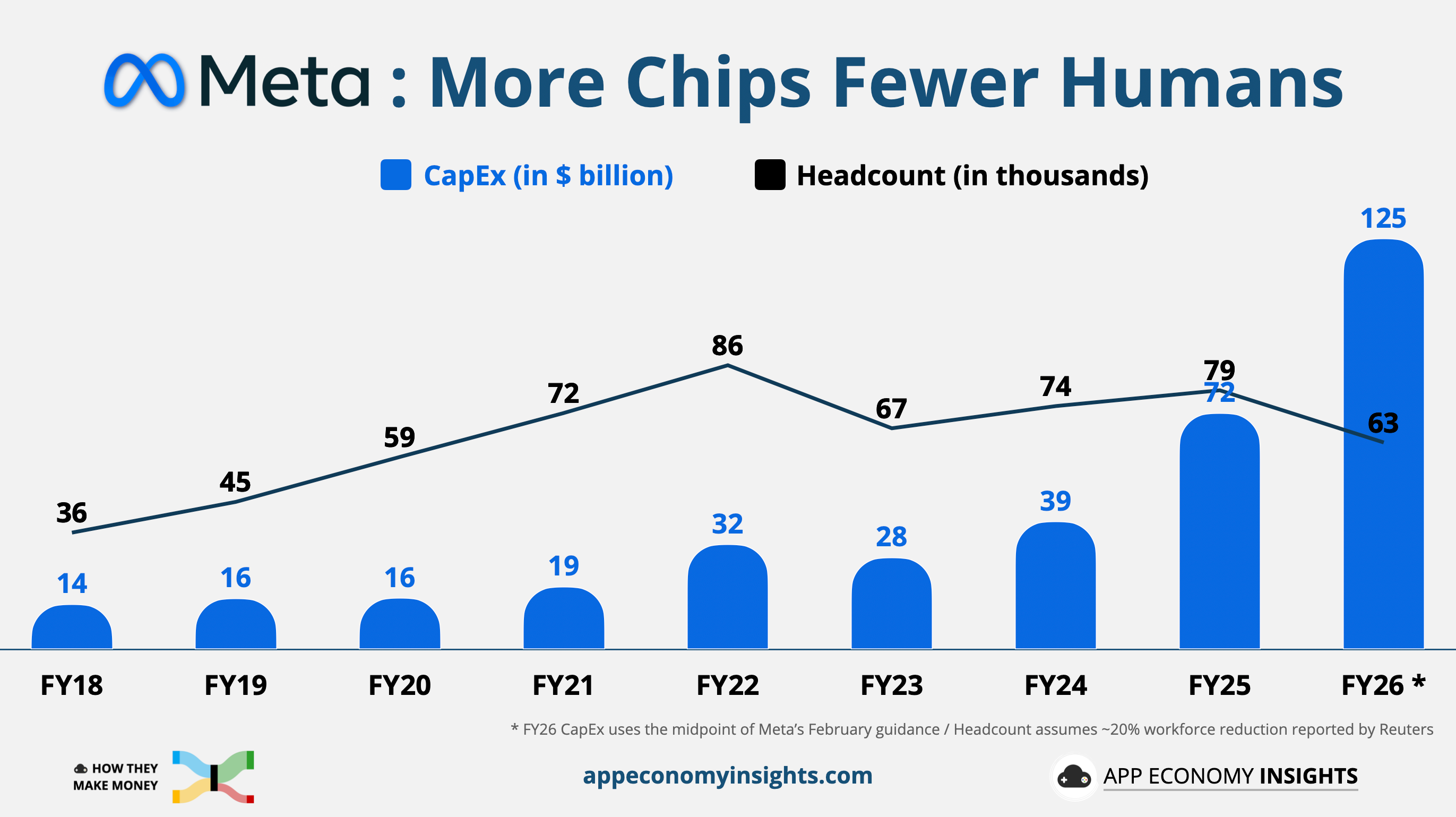

🤖 Meta: More Chips Fewer Humans

Meta’s massive AI CapEx ramp continues to materialize, one infrastructure deal after another.

This week, the company signed a deal worth up to $27 billion over five years with AI cloud provider Nebius, including $12 billion of dedicated capacity starting in early 2027. It is another reminder that Zuck is racing to lock in as much compute as possible before capacity tightens further.

At the same time, Reuters reported that Meta is considering layoffs that could affect 20% or more of its workforce, though the company pushed back, calling the report speculative. If it happens, it would be Meta’s biggest cut since the ‘year of efficiency’ layoffs in 2023.

The two headlines are connected. Meta is not slowing its AI spending. It is reallocating. The company wants more data centers, more chips, and fewer workers doing jobs that AI can increasingly automate. Reuters noted that analysts estimate cuts of that size could save roughly $6 billion. That barely moves the needle for a company planning ~$125 billion in 2026 CapEx.

The bigger picture is that Meta is starting to look like the clearest example of what the AI era may do to Big Tech cost structures. The new org chart may be built less around adding headcount and more around adding compute.

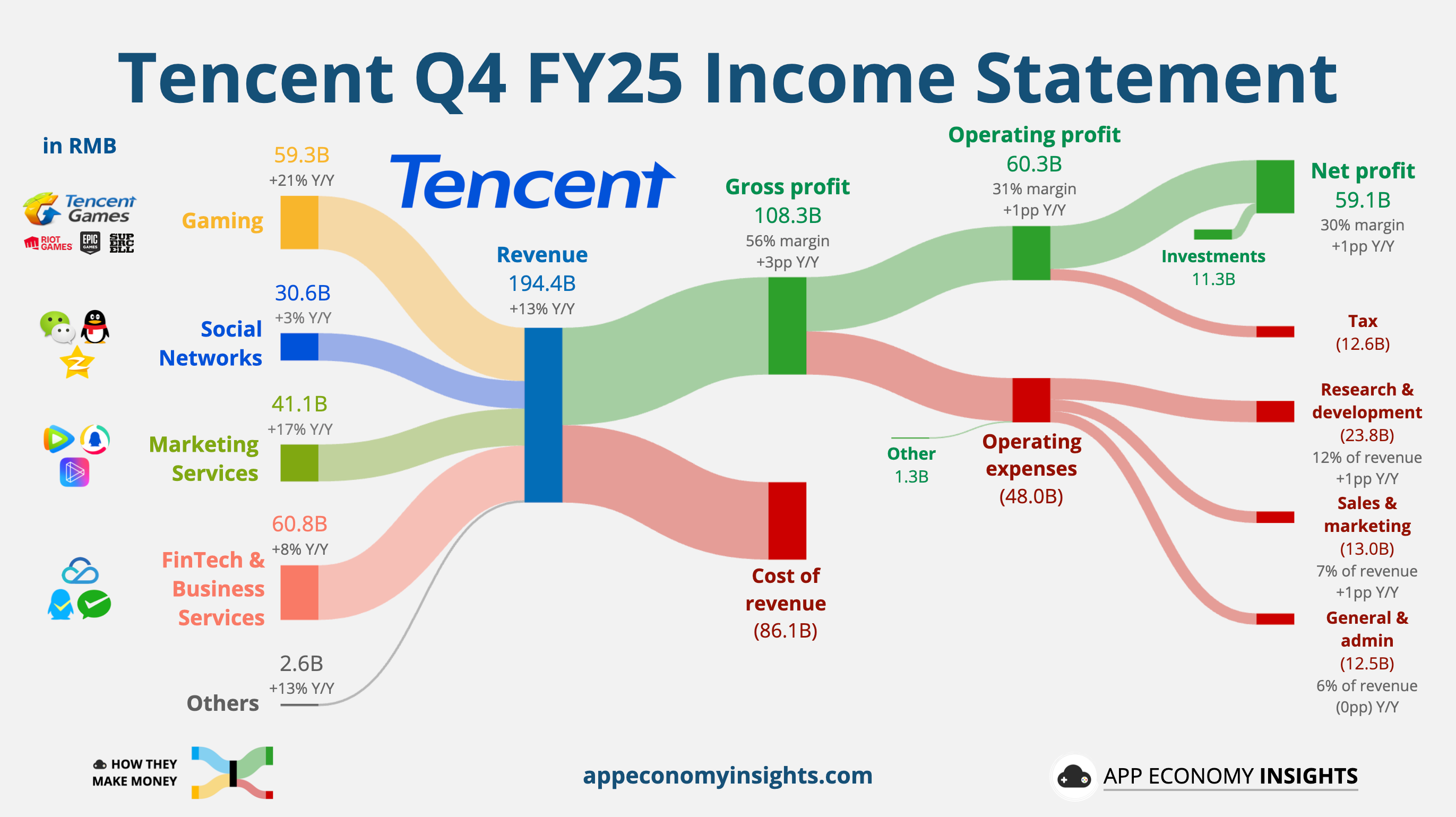

📱 Tencent: Agents Meet Distribution

Tencent’s core business is strong enough to fund a much more aggressive AI push. Q4 revenue rose 13% Y/Y to RMB 194 billion (~$28 billion), while net profit climbed 15%, helped by the higher-margin mix shift toward gaming and advertising.

Gaming led the quarter: Overseas gaming revenue surged 32% to RMB 21.1 billion in Q4. Success was driven by Supercell’s recovery (notably Clash Royale) and the breakout hit Delta Force. Meanwhile, China gaming revenue grew 15% to RMB 38.2 billion, supported by evergreen titles and the launch of Valorant Mobile.

Ad tech is scaling efficiently: Marketing services rose 17% to RMB 41.1 billion. Tencent said its AiM Plus ad model uses generative AI to create and target content, helping the business outgrow the broader Chinese advertising market.

Tencent’s previously measured AI posture is giving way to a much more aggressive one. The company now plans to double AI investment to over RMB 36 billion in 2026 (~$5 billion), funded in part by reduced share buybacks. That push also includes a major Hunyuan 3.0 upgrade expected in April, backed by a restructured research team.

Agents inside the super app: Tencent is moving beyond chatbots to agentic AI. It recently launched QClaw (an AI assistant integrated into WeChat) and WorkBuddy, leveraging the viral OpenClaw framework to automate tasks like travel booking and ride-hailing for its 1.42 billion MAUs.

Cloud is becoming a profit engine: Business Services generated a record RMB 5 billion in adjusted operating profit for the year, showing that Tencent’s pivot toward higher-quality PaaS and SaaS is working.

GPU supply constraints held back hardware purchases in Q4, but Tencent expects that to change in 2026 as H200 chips become more available. The bigger takeaway is that Tencent now has the cash flow, distribution, and product surface area to turn AI from an experiment into a real platform advantage.

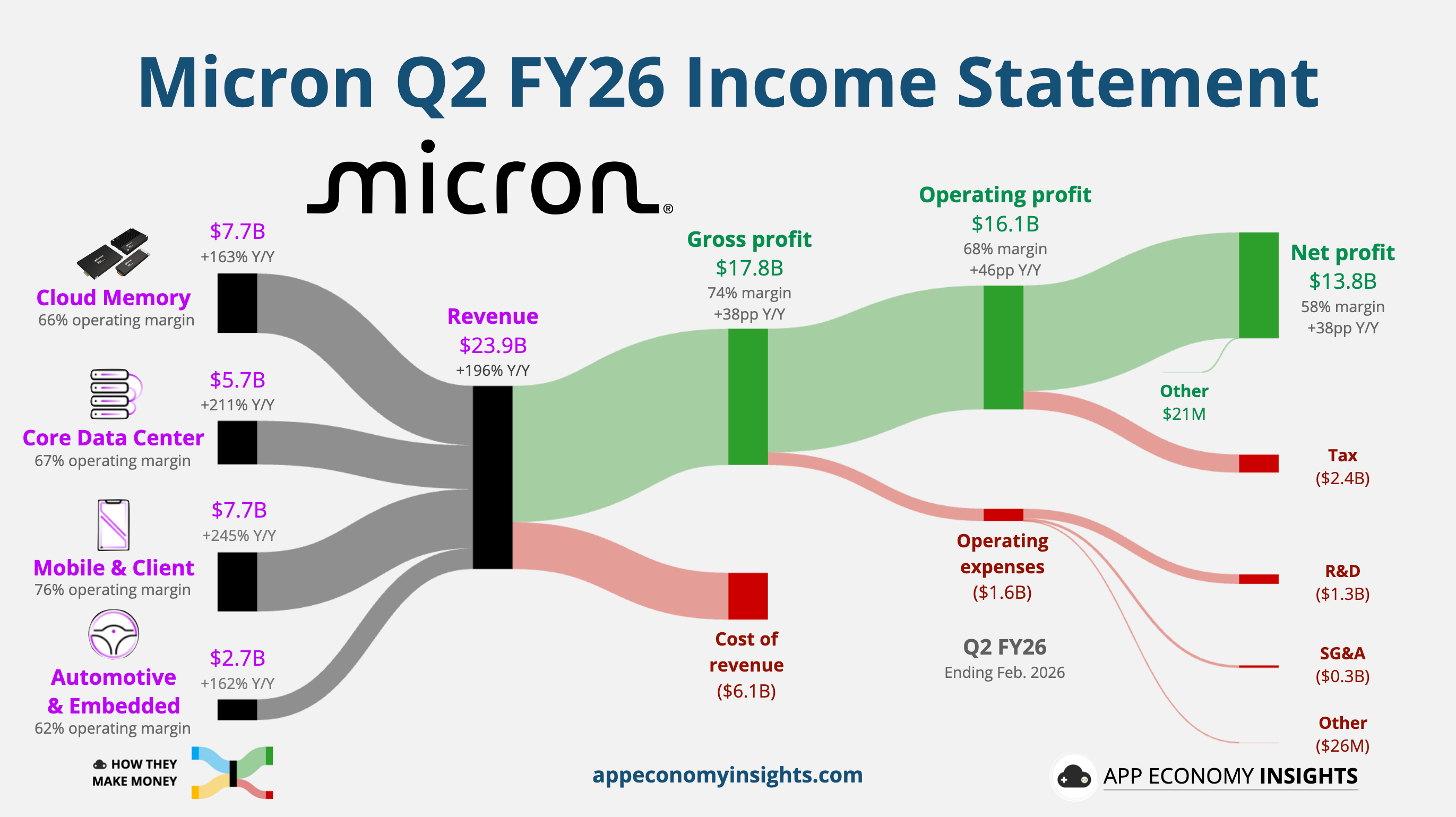

☁️ Micron: Demand Goes Vertical

Micron just released its Q2 FY26 earnings (February quarter), and the results suggest this cycle is accelerating faster than even bullish investors expected. While the stock dipped on aggressive spending plans, the underlying fundamentals remain extraordinary.

Breaking Every Record

Revenue for Q2 skyrocketed 196% Y/Y to $23.9 billion, beating consensus by over $4.5 billion. To put that in perspective, Micron’s revenue guidance for the next quarter alone (~$33.5 billion) now exceeds the full-year revenue of every year in the company’s history through 2024.

Gross margins hit 74%, up from 56% just three months ago. Micron’s guidance for the next quarter points to an 81% gross margin, a figure that actually edges out NVIDIA’s current levels.

The $25 Billion Price Tag

So, why did the stock slide? The answer lies in the massive capital requirements to stay on top.

CapEx surge: Micron raised its FY26 CapEx forecast to over $25 billion, up from the $20 billion discussed last quarter.

2027 ramp: Management warned that fiscal 2027 spending will “step up meaningfully,” increasing by more than $10 billion over 2026 levels.

The investor dilemma: Revenue is booming, but some investors are uneasy about how much cash Micron must pour into fabs in Idaho and New York to keep up.

The Shortage Broadens

The memory shortage has evolved beyond an AI-only narrative. It is now rippling through the broader electronics ecosystem.

HBM4 momentum: Micron has begun volume shipments of HBM4 for NVIDIA’s next-generation platforms, securing its position in a market many feared it would lose to SK Hynix and Samsung.

A longer shortage? While analysts once hoped supply would normalize by 2027, some industry leaders now think tightness could persist for four to five more years.

Consumer spillover: HP recently said memory prices roughly doubled in a single quarter. As Micron prioritizes high-margin AI memory, standard PC and phone manufacturers are fighting for scraps, driving hardware costs higher for everyone.

What to Watch Next

NVIDIA’s Vera Rubin allocation: The next major catalyst is the volume of HBM4 orders for NVIDIA’s upcoming Vera Rubin line. Any shift in how NVIDIA allocates these orders between the Big Three (Micron, Samsung, SK Hynix) will move the needle significantly.

Margin ceiling: With gross margin guidance at 81%, the market will be watching to see whether Micron is nearing a ceiling for profitability or whether pricing power can push margins even higher.

For now, Micron is one of the primary beneficiaries of AI’s second-order effects. Training and inference need compute, compute needs memory, and the world still cannot build enough of it. The open question is no longer whether the demand is real, but how long supply can remain this far behind it.

That's it for today.

Happy investing!

Want to sponsor this newsletter? Get in touch here.

Thanks to Fiscal.ai for being our official data partner. Create your own charts and pull key metrics from 50,000+ companies directly on Fiscal.ai. Save 15% with this link.

Disclosure: I own META and TCEHY in App Economy Portfolio. I share my ratings (BUY, SELL, or HOLD) with App Economy Portfolio members.

Author's Note (Bertrand here 👋🏼): The views and opinions expressed in this newsletter are solely my own and should not be considered financial advice or any other organization's views.

Great-Work! Is it just me, or will Donald Trump appoint a new Fed Chairman (May 15, 2026) who actually supports launching the D-USD (Digital U.S. Dollar)? What would an announcement like that do to BTCUSD?https://cenreico.substack.com/p/spike-in-gold-is-telling-us-something?r=5yuxxv