🔎 Google's NVIDIA Moment?

TPUs, Anthropic, and the race to power AI

Welcome to the Premium edition of How They Make Money.

Over 240,000 subscribers turn to us for business and investment insights.

In case you missed it:

Is this Alphabet’s NVIDIA moment?

The stock has nearly doubled from its April lows, despite all the talk about OpenAI coming for Google’s jugular.

So what’s happening?

Antitrust relief: The regulatory fog has partly lifted. A Chrome divestiture is off the table for now, removing one of the worst-case scenarios.

TPU megadeal: Anthropic just locked in access to up to 1 million Google Cloud TPUs, bringing over 1 GW of AI compute online in 2026. The agreement is “worth tens of billions,” implying meaningful revenue growth acceleration for GCP.

What are TPUs, anyway?

Tensor Processing Units are Google’s custom AI chips, offering faster and more efficient performance than traditional GPUs for training and running large models. Introduced in 2016 to power Search and Translate, TPUs have been available through GCP since 2018 for researchers and select enterprises. What’s new today is scale. Anthropic’s multi-year deal marks the first hyperscale deployment of TPUs by an external AI lab—turning them from a niche option into a credible alternative to NVIDIA’s GPUs.

It’s a marquee win for TPUs. If more deals follow, it could become a meaningful revenue engine, even for a $3+ trillion company like Alphabet.

Here’s what stood out this quarter.

Today at a glance:

Alphabet Q3 FY25.

TPUs & going nuclear.

Key quotes from the call.

Chrome, Atlas, and antirust update.

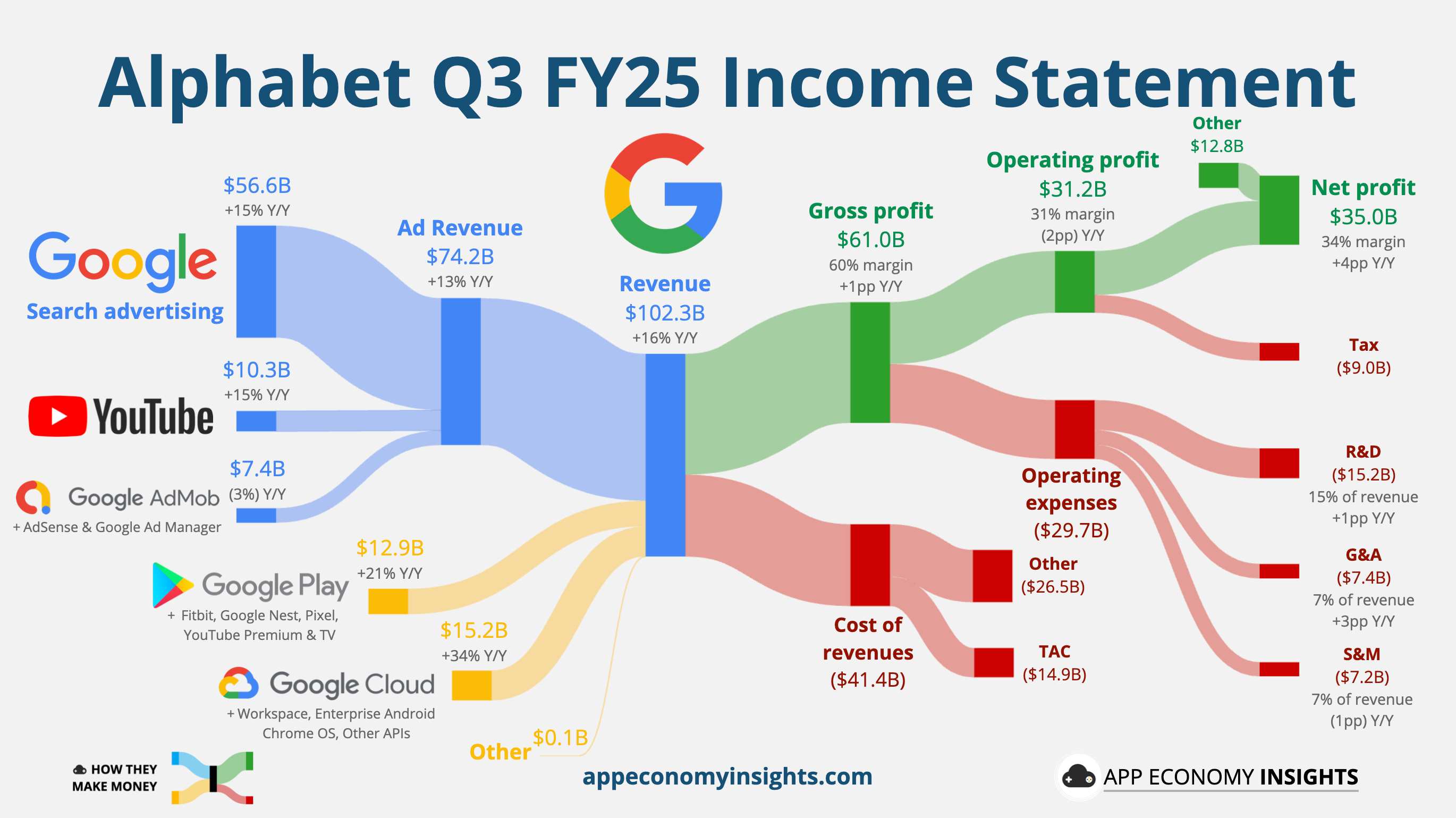

1. Alphabet Q3 FY25

Income statement:

Revenue grew +16% Y/Y to $102.3 billion ($2.2 billion beat).

🔎 Advertising: $74.2 billion (+13%).

Search: $56.6 billion (+15%).

YouTube ads: $10.3 billion (+15%).

Network: $7.4 billion (-3%).

📱 Subscriptions, platforms, and devices: $12.9 billion (+21%).

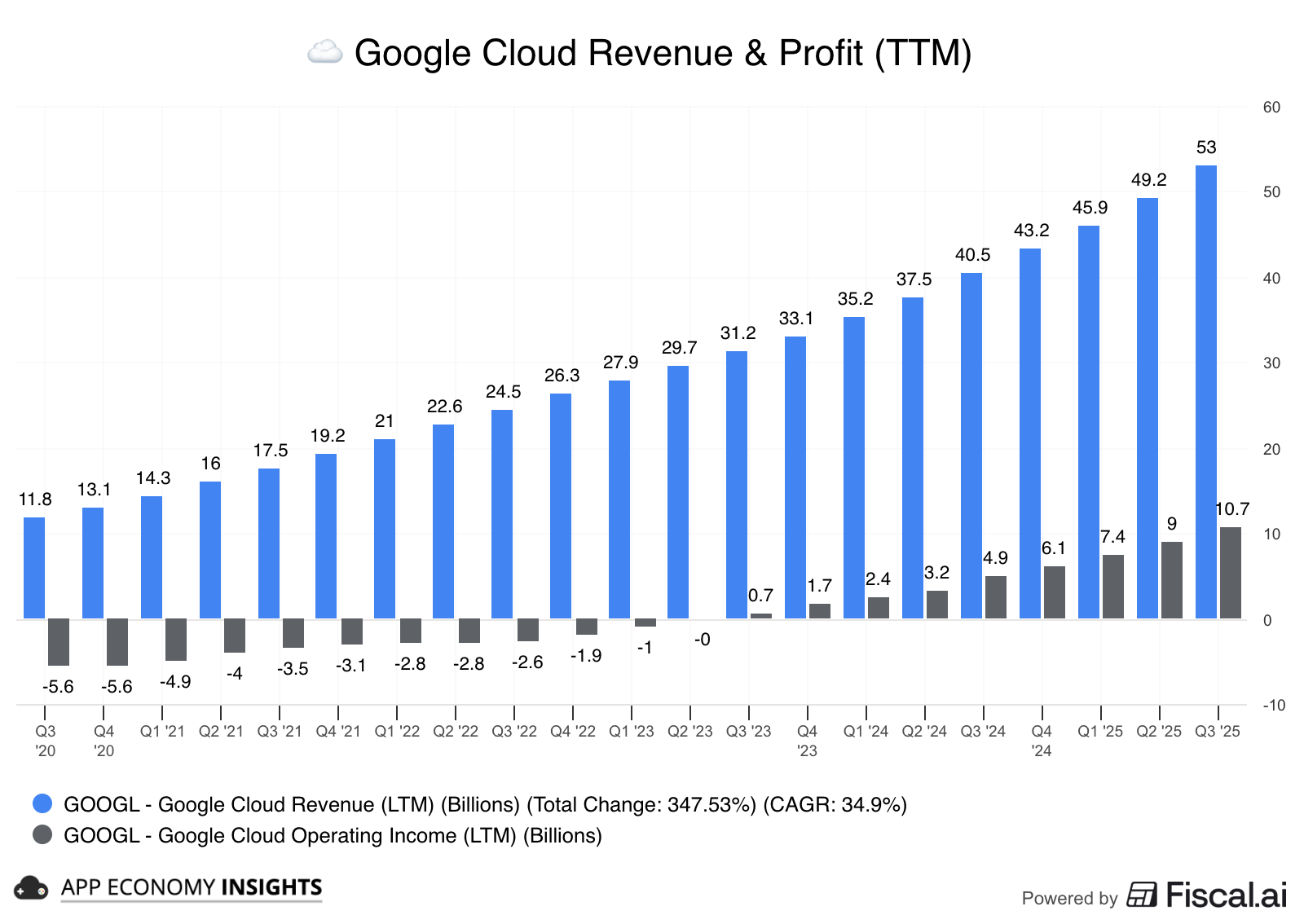

☁️ Cloud: $15.2 billion (+34%).

Margin trends:

Gross margin: 60% (+1pp Y/Y).

Operating margin: 31% (-2pp Y/Y).

Services (Advertising & Other): 39% (-2pp Y/Y).

Cloud: 24% (+7pp Y/Y).

Earnings per share (EPS) grew 35% Y/Y to $2.87 ($0.61 beat).

Cash flow:

Operating cash flow was $48.4 billion (+58% Y/Y).

Free cash flow was $24.5 billion (+39% Y/Y).

Balance sheet:

Cash, cash equivalents, and marketable securities: $98.5 billion.

Long-term debt: $21.6 billion.

So, what to make of all this?

New milestone: Alphabet’s revenue topped $100 billion for the first time, rising 16% Y/Y (+15% Y/Y in constant currency, up from +13% Y/Y in Q2), and net income surged +33% Y/Y to $35 billion.

Search rose +15% Y/Y, driven by retail and financial services. AI Overviews and ‘AI Mode’ are boosting engagement, turning last year’s cannibalization fears into a tailwind as commercial intent rebounds.

YouTube Ads jumped +15% Y/Y, driven by both brand budgets and direct-response. Shorts now see 200 billion daily views, while YouTube Premium helped lift total paid subs beyond 300 million.

Subscriptions, platforms & devices climbed to +21% Y/Y, reaching a $50 billion annual run rate for the first time, led by One and Pixel hardware.

Cloud posted a +34% Y/Y growth, up from +32% Y/Y in Q2, pushing trailing-12-month (TTM) revenue above $50 billion and a record $155 billion backlog (more on this in a minute). Operating income in the unit jumped 85% to $3.6 billion, signaling strong leverage.

Margins & Capex: Company-wide operating margin held firm at 31%, despite record AI and infrastructure spending. Alphabet raised its 2025 CapEx outlook to $91–93 billion (up from ~$85 billion), after spending $24 billion in Q3. Most of that is going into data centers, TPUs, and AI infrastructure — the physical backbone of Gemini and Cloud.

💡 Key takeaway: Alphabet is executing on both sides of the AI equation: monetization through ads and subscriptions, infrastructure expansion through Cloud and compute. With revenue growth reaccelerating, margins holding strong, and capex ramping, the company is firmly back on offense.

2. TPUs & going nuclear

Anthropic’s partnership now spans training, inference, and dedicated capacity, marking the first hyperscale deployment of Google’s in-house AI chips by an external lab.

Why this is a big deal

Like most AI deal announcements, it comes down to the equity portion, strategy, and long-term revenue implications.