🏦 US Banks: Q2 Mixed Bag

Investment deals shine, but NII gets under pressure

Welcome to the Tuesday Premium edition of How They Make Money.

Over 130,000 subscribers turn to us for business and investment insights.

In case you missed it:

As always, earnings season kicks off with US Banks.

These top lenders set expectations for the macro environment.

Expect an avalanche of visuals in the coming weeks as the reports for the second quarter of 2024 trickle in. Stay tuned for Netflix this Friday! 🍿

So, what did we learn from the big banks?

Today at a glance:

The Big Picture

JPMorgan: Cautious Optimism

Bank of America: Profit Dips

Wells Fargo: Outlook Disappoints

Morgan Stanley: Wealth Slowdown

Goldman Sachs: Strategic Shift

Charles Schwab: Record Assets

Citigroup: Regulatory Hurdles

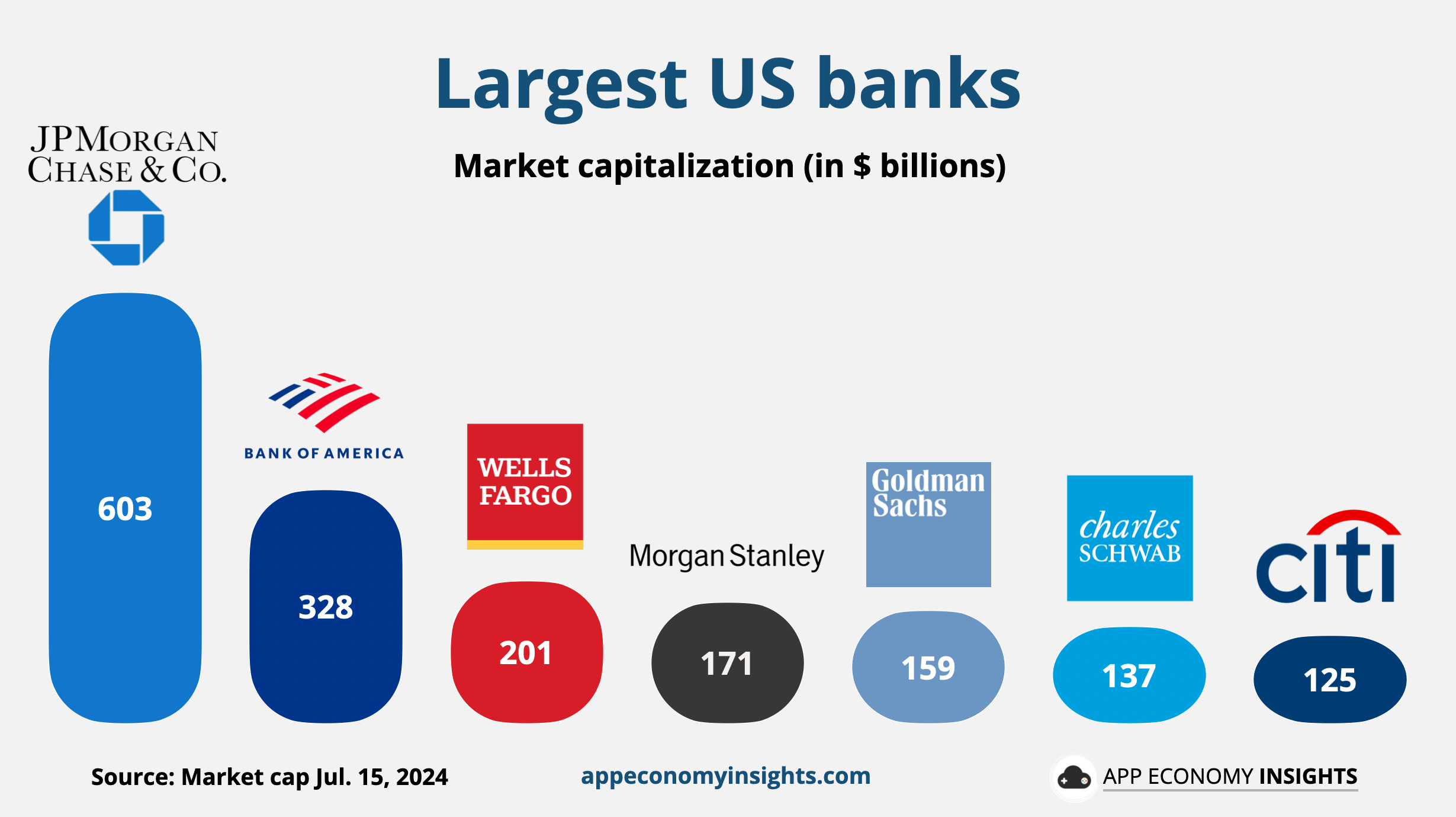

The Big Picture

Here’s an updated look at the largest US banks by market cap.

JPMorgan CEO Jamie Dimon explained:

“While market valuations and credit spreads seem to reflect a rather benign economic outlook, we continue to be vigilant about potential tail risks.”

Dimon's cautious optimism perfectly encapsulates the mood surrounding Q2 earnings for major US banks. While investment banking activity provided a bright spot, concerns over slowing growth, rising credit risks, and geopolitics cast a shadow on future prospects.

As a reminder, banks make money through two main revenue streams:

💵 Net Interest Income (NII): The difference between interest earned on loans (like mortgages) and interest paid to depositors (like savings accounts). It’s the main source of income for many banks and depends on interest rates.

👔 Noninterest Income: The revenue from services unrelated to interest. It includes fees (like ATM charges), advisory services, and trading revenue. Banks relying more on noninterest income are less affected by interest rate changes.

Here are the major developments in Q2 FY24:

📉 NII Pressures Intensify: The decline in net interest income (NII) accelerated in Q2, with banks like Wells Fargo missing estimates and revising guidance downward due to higher deposit costs in a competitive landscape.

📈 Investment Banking Resurgence: Investment banking activity rebounded strongly for some banks (albeit from a low base), driven by increased dealmaking and a recovering IPO market, providing a much-needed boost to fee-based income.

⚠️ Credit Concerns Rise: Credit loss provisions increased across major banks, particularly in consumer lending, reflecting growing caution amid economic uncertainty and higher interest rates.

💳 Visa Gains Mask Underlying Trends: One-time accounting gains from a Visa share exchange deal (allowing big banks to restructure their stake) artificially inflated profits for banks like JPMorgan Chase and Citigroup. It’s essential to look beyond these one-off events to assess their true performance.

💼 Mixed Wealth Management Results: While some banks experienced continued growth in wealth management, others faced headwinds due to market volatility and changing investor sentiment.

⚙️ Restructuring Efforts Continue: Banks continued their focus on streamlining operations and optimizing their business portfolios to improve efficiency and long-term profitability.

⚖️ Regulatory Scrutiny Persists: Regulatory challenges remained a key concern, with Citigroup facing fines for insufficient progress in addressing data management issues and Wells Fargo still operating under regulatory restrictions.

🚨 Fed Stress Test Raises Concerns: The Federal Reserve's stress test revealed increased vulnerabilities among major banks, with projected losses higher than the previous year.

🤔 Investor Sentiment Wavers: Despite strong year-to-date performance, bank stocks experienced a setback in Q2 as earnings results mostly failed to meet heightened expectations, reflecting concerns about NII pressures and credit quality.

Here is the Q2 FY24 performance Y/Y at a glance.

Let’s visualize them one by one and highlight the key points.