🚖 Tesla: Robotaxi Pivot

A new strategy emerges amid declining sales and layoffs

Welcome to the Premium edition of How They Make Money.

Over 100,000 subscribers turn to us for business and investment insights.

In case you missed it:

📉 Tesla (TSLA) shares are nearly 65% off their peak.

That’s a critical detail to keep in mind before judging a post-earnings pop.

The company missed expectations for the third consecutive quarter.

So, what’s happening?

Two key executives departed.

Tesla cut 10% of its workforce.

The company is losing market share.

Deliveries have declined 9% from a year ago.

Competition is heating up for humanoid robots.

A new strategy emerged with lower FSD prices.

Musk teased a Tesla Robotaxi announcement in August.

From the shareholder letter:

"The future is not only electric, but also autonomous. We believe scaled autonomy is only possible with data from millions of vehicles and an immense AI training cluster. We have, and continue to expand, both.”

As always, we want to look beyond the headlines. Tesla has been through rough patches in the past and has come stronger on the other end. But it faces more competitive pressure today. The company's future hinges on autonomous driving and this shift could take time.

The quarter had a lot to unpack, and we're here to walk you through it with visuals and data-driven insights.

Today at a glance:

Tesla Q1 FY24.

Recent business highlights.

Key quotes from the earnings call.

What to watch looking forward.

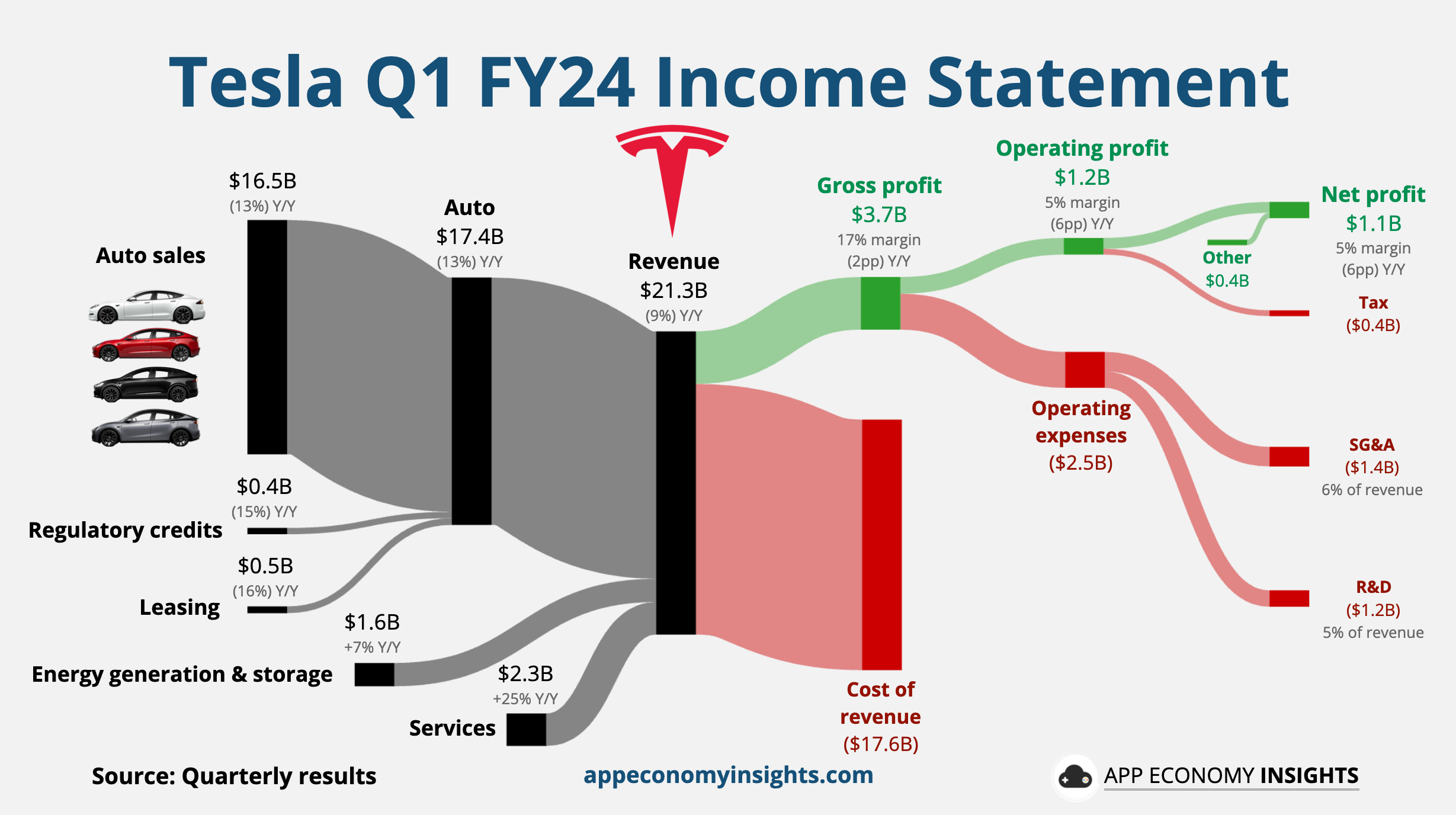

1. Tesla Q1 FY24

Tesla's revenue comes from three primary sources:

🚗 Automotive: Revenue from selling electric vehicles, including models S, 3, X, and Y (82% of revenue).

🔌 Services and Other: Revenue from vehicle service, Supercharger network, and sales of automotive parts and accessories (11% of revenue).

🌞 Energy Generation and Storage: Revenue from solar products and energy storage solutions, like Solar Roof and Powerwall (8% of revenue).

Q1 FY24 Key metrics:

Production: 433K vehicles (-2% Y/Y).

Deliveries: 386K vehicles (-9% Y/Y).

Analysts expected roughly 423K deliveries, making it a significant miss. Management blamed the decline on the ramp-up for the updated Model 3 (Fremont), external disruption from the Red Sea conflict, and the arson attack at Gigafactory Berlin.

Income statement:

Revenue declined by 9% Y/Y to $21.3 billion ($1.0 billion miss).

The average price per vehicle declined alongside the deliveries, leading to automotive revenue declining by 13% year-over-year.

Gross margin was 17% (-3pp Q/Q, -2pp Y/Y).

Operating margin was 5% (-3pp Q/Q, -6pp Y/Y).

EPS (non-GAAP) was $0.45 ($0.05 miss).

Gross margin trends: