🏦 US Banks: Q2 FY23 Earnings

What we learned from the big banks and what to watch

Greetings from San Francisco! 👋

Welcome to the new members who have joined us this week!

Join the 40,000+ How They Make Money subscribers receiving insights on business and investing every week.

Today, we kick off earnings season with US Banks.

The banking sector serves as the economy's barometer, so their performance can give us a pulse on the broader economic health. Let’s review what we learned.

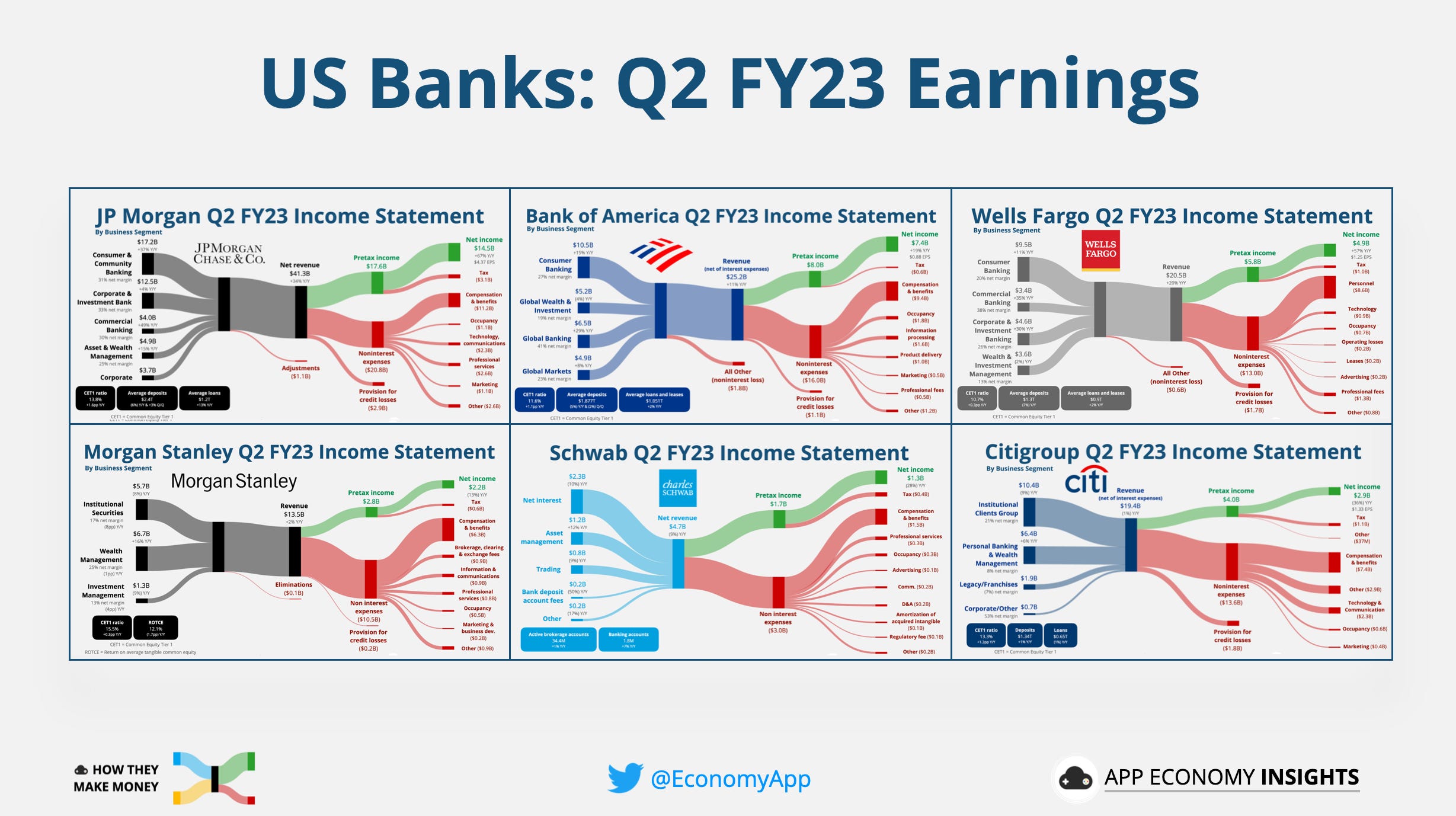

Here is a sneak peek at the report:

We’ll break down earnings, including key quotes:

JP Morgan Chase.

Bank of America.

Wells Fargo.

Morgan Stanley.

Schwab.

Citigroup.

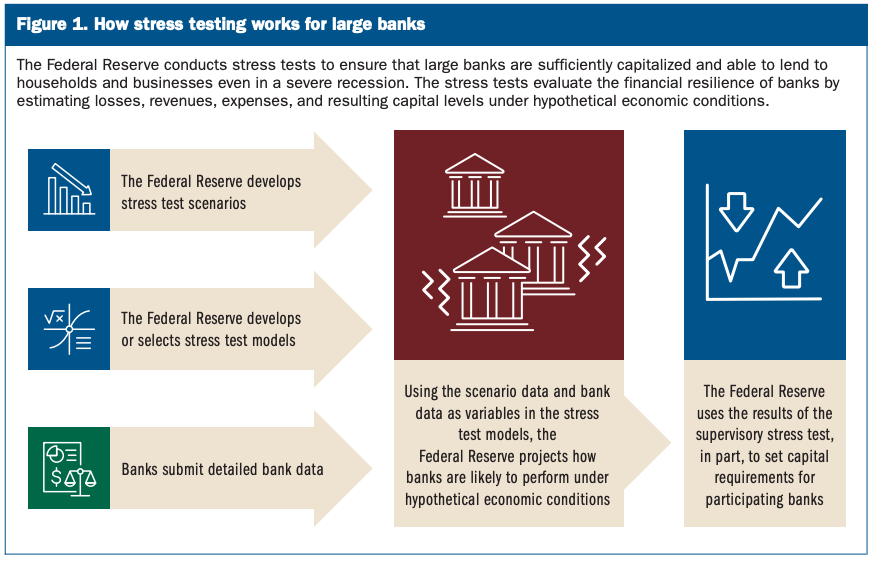

The major US banks passed the stress test

According to the most recent Federal Reserve stress test, the 23 largest US banks have showcased resilience despite recent banking failures. However, indications from the Fed suggest that future stress tests might see an increase in their stringency, stemming from lessons learned from this year's banking crisis.

The Fed simulated a severe global recession scenario in which:

Commercial real estate prices fall by 40%.

Office vacancies rise substantially.

Unemployment rises to 10%.

Home prices drop by 38%.

In this severe scenario, the collective losses for the 23 largest banks would total $541 billion, pushing their capital ratios down from 12.4% to 10.1%.

Midsize and super-regional banks—such as M&T Bank, Citizens Bank, US Bancorp, and Truist—passed but showed relative weaknesses that may concern investors.

The Fed's tests indicate that banks with large trading books could withstand a market shock due to inflation and rising interest rates.

Is a soft landing on the horizon?

Goldman Sachs recently revised the likelihood of a US recession occurring within the next year to 20%, a notable reduction from a previous estimate of 25%.

Chief Economist Jan Hatzius explained the revision by stating:

"The main reason for our cut is that the recent data have reinforced our confidence that bringing inflation down to an acceptable level will not require a recession.”

It's worth noting that Goldman Sachs had previously hiked its recession probability to 35% in March in response to the banking crisis.

The big picture

The big banks are dealing with a mix of tailwinds and headwinds:

Higher rates: The Federal Reserve hiked rates from virtually 0% in Q1 2022 to a current range of 5.00%-5.25%, with a further increase of 0.25% widely anticipated. This allows banks to charge higher loan rates.

Rising competition: Amid higher rates, the scramble for deposits intensifies. Banks are compelled to offer higher rates to depositors as competition from smaller entities and new market entrants heats up. Apple launched its new high-yield savings account (4.15% APY) in April.

Lending up, investing down: Across the board, banks are seeing a rise in net interest income buoyed by higher interest rates. Conversely, noninterest income sources, like wealth management and investment banking, are experiencing a downturn due to an unfavorable market and a scarcity of IPOs.

Office loan losses: JP Morgan Chase and Wells Fargo have augmented provisions for commercial property loan losses in Q2 FY23, largely due to exposure to offices. As remote work gains traction and layoffs persist, office landlords face mounting challenges, leading some to strategically default on loans to initiate renegotiations.

Regional banks exodus: In a flight to safety, depositors gravitate towards larger banks, putting smaller institutions under pressure to raise deposit rates to retain clients.

Consolidation: In a significant move, JP Morgan Chase acquired a majority of assets and assumed specific liabilities from the beleaguered First Republic Bank in May. This acquisition, facilitated by a federal auction, led to an upfront post-tax gain of $2.7 billion for JPMorgan, offset by projected post-tax restructuring costs of approximately $2.0 billion in 2023 and 2024. Despite First Republic Bank's struggles, this strategic acquisition is expected to modestly boost JPMorgan's earnings and generate over $500 million of additional net income annually. First Republic Bank's 84 branches will continue to operate as usual under JPMorgan Chase.

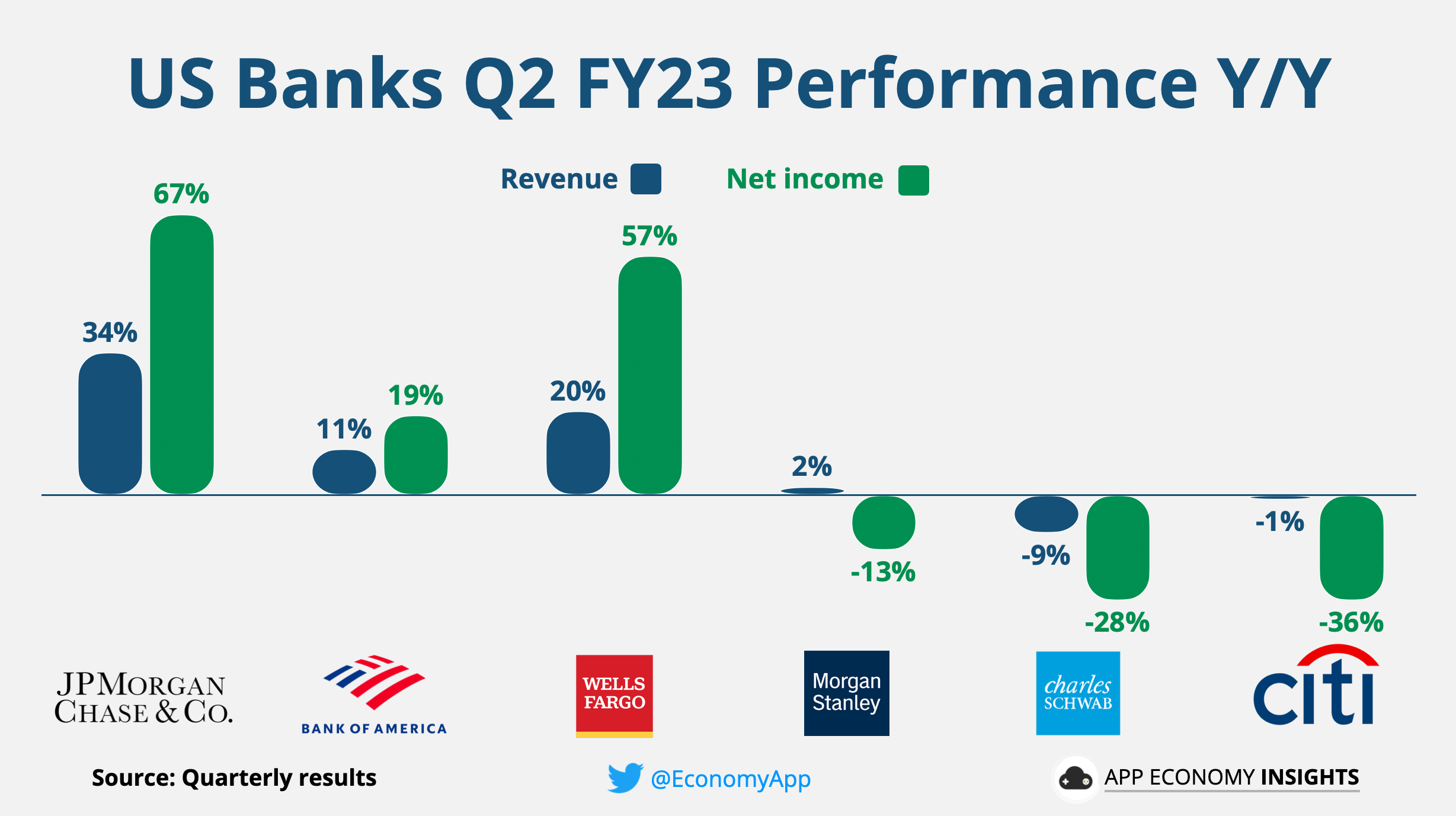

Here is the bird’s-eye view of the Q2 FY23 performance Y/Y.

As you can see, Q2 had a wide range of fortunes for the big US banks.

Let’s look closer.

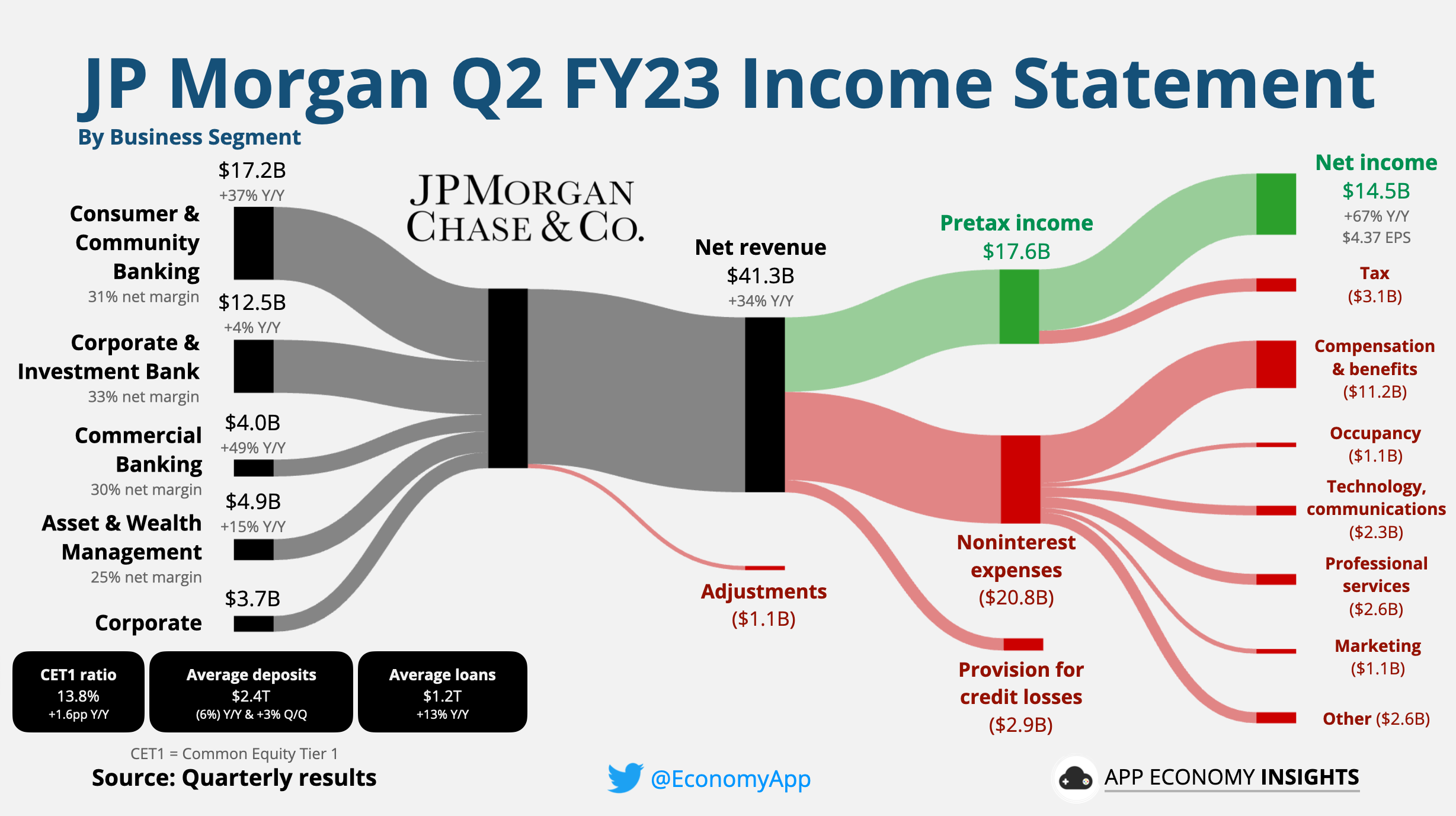

JP Morgan Chase

Revenue grew +34% Y/Y to $41.3 billion ($2.5 billion beat):

Net Interest income: $21.8 billion (+44% Y/Y).

Noninterest income $19.5 billion (+25% Y/Y).

Breakdown by business segment: