🏦 US Banks: Q1 FY23 Earnings

What we learned from the big banks and what to watch

Greetings from San Francisco! 👋

Welcome to the new members who have joined us this week!

Join the 34,000+ How They Make Money subscribers receiving insights on business and investing every week.

Today, we turn to US Banks. They just reported their Q1 FY23 performance.

Bank earnings are closely monitored as they often reflect the overall health of the broader economy. So let’s review what we learned.

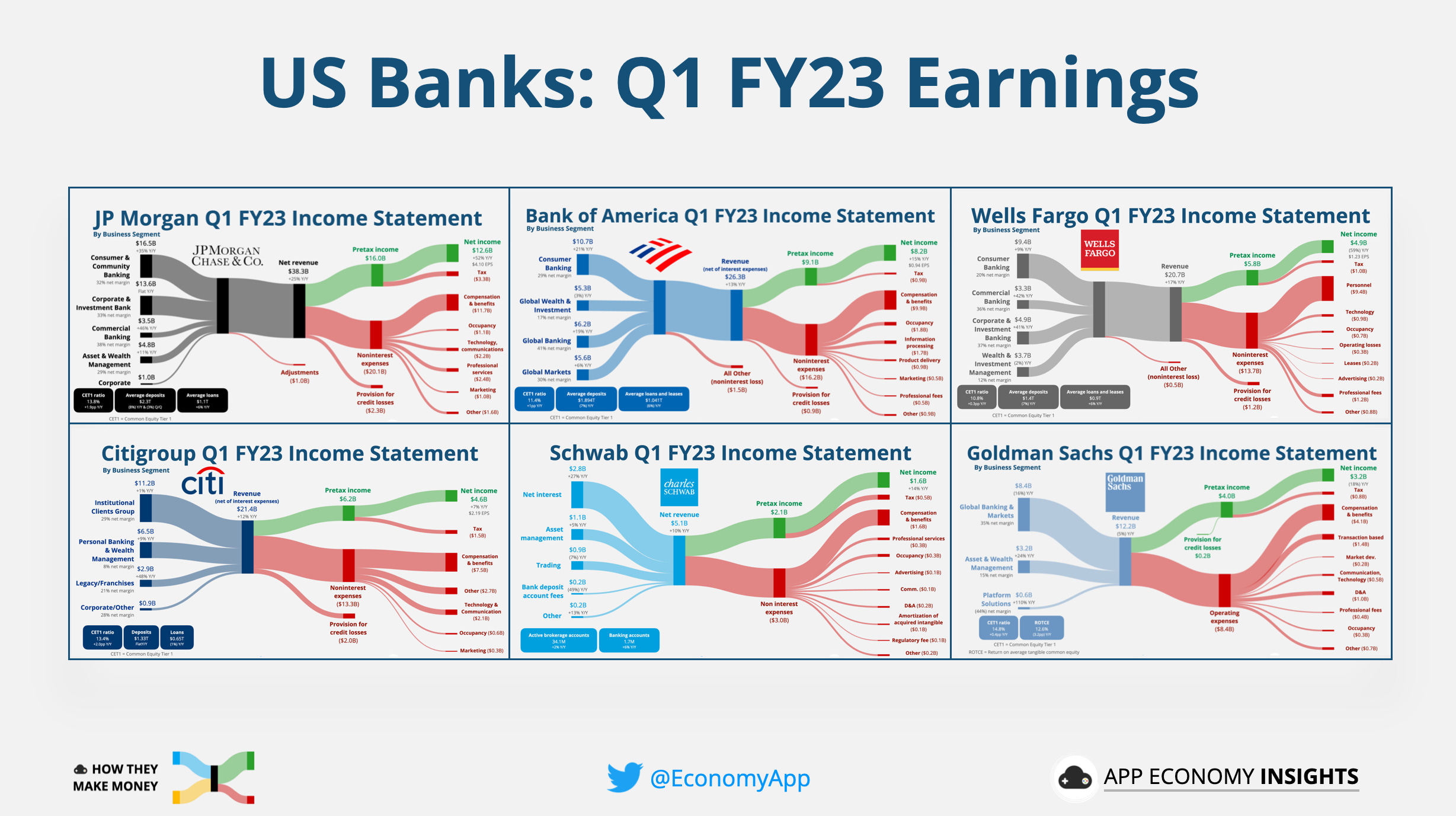

Here is a sneak peek at the report:

We’ll break down earnings, including key quotes from the call:

JP Morgan Chase.

Bank of America.

Wells Fargo.

Goldman Sachs.

Citigroup.

Schwab.

The big banks have benefited from two tailwinds this quarter:

Higher rates: The federal reserve lifted rates from essentially 0% in the first quarter of 2022 to a range of 4.75%-to-5% today. Big banks were able to charge higher rates on loans without significantly increasing the rates paid to depositors.

Regional banks exodus: Following the collapse of Silicon Valley Bank and Signature Bank, many depositors fled regional banks in favor of the big players. As a result, JP Morgan estimated that it picked up about $50 billion in new deposits at quarter-end (more on that in a second).

In short, the big banks not only survived but thrived through the recent crisis. However, we ought to wonder how long the new deposit inflow will stick around. Depositors may be looking for higher rates in the coming months.

Fed data showed that depositors moved over $600 billion from their accounts in the first quarter, primarily to get a better return in money-market funds.

While the rapid rise in rates was meant to cool inflation, it led to the demise of some regional banks. Many bank customers have developed a preference for larger institutions “too big to fail.” The top US banks have benefited from a temporary influx in deposits, without having to increase deposit rates as some smaller banks.

It’s been a boon for revenue and profit across the board. We’ll cover them in detail, but here is the bird’s-eye view of the Q1 FY23 performance Y/Y. Goldman Sachs was the outlier of this group.

The recent bank system turmoil is expected to lead to a pullback in lending by Fed officials. But for now, big banks have not materially changed their lending plans.

The outlook remains uncertain due to concerns about the macro environment and the potential for an upcoming recession. As a result, banks have increased their provision for credit losses. Credit-card delinquencies increased year-over-year, and more borrowers carried over balances.

In addition, investment banking and underwriting have been slow. The wealth management segments have been lagging in what remains a bear market.

📱A new challenger approaches: If you missed the big news yesterday, Apple (the largest company in the world) launched Apple Card’s saving accounts in partnership with Goldman Sachs. They offer a 4.15% APY (one the highest on the market right now, directly competing with small fintech firms like Robinhood or SoFi).

No fees.

No minimum deposits.

No minimum balance requirements.

This could add pressure to deposits at large US banks in the coming months.

Let’s look closer at the specific banks.

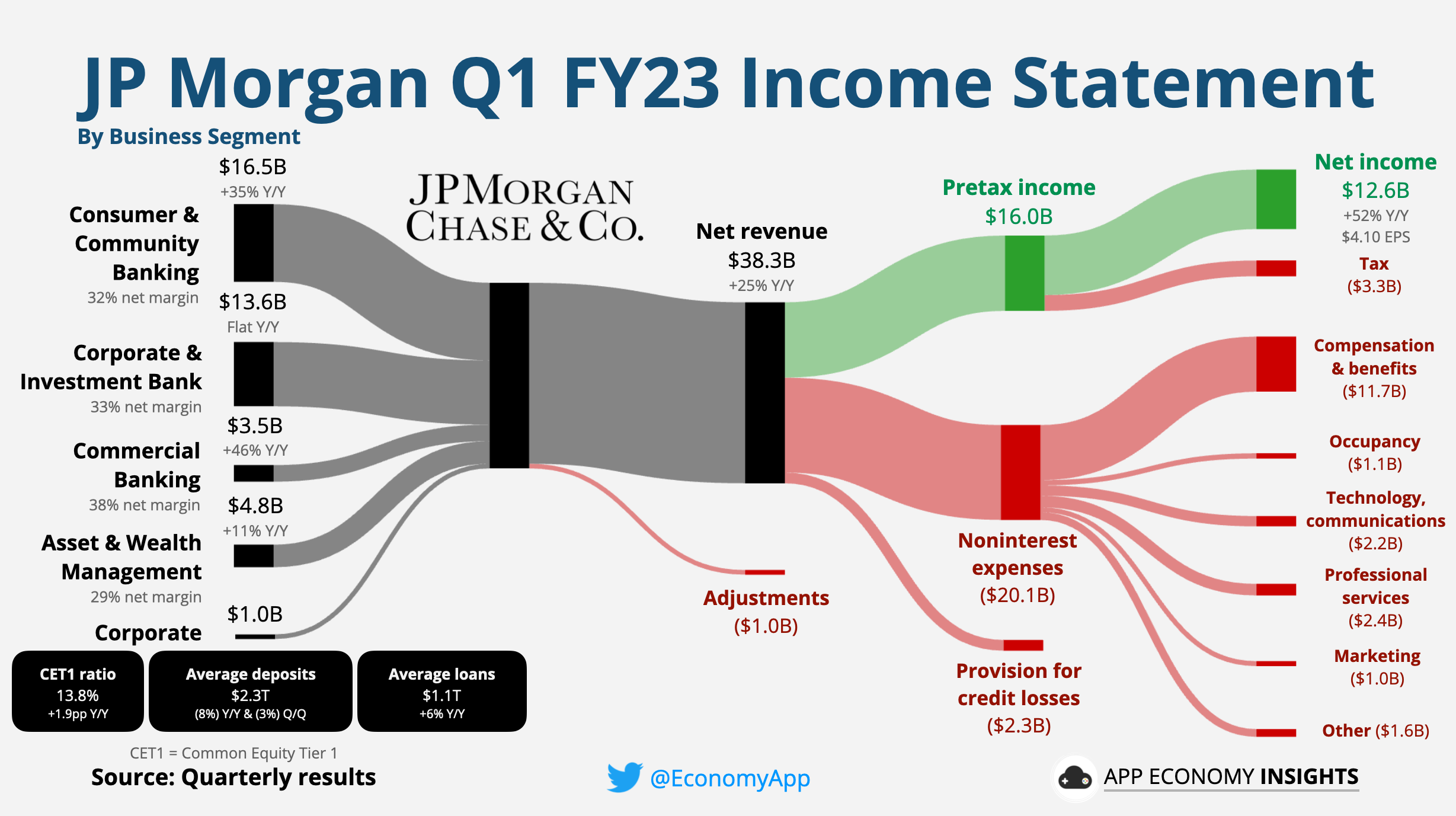

JP Morgan Chase

Revenue grew +25% Y/Y to $38.3 billion ($2.5 billion beat):

Net Interest income: $20.8 billion (+49% Y/Y).

Noninterest income $18.5 billion (+5% Y/Y).

Breakdown by business segment: